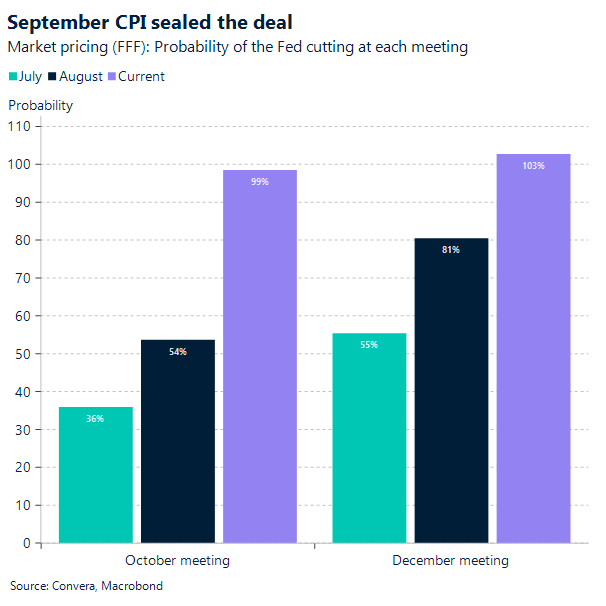

USD: Dollar holds up on rate cut expectations

After weeks of a government shutdown, we’ve finally received the belated key piece of economic data, which turned out to be less pessimistic than anticipated. The report almost certainly points to another rate cut from the Federal Reserve this week. Both the headline and core 12-month CPI changes came in slightly below forecasts at 3.0%, a reading only seven out of 76 economists in the Bloomberg survey had predicted for the core number. While the 4.1% rise in the gasoline index in September was a significant contributor to the monthly bump, the softer overall readings spurred a predictable market reaction: the Dollar Spot slightly dropped, Treasuries rallied, and both the S&P 500 and Nasdaq 100 jumped up. This data also provides a boost to the administration, supporting their argument that inflation is under control and that tariffs aren’t causing a surge in the cost of living.

Although inflation is running at 3.0% on a 12-month basis, still well above the long-term 2% target, the Fed is clearly prioritizing the labor market. Unfortunately, the good news on inflation could quickly become bad news for job growth. Downside risks to employment are increasing as companies look for ways to offset rising input costs from tariffs, potentially leading to layoffs.

The September CPI report also contained an important signal that should give the Fed more flexibility: housing prices are reaching multi-year lows. The owners’ equivalent rent (OER), a key proxy for housing prices, rose only 0.1% in September, its slowest pace since 2020. This reduced pressure on a major component of inflation offers the Fed more room to maneuver.

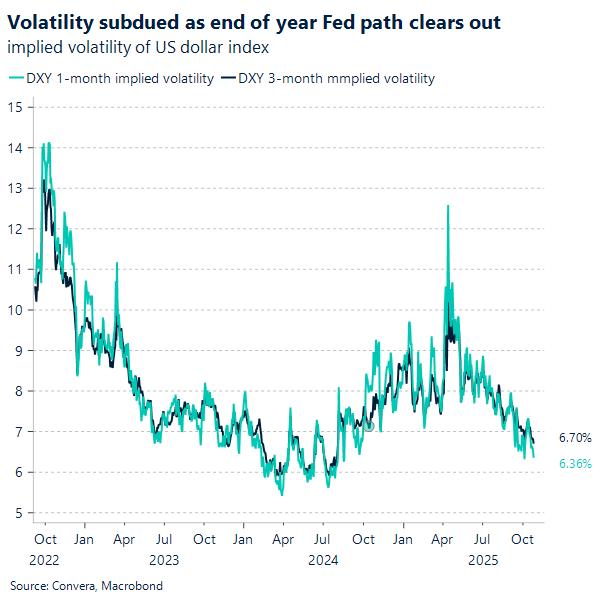

Despite these signals, the reaction in the foreign exchange market was notably subdued, failing to deliver the volatile move many had expected. This is consistent with the overall low volatility that has characterized the currency market this week, with the DXY staying within one standard deviation of its average about 80% of the time over the past three months.

It’s important to note that even with markets consistently pricing in two rate cuts this year, the US Dollar hasn’t moved substantially lower. Another significant drop seems conditional on an extreme deterioration in the labor market, which simply isn’t the case right now. Given this, the upcoming Fed meeting is now looking relatively unsurprising, with more questions likely to surround the Fed’s long-term ability to accurately assess the economy without reliable, timely data.

CAD: Trade talks ended, and a +10% tariff increase

It seems almost surreal. President Trump ended trade talks with Canada, after Doug Ford, Ontario Premier created an ad campaign criticizing the U.S. President. Trump explicitly blamed the ad, which controversially used the late President Ronald Reagan’s words to criticize U.S. tariffs. After all what’s unfolded this year, and in the middle of crucial negotiations, deliberately upsetting Canada’s largest trading partner through an ad, doesn’t seem like the smartest strategy.

Contrast that with Mexico. The trade partner south the border isn’t allowing local governors to run policy attack ads in the U.S. that will cause to anger tariff-man. In fact, they seem to be aligning more closely with President Sheinbaum’s focus on diplomatic efforts. During the weekend, the Canadian government has vowed to take down the ad so trade talks can resume. However, on Saturday, Trump said he is increasing tariffs on Canada by an additional 10%, “above what they’re paying now.”, as Trump mentioned on social media.

While Canada absolutely needs to diversify away from the U.S., as PM Carney has reiterated recently, the Canadian government also needs to maintain a very careful approach leading up to CUSMA renegotiations. The move from the Ontario premier, and subsequent backpedaling, only proves Trump right when he claims that the Canadian government doesn’t have the cards to play this tit-for-tat trade game.

Maybe Trump will backpedal again, as we’ve seen him consistently do this year. Some may also argue that this move to cut trade talks and increase the tariff rate by an additional 10% comes just to destabilize PM Carney ahead of the Federal budget announcement on November 4. Regardless, the news guaranteed local upheaval and discomfort with the government. To make matters worse, U.S. auto companies have already pledged to cut investments and close some plants in Southern Ontario, planning to relocate to the U.S. Talk about terrible timing.

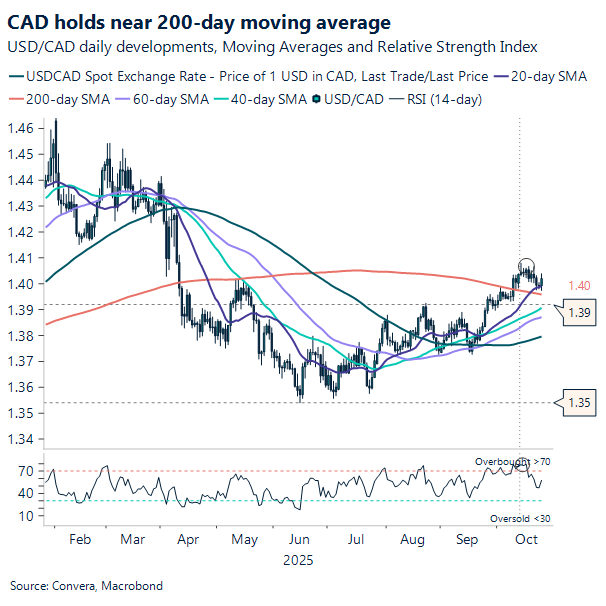

The Loonie tumbled immediately after President Trump announced the end of trade negotiations. However, it has ended the week wobbling around the 1.40 level.

Apart from politics, attention will now shift to the central banks, with the Bank of Canada (BoC) playing the opening act before the Federal Reserve this Wednesday. The BoC’s decision holds the only real suspense. Although markets are pricing in a rate cut, the move doesn’t appear justified when looking at the latest CPI data. Core, headline, trimmed, and median CPI all jumped higher than expected. While some may argue this was primarily due to base effects, the reality is that the bounce in CPI was broad-based. The BoC may opt to hold rates now and cut in December, which would still give the economy needed support while they wait for more data on how entrenched inflation is becoming. A pivotal meeting lies ahead.

MXN: Consolidation continues

The Mexican peso continues to trade within a relatively narrow range, but with a pattern of gradually higher highs, now approaching the 18.50 level. However, despite repeated attempts to break above the 50-day Simple Moving Average (SMA), the Mexican Peso has remained below this key medium-term trend indicator since April. There’s been broader weakness in emerging-market currencies, which briefly extended losses following a Reuters report that the Trump administration is considering restrictions on exports to China involving U.S.-origin software.

The USD/MXN pair, which had posted strong year-to-date gains on the back of robust carry trade appeal, has now entered a phase of choppy, sideways consolidation around the 18.40 mark. While recent geopolitical tensions, including the U.S.-China trade spat, briefly pushed the Peso higher, its retreat reflects a return to low-volatility trading, with support from Mexico’s solid macro fundamentals and interest rate differential likely keeping the pair range-bound in the near term. For the short-term, the USD/MXN is expected to continue this range-bound crawl, holding year-to-date gains at 12%.

The Fed’s meeting this Wednesday is unlikely to be a major market catalyst—unless Chair Powell delivers another hawkish surprise, dampening expectations for a year-end rate cut.

FX relatively calm after a softer US CPI reading

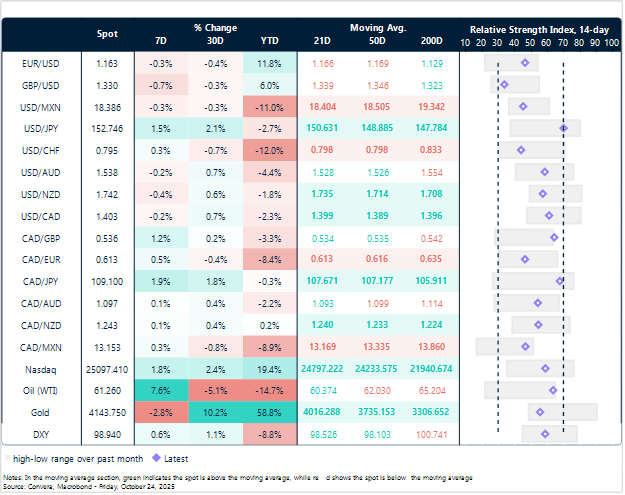

Table: Currency trends, trading ranges and technical indicators

Key global risk events

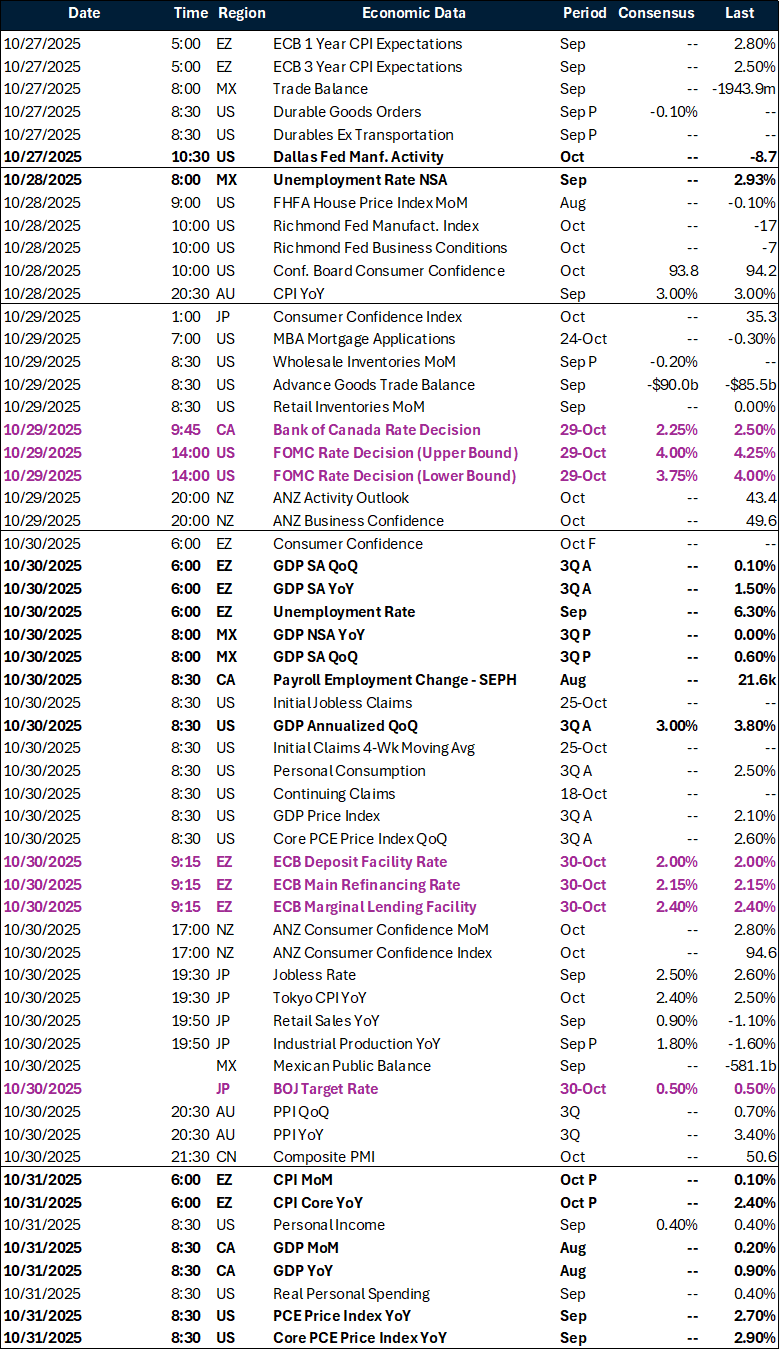

Calendar: October 27-31

All times are in EST

Have a question? [email protected]

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.