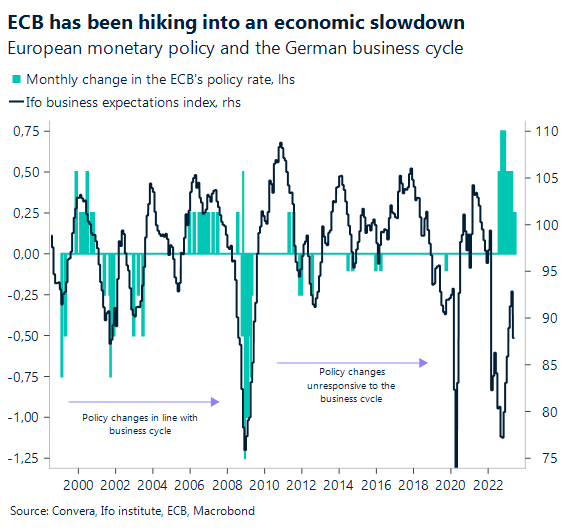

German manufacturing falls deeper into recession

German manufacturing activity fell to its second-lowest level since the Global Financial Crisis in June, just a week after the European Central Bank (ECB) increased its benchmark deposit rate to a 22-year-high. The upcoming inflation reading on Friday might show that underlying price pressures remained near record levels, showcasing the dilemma of high inflation and faltering economic growth policymakers are facing right now.

The weaker-than-expected purchasing manager indices for Germany and France dragged down the European PMI deeper into negative territory. Eurozone manufacturing fell by 1.2 points to 43.6 in June, the sharpest contraction in three years. The composite index, indicating the level of activity in the overall economy, did manage to stay above the important 50 mark in Germany and the Eurozone. However, the readings of 50.8 and 50.3 did not indicate that the recession of Q1 will be followed by a sharp rebound in the next quarter or two. New orders dropped for the first time in five months, and input costs rose by the least since December 2020. While the European inflation print for June, due on Friday, might be higher than the month before, recent soft and leading indicators continue to point to weaker price pressures going into the second half of the year.

This is why the euro reacted so negatively to the PMI release just before the weekend. Markets had cut their rate expectations for the ECB in response to the recent data and now see an 80% probability of a hike in September in addition to the fully priced in increase in July. German 2-year Bund yields fell by the most in a month, ending the flat at around 3.17%. EUR/USD followed suit, after having risen to the highest level since the beginning of May at $1.1020 during the week. The currency pair currently trades at around $1.0890. The upcoming data out of Germany – Ifo business index, Gfk consumer expectations and retail sales – will be crucial for the common currency, as it searches for new momentum post-PMI.

Weak PMI puts the spotlight on PCE

Equity markets across the globe ended the week lower on Friday after the mixture of hawkish central bank speeches and disappointing PMI numbers on Friday left investors uncertain about the near-term outlook for the global economy. The S&P 500 had recently touched the highest level since May 2022 at 4450 points, after having risen by 26% since October, but has fallen by 2.2% in the last two weeks.

The rally in risk assets had split Wall Street analysts into two camps, as most of the returns had been generated by large cap technology stocks. The capital reallocation into stocks had even occurred against the backdrop of bonds broadly pricing in a higher for longer scenario following a plethora of hawkish central bank speeches and rate decisions across the developed world. The US dollar is currently negatively correlated to stocks and therefore found it harder to strengthen amidst the risk asset appreciation. However, the weaker-than-expected purchasing manager index, showing that US manufacturing stayed in contraction for the seventh consecutive month, pushed the trade weighted dollar to its first weekly appreciation in a month.

While upcoming data will be scarce for the US, investors will be focusing on inflation numbers on Friday. Gauging the probability of a recession occurring in the next 12 months remains difficult, as lagging indicators remain resilient to the continued deterioration of leading indicators. The release of the PCE price index will be important as markets push back against the FOMC’s forecast of two more rate hikes in 2023 and no cuts in the following year, with investors pricing in the end of the tightening cycle to occur in July and first cuts to be implemented in 2024.

Strong pound to falter as recession fears rise

GBP/USD is hovering above $1.27 this morning after having slipped from a 14-month high of around $1.2850 last week as investors grow increasingly concerned about the possibility of a UK recession following the Bank of England’s (BoE) significant interest rate hike. GBP/EUR also suffered its worst week in ten but is finding support at its 100-week moving average this morning.

Investors have been analysing a range of economic data. Surging wages and sticky inflation has prompted bets of UK interest rates reaching 6% this year, but evidence of a slowing economy is starting to raise recession fears. Normally, when a G10 major central bank opts for a jumbo rate hike of 50 basis points, you might expect a jump in its currency’s valuation. But the fact that the pound came off its peaks is just a reflection of recession fears. The latest PMI surveys on Friday indicated a sharp slowdown in UK business activity growth in June, driven by a moderation in service sector growth, a deeper contraction in manufacturing, and persistent inflation pressures. This week is pretty light on UK economic data, so sterling will likely take cues from global risk sentiment and the global rates outlook.

Despite the recent downturn in the pound versus many peers, it remains the best performing G10 currency year-to-date though, and is up on average 7.6% against 57 of the world’s currencies. Against its one-year average rates, GBP/EUR is over 1% higher, whilst GBP/USD is over 5% higher.

Mixed picture amid wavering sentiment & global rates outlook

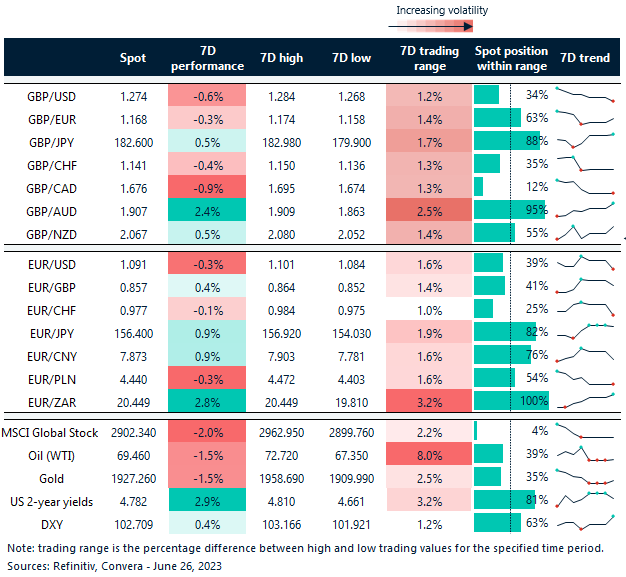

Table: 7-day currency trends and trading ranges

Key global risk events

Calendar: June 26- June 30

Have a question? [email protected]

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.