USD holds on tariff headlines

As anticipated, the tariff deadline morphed into a guideline. The dollar held steady after President Donald Trump confirmed that reciprocal tariffs are set to take effect on August 1. Still, trade tensions are poised to intensify: a dozen or more U.S. trading partners will receive formal notice this week outlining proposed tariff rates, some potentially reaching as high as 70%. Treasury Secretary Scott Bessent added that for countries failing to strike a deal by April 2, tariffs would snap back to those earlier levels. Buckle up for a turbulent week in trade.

For the Canadian dollar, last week, probed the lower end of its 1.36–1.38 consolidation range, spurred by U.S. payrolls data that failed to reinvigorate the greenback’s momentum. For CAD strength to gain further traction, traders will be watching for a clean break below 1.359, a key support level that could shape price action through July.

Technically, the bias leans toward continued USD weakness is showing signs of fatigue. However, since May, both the 40-day and 100-week moving averages have acted as firm resistance near the 1.38 level, capping upside attempts. Adding to the bearish tone is the 100-day moving average crossing below the 200-day, a classic “death cross” formation, suggesting downside pressure may persist. Should the U.S. dollar stay under strain, attention could shift to the 2025 low at 1.354 as the next downside target. Tariffs aside, with no major macro catalysts on deck this week apart from Thursday’s jobless claims, it’s shaping up to be a relatively subdued week, price action may remain rangebound, with markets eyeing Friday’s Canadian employment figures for June.

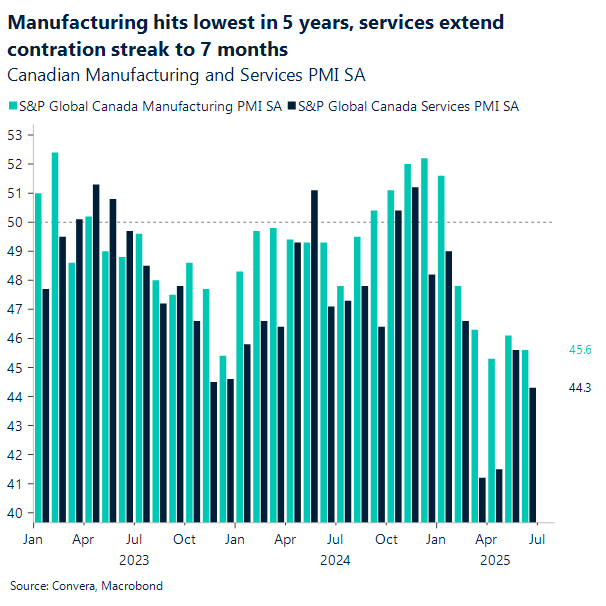

On the macro front, S&P Global’s June Canada Manufacturing PMI slid to 45.6, the lowest in over five years, marking a fifth straight month of contraction. Weighed down by tariff-hit exports and sharp inventory drawdowns, the numbers stoked further growth concerns. Meanwhile, the Services PMI fell to 44.3 from 45.6 in May, reflecting a faster pace of decline and extending the contraction streak to seven months. Activity and new business volumes continued to retreat, underscoring lingering uncertainty, particularly around U.S. trade policy. Employment ticked higher for a second consecutive month, while on the inflation side, input costs surged to their highest level since October 2022, driven by rising supplier prices.

Trade in focus: July 9th deadline is here

After Thursday’s upbeat labour market surprise perked up the dollar, the mood soured later that day—on the eve of Independence Day—when President Donald Trump announced that his administration would begin sending formal letters to trading partners. These letters would outline unilateral tariff rates scheduled to take effect on August 1, with the notorious July 9th deadline now looming (this Wednesday).

The dollar swiftly lost ground, slipping below the 97 mark and remaining subdued for the rest of the session.

Trump originally unveiled the higher so-called “reciprocal” tariffs on April 2, but paused implementation for 90 days to allow time for negotiations (until July 9th), temporarily setting a 10% base rate.

He has long threatened that failure to reach deals ahead of the deadline would trigger automatic tariff hikes—raising the stakes for trading partners now racing to finalize agreements. Still, many now view the deadline as more fluid than firm, calling it part of Trump’s negotiation playbook. Adding to this softer scenario, Treasury Secretary Scott Bessent revealed over the weekend that countries failing to reach an agreement by the July 9th deadline may be granted a three-week extension to negotiate. His statement stands in stark contrast to the more hardline, threat-driven stance typically adopted by President Trump—offering fresh insight into the administration’s multi-pronged negotiation strategy. This nuanced shift helped the dollar recover some ground in early London trading, with the DXY climbing back above the 97 mark and hovering at 97.200 this morning.

On the data front, little is scheduled. Keep an eye on the NFIB Small Business Optimism Index, as small firms are expected to be among the hardest hit by tariffs. Also watch the FOMC minutes for clues on the policy path, but expect the familiar “wait-and-see” mode to prevail once more. With few catalysts ahead, trade talks and tensions will be the key drivers of dollar direction—and likely shape broader FX price action through the week.

Euro rallies on hype, not on health

The euro closed the week firmer against the British pound on Friday, with EUR/GBP up 1%, buoyed by lingering fiscal concerns and political turmoil in the UK following earlier-week developments. The pair found fresh momentum after BoE Governor Alan Taylor’s speech at the LSE, where he warned of heightened downside risks heading into 2026, citing fading inflationary pressures and economic slack. His call for more aggressive rate cuts added to the bearish tone for GBP.

Meanwhile, EUR/USD edged up 0.5%, not so buoyed as fundamentals turned against the common currency. Last week’s solid US labour market data tempered expectations for Fed easing, re-widening rate differentials in favour of the dollar and capping further sentiment-driven euro gains. With the July 9th deadline fast approaching, FX markets are likely to get noisy. Still, don’t expect EUR/USD to make a decisive break above 1.18 this week—unless trade tensions take a sharp turn for the worse, which we don’t currently anticipate.

On the data front, Eurozone inflation showed further signs of cooling on Friday. May’s Producer Price Index fell 0.6% month-on-month, easing beyond expectations and extending April’s 2.2% drop. Meanwhile, this morning saw Germany’s industrial production increased by 1.2% month-on-month after a 1.6% drop in April, signaling early signs of a cyclical rebound. The upswing was supported by stronger industrial orders and inventory drawdowns—but recent data suggests front-loading ahead of tariffs may have played a larger role, casting doubt on the sustainability of the recovery.

Looking ahead, attention turns to Eurozone retail sales today, which could reinforce the recent stream of soft data across the bloc. Yet, expect trade-related headlines to dominate the macro narrative into next week.

GBP rally on a knife’s edge ahead of “Liberation Day 2.0”

The British pound’s strong run – which has seen the GBP/USD up as much as 14% from its January nadir – came to a crashing halt last week as the Labour government’s political woes hit sentiment towards the UK currency.

The GBP/USD fell from four-year highs, with the pair losing 0.7% for the week, while sterling was lower versus most other key FX markets.

The GBP’s other major losses last week were in GBP/CAD, down 0.7%, and GBP/EUR, down 0.5%.

The British pound might face another tough week with financial markets more nervous ahead of Wednesday’s US tariff deadline.

US president Donald Trump announced a 90-day suspension of his tariff program that is due to expire on 9 July. Last week President Trump said a series of letters outlining the new tariff rules will be sent to trading partners on Monday.

While the UK and US have already struck a trade agreement, any increase in volatility across financial markets could hit the risk-sensitive British pound.

DXY holds up ahead of tariffs deadline

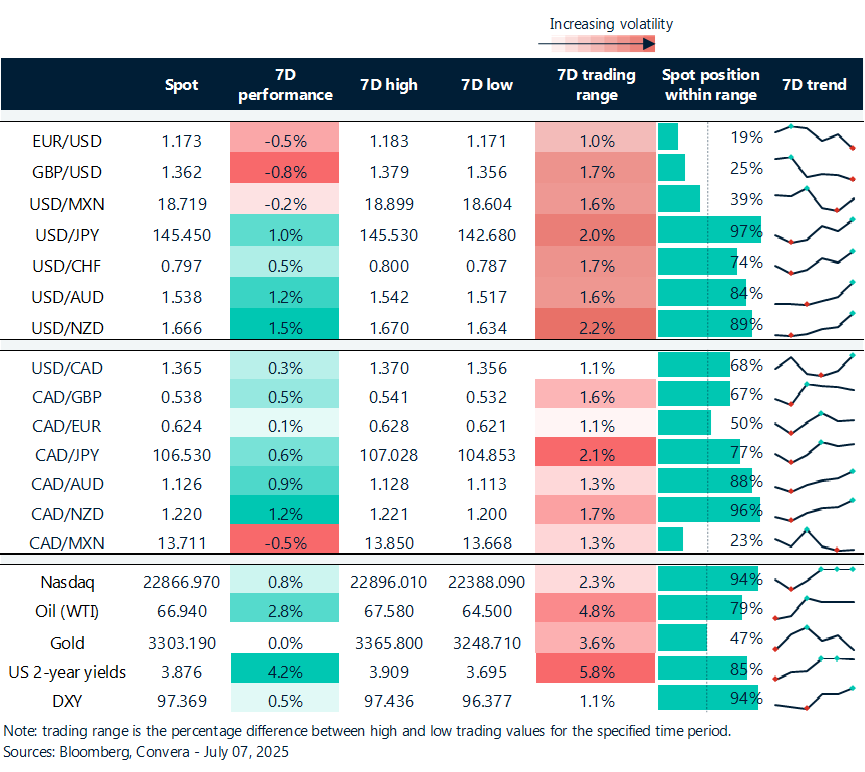

Table: 7-day currency trends and trading ranges

Key global risk events

Calendar: July 7-11

All times are in ET

Have a question? [email protected]

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.