Dollar steadies as crucial jobs data looms

Despite clocking its first monthly rise in three, the US dollar is on course to snap a six-week winning streak against major peers. The pivotal monthly US jobs report is the main focus today as it is likely to inform the path for Federal Reserve (Fed) policy over the near term.

The US currency has recently been weighed down by slumping Treasury yields, after a volatile week which has seen overall soft economic data temper the outlook for further Fed rate hikes. Two-year Treasury yields, which are particularly sensitive to rate expectations, have declined about 20 basis points this week to 4.86%, the biggest slide since mid-March. The latest rout in yields and the dollar has been in response to weaker second-tier data releases, which raises the odds of a deeper decline if we see the first-tier payrolls number disappoint today too. The consensus is looking for more signs of a cooling labour market, expecting a 170k payrolls increase. Individual forecasts range from 120k-230k. Wage growth is also seen decelerating somewhat to 4.3%, whilst the unemployment rate is expected to stay at 3.5%.

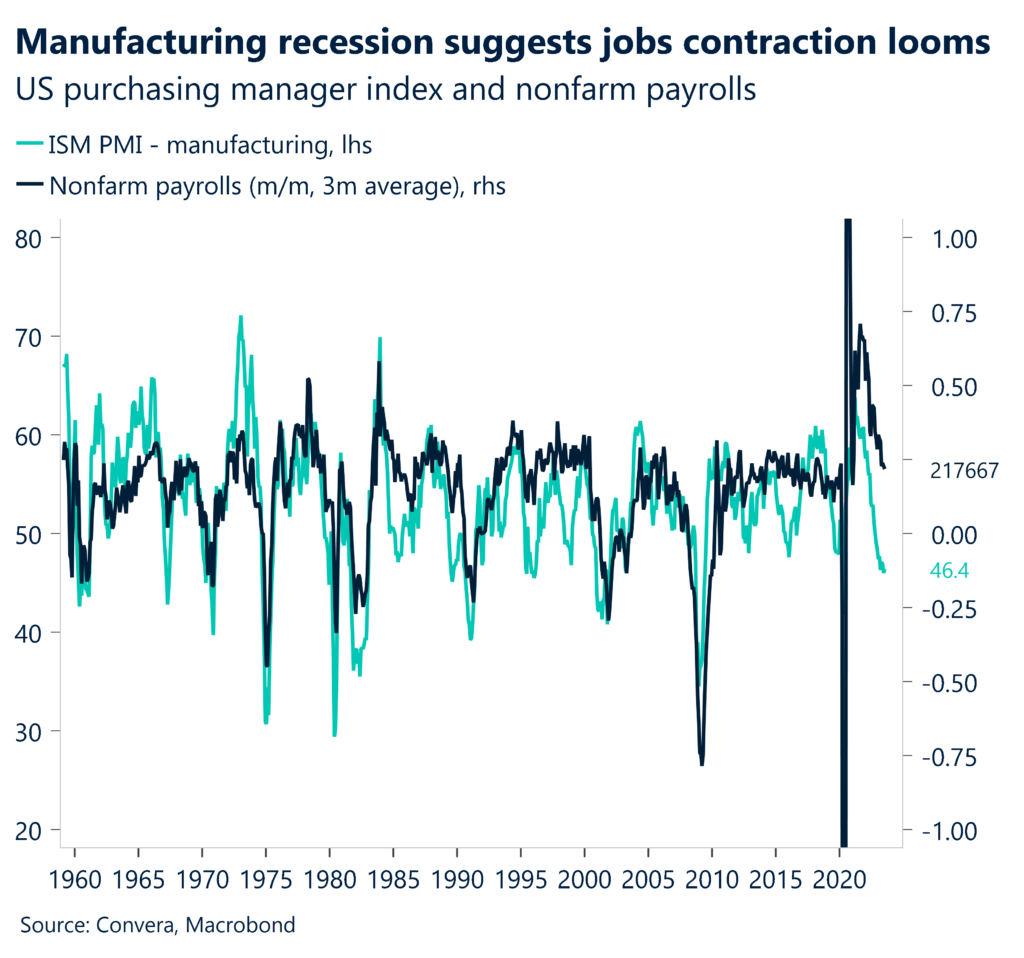

After the jobs data the ISM manufacturing index will be published, which is seen improving only marginally to 47, meaning that the index will continue languishing in the contraction area. This also indicates that the US labour market will continue cooling over the medium term, which raises the odds that the Fed has finished tightening.

Potential overpricing makes pound vulnerable

Seasonality trends held up for the pound during August as it depreciated against the US dollar. GBP/USD fell over 1% to log only its third monthly decline so far this year. The monthly chart set up looks bearish too, implying a softer start to September may unfold, particularly following the not-so-hawkish comments from Bank of England (BoE) policymaker Huw Pill.

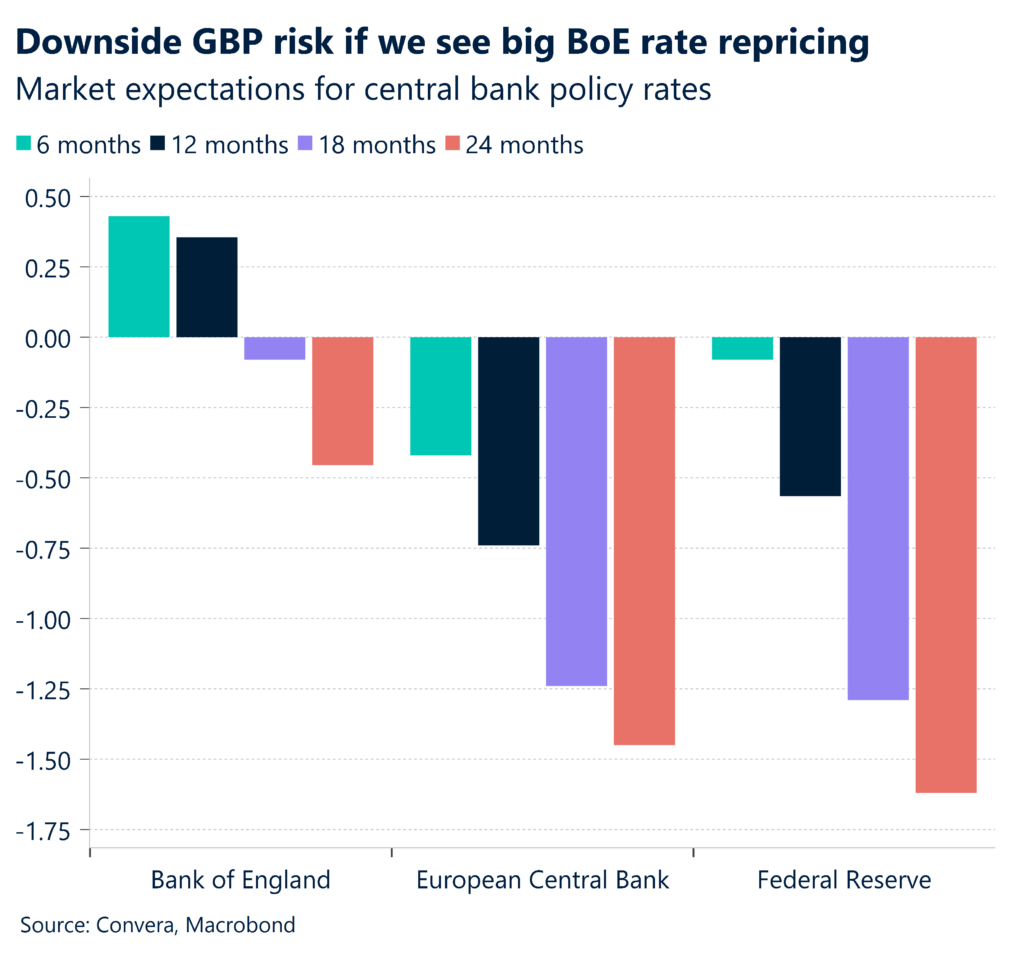

A keynote speech from the Chief Economist suggested he favours keeping the BoE’s Bank Rate at its current 5.25% or that only one more hike is necessary compared to current market pricing of at least two more hikes. But in a further rebuff to market thinking, he also underlined keeping rates at current levels for some time to ensure inflation does move back to target. More reflective of his usual hawkish tones he suggested that UK core inflation remains stubbornly high and doesn’t show any obvious decline. However, some of our leading indicators, as well as base effects, point to lower inflation in the short term. Couple this with further UK economic weakness suggests market pricing of BoE rate expectations is still too aggressive, which makes the pound vulnerable. While current yield spreads still suggest upside scope for sterling, this change of heart by Mr Pill, who has been on the hawkish side up till now, may limit the pound’s upside potential from here.

Against the US dollar, daily momentum readings have flipped to negative, and the relative strength index has turned lower. A break of the 100-day moving average support could open the door to test $1.25 this month. Meanwhile, after Eurozone inflation data, GBP/EUR has looked poised to test €1.17 again after its biggest two-day rally in over two weeks, yet the currency pair has started today on the softer side.

Markets betting against the ECB

The euro is looking to finish the week in green territory for the first time since the beginning of July. However, the pace of this week’s appreciation has definitely slowed as markets start doubting the ECB’s willingness to tighten monetary policy further against the backdrop of disinflationary forces mounting. EUR/USD is positioned slightly above the $1.08 mark with investors focusing in on US jobs and PMI data.

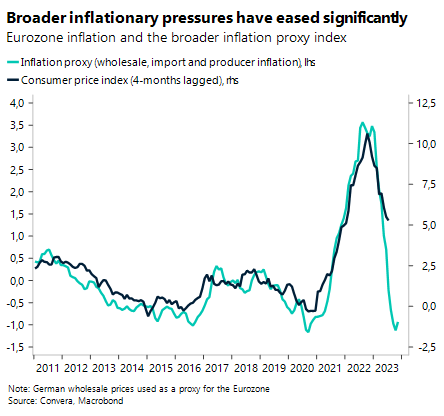

Eurozone inflation did prove more stubborn than economists had expected in August. Consumer prices remained unchanged at 5.3%, defying expectations of a drop to 5.1%. Markets still revised down their rate hiking bets for September from 50% to less than 30%, following the fall of core inflation from 5.5% to 5.3%. This can be explained by the expected medium-term trajectory of European inflation.

While this individual report has been worse than expected for the ECB, it should be the last one where base effect contributed positively to price growth. Starting from September, disinflationary forces should continue to pull down headline and core CPI. However, nothing is set in stone. The most hawkish members of the Governing Council are still pushing for rate increases with Robert Holzmann even seeing two hikes as a possibility.

GBP/EUR near top of recent trading range

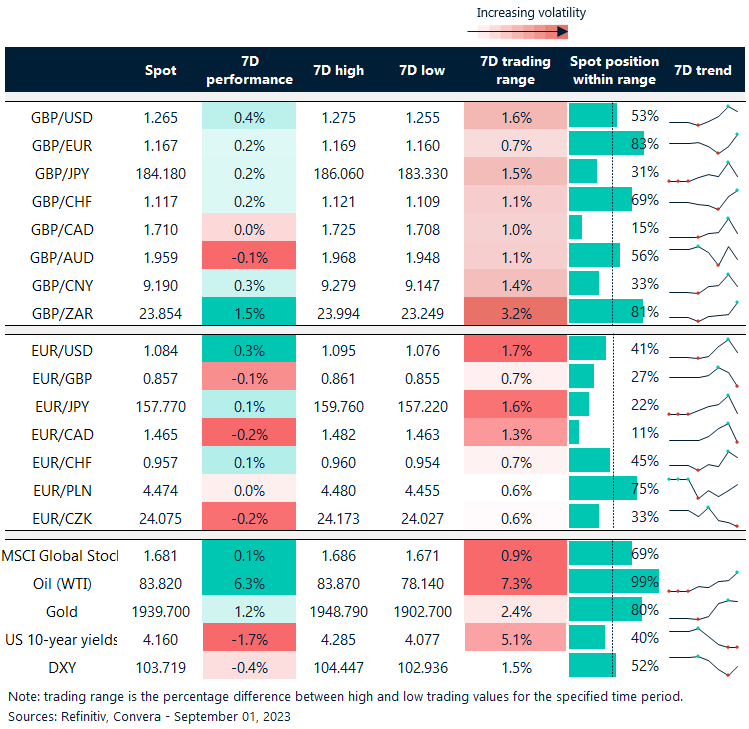

Table: 7-day currency trends and trading ranges

Key global risk events

Calendar: August 28-Septemeber 01

Have a question? [email protected]

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.