Fed pauses, but promises more rate hikes

The Federal Reserve left its benchmark policy rate unchanged at 5-5.25% for the first time since starting its tightening cycle, after having raised the fed funds rate ten consecutive times. The Fed’s updated projections showed that policy makers expect to raise the policy rate two more times this year, and that June has to be seen as a skip rather than the end to the Fed’s fight against inflation.

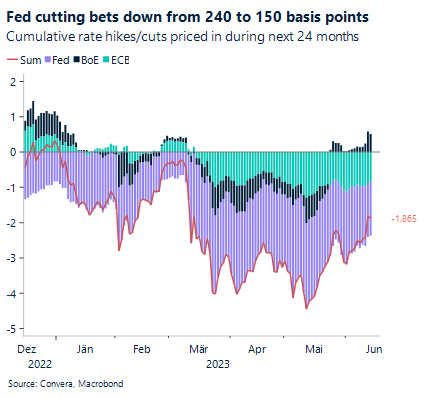

However, with inflation and economic activity set to continue slowing into the second half of the year, it will be difficult for the Fed to deliver on its promise to increase rates two more times. Markets now put the probability of a single hike in July at 70% and all rate cuts for this year have been successfully priced out. So, while investors remain skeptical about the extent of future tightening, Jerome Powell has been able to fend off bets about premature easing. Given the extreme data dependence of central banks at this stage of the policy cycle, incoming data will continue to play a major role in gauging what the Fed will do next.

The probability that the United States falls into recession, according to the New York Fed, has jumped to 71%, the highest level since the 1980s. The last five tightening cycles have all pushed the US into consecutive contractions, and bond investors continue to see this as a plausible possibility. The policy sensitive 2s/10s yield curve inverted to -90 basis points following the rate decision, indicating a level of uncertainty about the economic outlook.

China going against the monetary tide

A string of disappointing Chinese macro data has led the central bank to lower its one-year medium term lending facility rate by 10 basis points to 2.65%. The first easing measure since August, while more symbolic than anything else, does suggests a shift in tone from the Peoples Bank of China and comes just hours before official data showed economic activity weakened more than expected in May.

Industrial production, retail sales and fixed asset investment all surprised the consensus to the downside, suggesting that the second quarter will see a significant slowdown in economic growth compared to the consumption driven rebound in Q1. Retail sales increases by 12.7% year-on-year in May, from the previous 18.4% expansion in April, recording the first yearly fall since November of last year. Fixed investments grew by 4% in the first five months of 2023, setting the slowest pace since 2021. These data points suggest that more stimulus from Beijing might be on the way. Economists expect the PBoC to deliver further rate cuts in addition to targeted fiscal stimulus from the government being prepared.

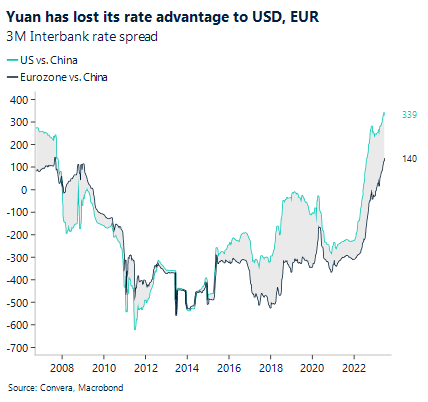

This stands in stark contrast with the United Kingdom, Eurozone and US, where monetary policy is growing more restrictive by the month. Following the events of the Global Financial Crisis and the ultra-easy monetary policy of the Federal Reserve, a negative US-CN rate differential became the norm during the last decade. However, the simultaneous bottoming of spreads and the exchange rate between 2012-2014 has been followed by a continued recovery of both indicators. At the end of last year, the 3-month interbank rate in the US and Europe surpassed the one in China for the first time since 2008. Since then, the monetary tightening of the Fed and ECB has continued, putting upward pressure on rate differentials and the exchange rate alike

Dollar not as weak as expected

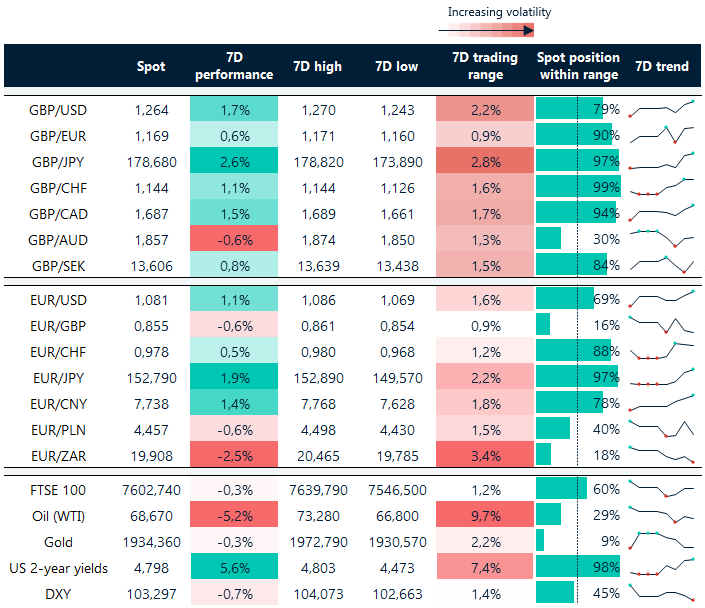

EUR/USD is on its way to record the second weekly appreciation in a row, after having jumped above $1.08 following the FOMC meeting. However, the gains for the common currency have been limited as markets have priced out all rate cuts for 2023, suggesting that the higher for longer rate environment could cushion the dollars blow in the short term. GBP/USD briefly touched a new 13-month high, reaching the $1.27 mark, but as with the Euro, some selling pressure in the early European session pushed the pair down to $1.2650 again.

Both the European Central Bank and Bank of England are expected to hike rates further this year, while the Federal Reserve inspects the damage the tightening cycle has done to the US economy. The consensus still sees a weaker dollar going into the second half of the year based on rates having peaked or being close to peaking in the US. However, while we do expect the effects of tighter lending conditions and the manufacturing recession to put pressure on the labor market and broader economy, the European and British economies face the same headwinds.

Inflation is rapidly falling in the Eurozone and the common region has already fallen into a recession. Economists expect the monetary divergence favoring the ECB and BoE vs. the Fed to come from the fact that inflation is coming down quicker in the US, not from a real divergence in the strength of the respective economies. Incoming data will show how if these consensus assumptions can stand the test of time. For today, we will be closely watching the rate decision in Europe, where the ECB is expected to rate its benchmark policy rates by 25 basis points.

EUR/USD $1.08 and GBP/USD $1.27 in focus

Table: 7-day currency trends and trading ranges

Key global risk events

Calendar: June 12- June 16

Have a question? [email protected]

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.