Written by Steven Dooley, Head of Market Insights, and Shier Lee Lim, Lead FX and Macro Strategist

Fed hike hopes start to evaporate

The US dollar extended gains overnight as the US’s key short-term bond market, the two-year bond yield, rebounded back to 4.00% after trading as low as 3.50% in late September.

US bond yields have been pushed higher by stronger data, most notably, last week’s super-charged September non-farm payrolls report that came in at 254k versus the 150k expected.

US markets now see less than two 25-basis point cuts from the Federal Reserve for the rest of the year – down from three cuts in mid-September.

Market volatility was also higher with the benchmark volatility index VIX, the so-called “fear index”, closing at 22.6, the highest level since 8 August – during the Japanese yen-inspired global mid-year sell-off.

In FX markets, higher US bond yields provide support for the greenback, with the USD index steady at two-month highs.

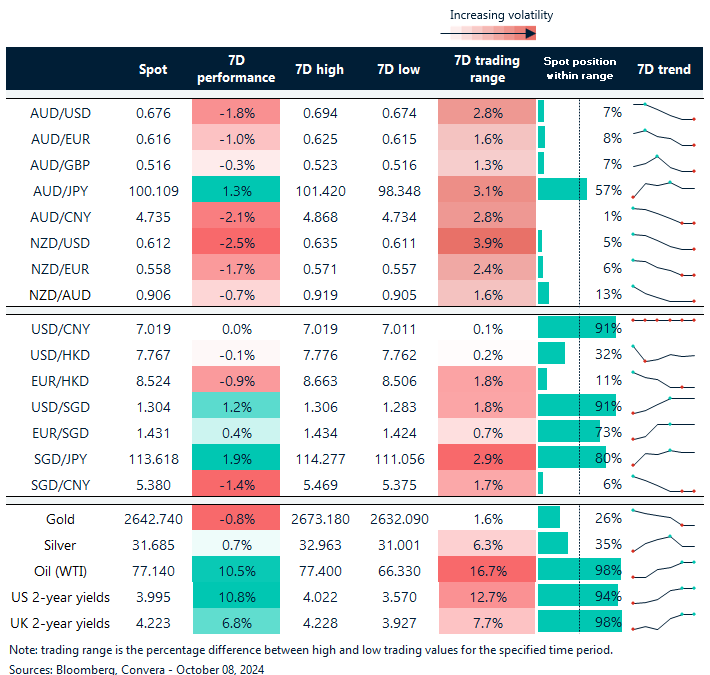

The Aussie and kiwi took the largest losses overnight with the AUD/USD and NZD/USD both down 0.6%. Both currencies lost ground in other major markets.

The USD/CNH fell 0.4% ahead of a big day for Chinese markets, resuming after a week-long national holiday.

Chinese shares had surged higher into the break, with the Shanghai Composite up 28% in less than two weeks, on a series of announcements about stimulus measures.

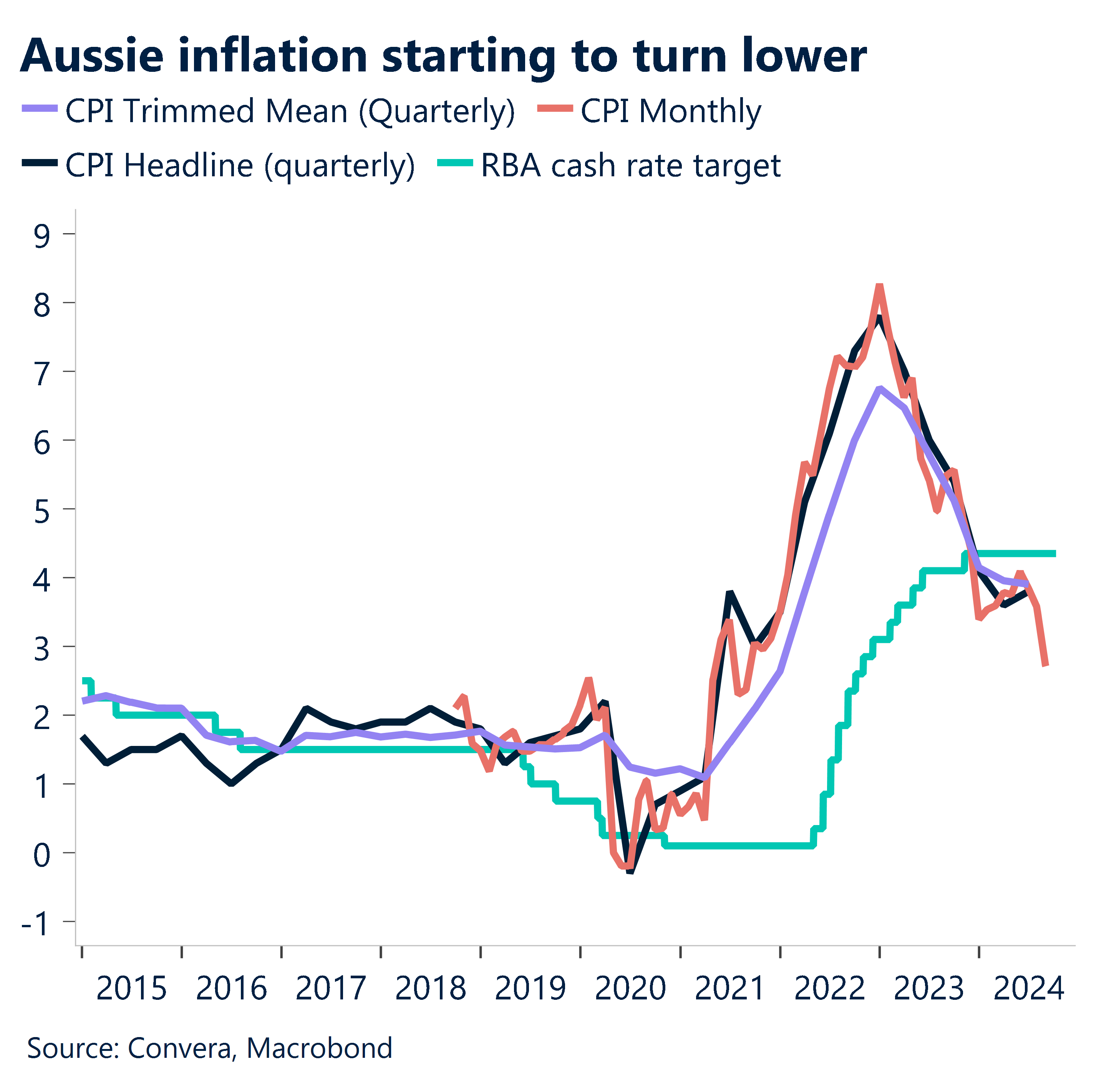

Aussie in focus ahead of RBA comments

The Aussie’s overnight moves saw the AUD/USD fall back to one-month lows.

The Aussie was pressured across markets with the AUD/EUR down 0.6% as it turned from 15-month highs and the AUD/GBP down 0.4% as it fell from three-month highs.

The AUD/JPY turned sharply from two-month highs.

For the Aussie, key releases today include the Reserve Bank of Australia minutes at 11.30am and a speech from RBA deputy governor Andrew Hauser at 12.00pm (AEDT).

Euro tests support after sharp decline

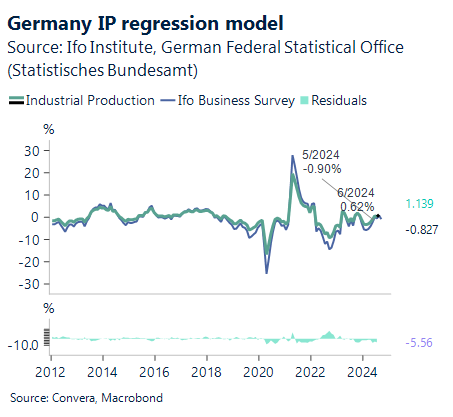

The euro has recently weakened as disappointing European data has weighed on the currency.

Coming up, we’re looking for Germany’s industrial slump to continue in August; we predict industrial production to decrease by 0.6% m-o-m.

In this case, Germany’s GDP growth in Q3 2024 would be -2.6% quarter over quarter, or -0.8 percentage points worse, confirming our conclusion that the country is experiencing a recession.

From the 1.125–1.1294 resistance zone, EUR/USD had dropped precipitously to test the 1.093–1.0981 support zone, just above the 200-day EMA.

In the short run, the pair might stabilize at this point and remain inside the Aug–Oct trading range.

An extended decline below 1.09 and back into the previous 2024 trading range would indicate a significant technical development that, in the longer run, might result in much more downside for the euro.

Aussie, kiwi feel the pinch

Table: seven-day rolling currency trends and trading ranges

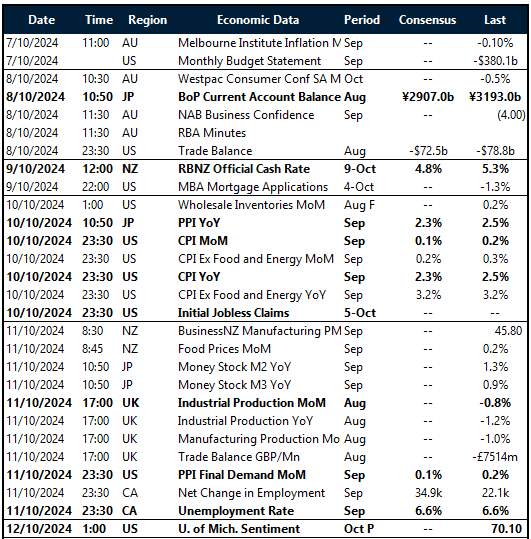

Key global risk events

Calendar: 7 – 12 October

All times AEST

Have a question? [email protected]

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.