Global overview

Safer currencies mostly outperformed Monday in cautious trade following a weekend revolt in Russia. The U.S. dollar was little changed versus the euro, sterling and Canadian dollar but struggled against counterparts from Japan and Switzerland. Markets were already in an anxious mood as rising lending rates around the world stoked pessimism about the outlook for global growth. Risk sentiment turned more cautious after a short-lived weekend uprising in Russia where mercenary forces led by Yevgeny Prigozhin’s Wagner group momentarily took over the headquarters of Russian troops. While the armed rebellion has been suppressed for now, uncertainties remain, keeping geopolitical instability elevated. The dollar index is coming off its first weekly advance of the month as expectations of more rate hikes around the world fan worries over global growth. The final week of June and the second quarter features data on U.S. and Canadian growth and late week numbers on U.S. consumer spending and inflation.

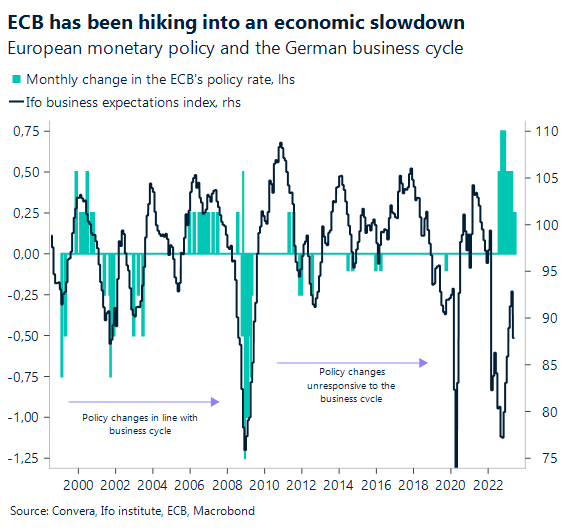

Germany business confidence darkens

The euro was little changed as it struggled for direction after data offered fresh signs of a sputtering German economy. Germany’s influential Ifo survey of business confidence deteriorated for a second straight month when it slipped to 88.5 in June from a downgraded 91.5 in May, missing forecasts of a decline to 90.7. The weaker than expected outcome increases the likelihood that Europe’s biggest economy contracted for a third consecutive quarter in the April-June period.

Stronger UK pound suffers a setback

Sterling seesawed to begin the final week of the first half as markets weighed Britain’s higher rate outlook against expectations for lower growth. GBP/USD fell for the first time in four weeks as the Bank of England’s 13th straight rate hike, a half-point bump to 5%, the highest in 15 years, dampened expectations for the UK to dodge recession this year. Risk-off sentiment stemming from instability in Russia kept sterling on shaky ground to kick off the last week of the second quarter.

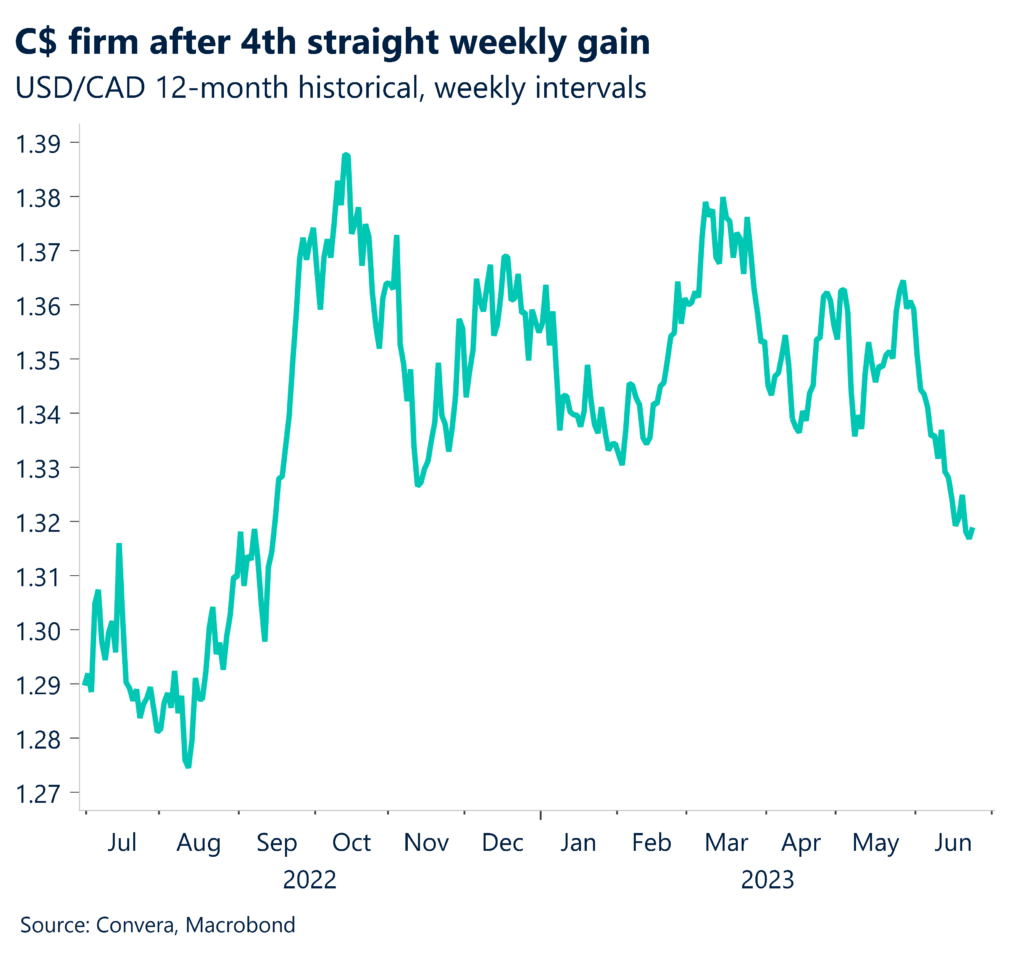

C$ remains buoyant ahead of data

Canada’s dollar hovered near nine-month highs against the U.S. dollar ahead of domestic data this week that’s forecast to show lower inflation and higher growth. Canadian consumer inflation Tuesday is forecast to cool to a 3.4% annual rate in May from 4.4% in April. Canada Friday issues monthly growth that’s expected to show the economy grew 0.2% in April after it flatlined in March. Outcomes that are generally in line with expectations would keep the Bank of Canada on track for another loonie-positive rate hike from 4.75%, the highest in 22 years, as soon as mid-July.

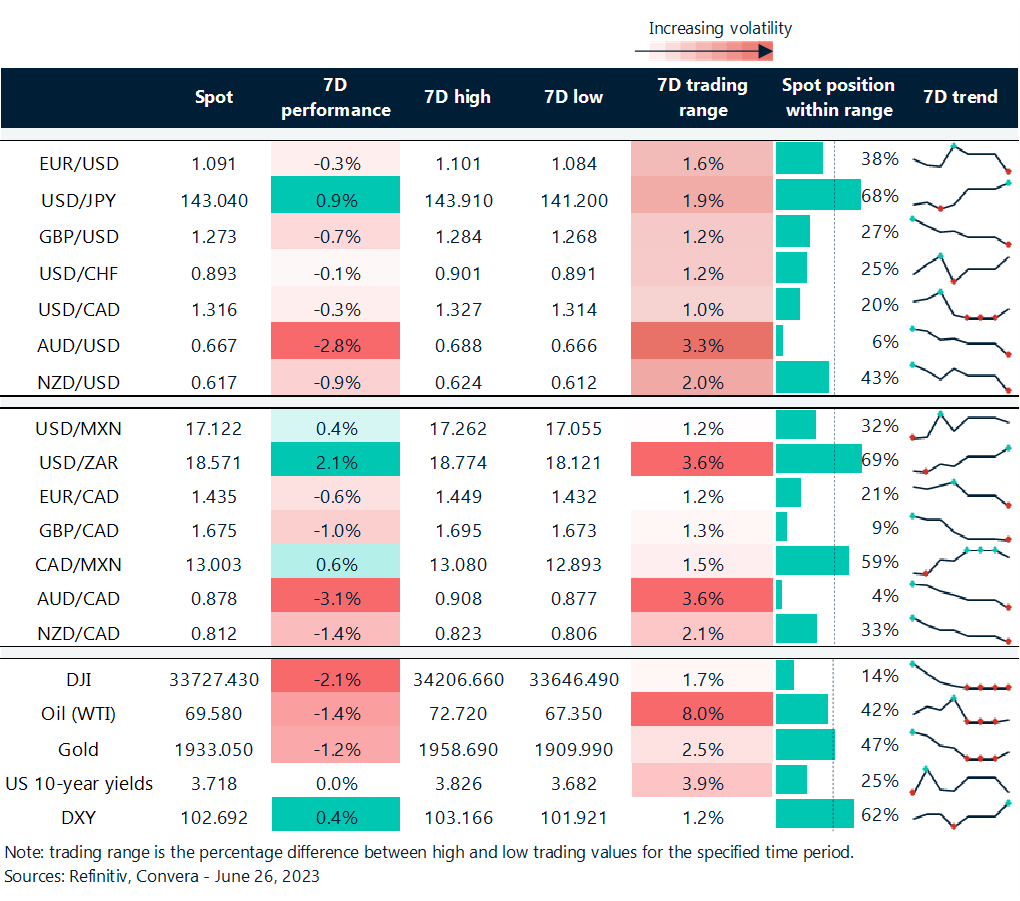

Dollar near upper end of ranges

Table: rolling 7-day currency trends and trading ranges

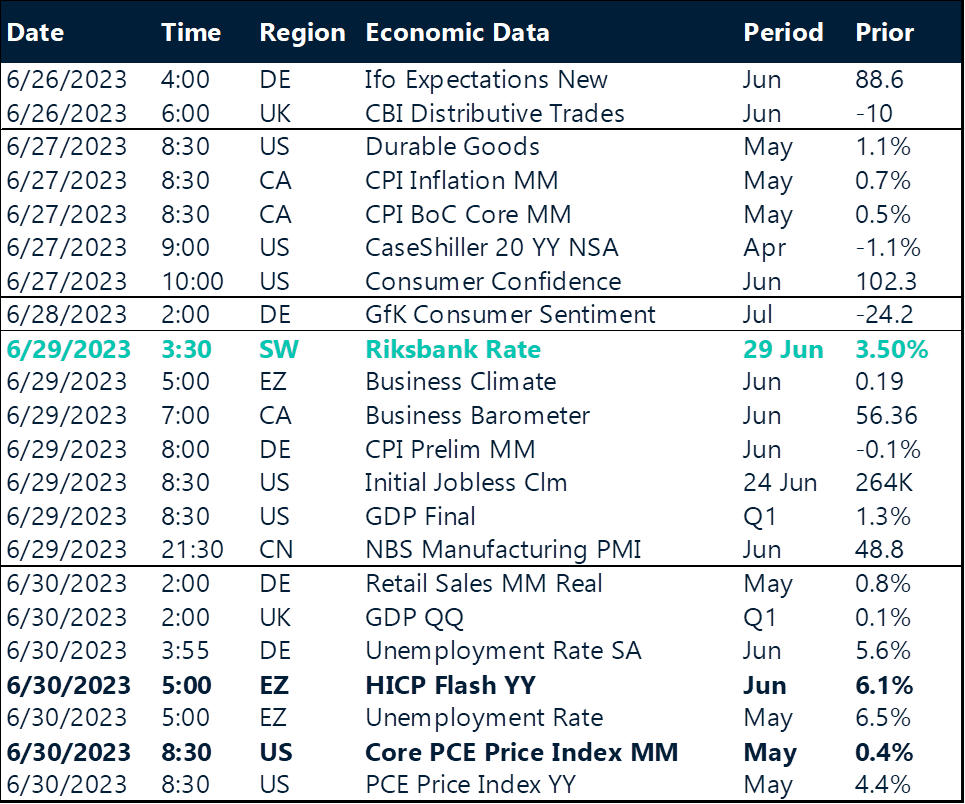

Key global risk events

Calendar: Jun 26-30

Have a question? [email protected]

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.