Written by George Vessey & Boris Kovacevic

Check out our latest Converge Podcast episode: When milliseconds matter: Preventing fraud in an instant payment world by Converge

Fed has confirmed the higher for longer narrative

Risk off sentiment is dominating global markets this morning after the Federal Reserve (Fed) signaled there might be more interest rate increases coming this year. While the US central bank left its policy rates unchanged at a 22-year high (5.25%-5.5%) at yesterday’s meeting, the FOMC’s rate projections in the form of the dot plot showed one more rate increase happening this year and only two rate cuts penciled in for 2024.

The upside revisions to both GDP and inflation forecasts are supporting the Fed’s thesis of a higher for longer regime, which has been slowly priced back into market pricing, supporting the dollar, while dragging down risk sensitive assets. While markets do not agree with the Fed that policy is going to be tightened again, investors have come to terms with the fact that less easing will be happening next year. The first rate cut has been pushed back from March just some months ago to July 2024. The central bank’s economists are implicitly forecasting a soft landing with GDP and inflation cooling in 2024, but not enough to cause a recession. However, when asked about the likelihood of such a scenario, chair Jerome Powell said that a soft landing is still not the baseline.

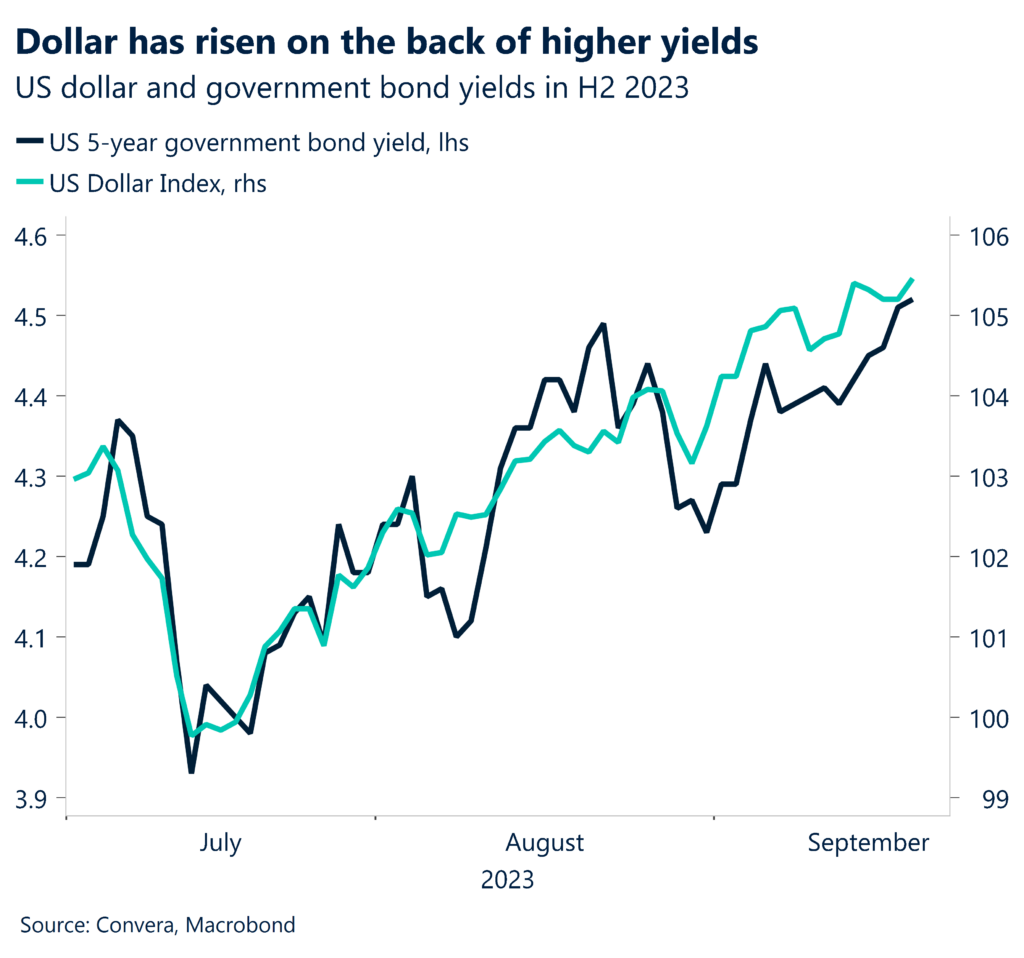

The Fed’s pushback against any premature easing has helped the dollar recover its early weekly losses with the US Dollar Index set to record its tenth consecutive weekly gain. The higher for longer narrative has gripped markets and investors have tried to keep up with the hawkish Fed rhetoric by pushing up the long end of the yield curve. Ten-year government bond yields have risen for five months now and are at the highest level since 2007.

Pound drops as BoE unexpectedly halts run of rate hikes

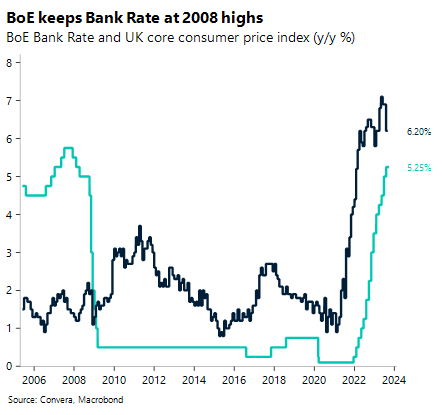

The Bank of England (BoE) has held interest rates at 5.25% after a knife-edge vote that is likely to signal the peak of borrowing costs in this cycle. Following better than expected inflation data in August, the bank’s Monetary Policy Committee (MPC) split five to four in favour of leaving rates unchanged, with Andrew Bailey, BoE governor, casting the final and decisive vote.

Markets were pricing a 50% chance of a 25bps hike and a 50% chance of a hold. A 5.5% peak rate was also the base case. However, markets are no longer fully pricing in another hike, and this has dragged GBP/USD to fresh 6-month lows.

In the short term, GBP has tended to fall following BoE decisions. On average, GBP/USD has dropped 0.9% from the Wednesday close to the Friday close wrapped around the Thursday decision. Long term GBP outlook remains uncertain given recession risks and financial stability concerns (risk off = GBP negative) versus global rate cutting expectations and rallying equities (risk on = GBP positive).

ECB now expected to lead the easing cycle

Global investors are still digesting yesterday’s rate decision by the Fed and have naturally not paid too much attention to developments in Europe. While both the ECB and Fed are now finally expected to be done with their respective tightening cycles, only US policymakers have built a compelling case about not needing to cut rates in the early 2024. Economic growth has been weakening in Europe and inflation, while coming down slower than expected, is set to continue falling from September onwards. Adding China’s reluctance to add too much stimulus to its stuttering economy has not been a good mixture for risk prone assets like the euro.

ECB Governing Council members have not been able to support the interest in the common currency so far. While policymakers have pushed back against the idea of the ECB needing to cut rates in the coming quarters, some of the comments were sending mixed messages. Historically, both the ECB and Fed have only held rates at their local peaks for a short period of time. This is why markets are pricing in rate cuts as soon as central banks are finished raising rates. With European policymakers talking about being done tightening monetary policy, the focus has shifted to the question of when the ECB will succumb to the economic weakening and start easing policy.

EUR/USD ($1.0640) has consequently fallen to the lowest level since March and is now down 5.6% from its peak reached in July at $1.1270. We have been right in pointing out the euro’s overvalued positioning above the $1.10, and following the weaker macro data surprises, the $1.08 levels. However, with markets now expecting the ECB (June) to start cutting rates before the Fed (July) and China slowly starting to add some stimulus to the economy, the currency might be prone to react less negatively to data misses. In the short-term, however, positive catalysts are missing.

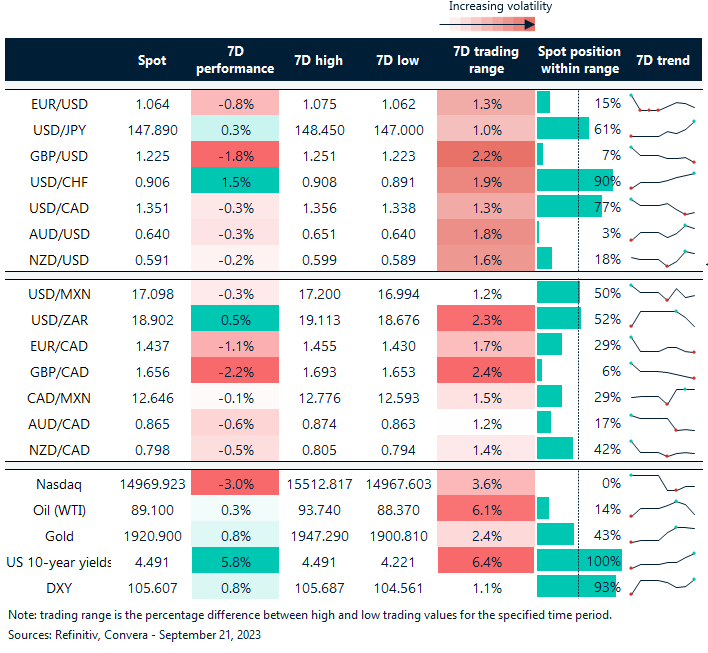

GBP/USD down 1.8% in a week after BoE pause

Table: 7-day currency trends and trading ranges

Key global risk events

Calendar: September 18-22

Have a question? [email protected]

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.