Written by Steven Dooley and Shier Lee Lim

Check out our latest Converge Market Update Podcast as volatility across assets remains low despite the ambiguity surrounding the future policy path of central banks. What’s driving this low volatility? The synchronization of policy pricing. Join our macro analyst Boris Kovacevic as he breaks down this week’s global market news.

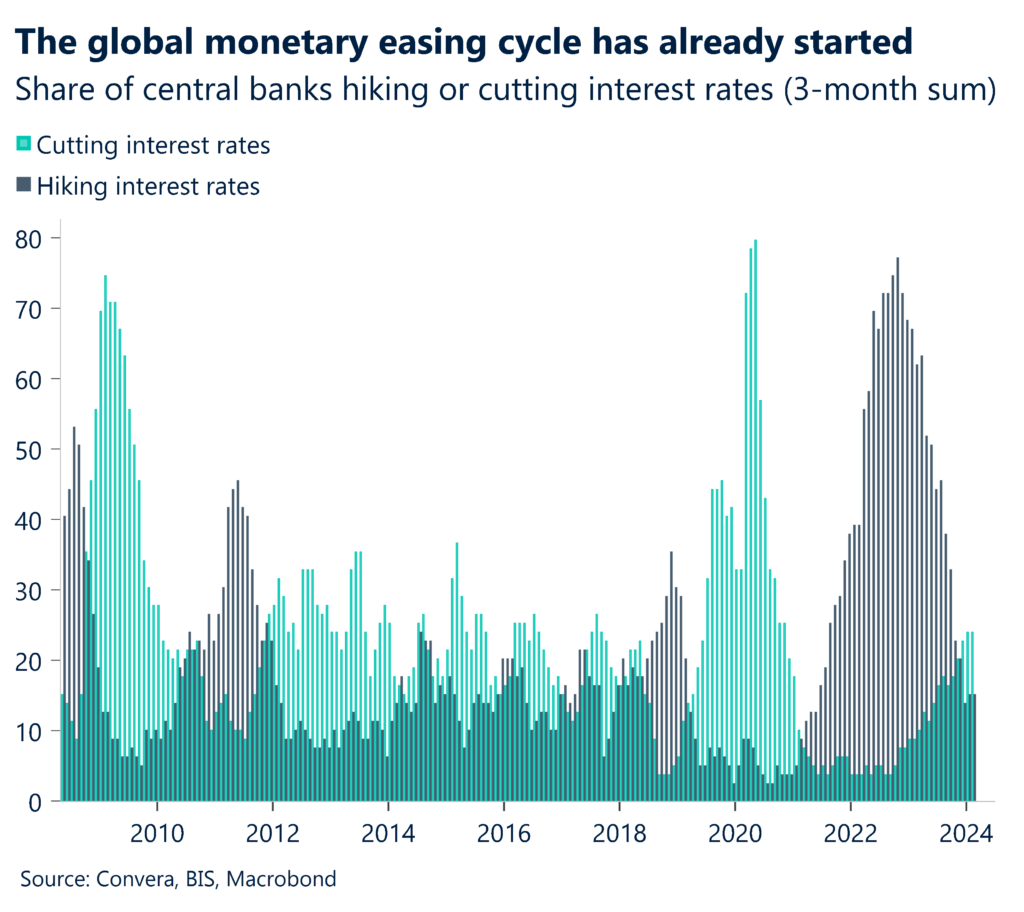

SNB first major central bank to cut

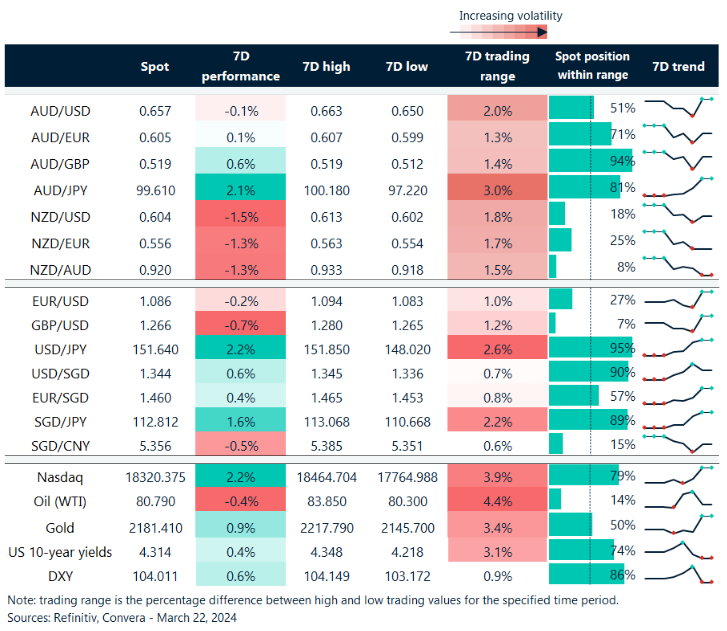

The Swiss National Bank was the first major central bank to cut interest rates overnight, causing the Swiss franc to tumble and, importantly, driving big gains in the USD/CHF pair.

The USD/CHF gains saw the greenback climb in other markets with the USD index up 0.8% as it reclaimed all of Wednesday night’s Federal Reserve-induced losses.

The SNB cut official interest rates by 25bps to 1.50% in a move that surprised forecasters that had expected the Swiss central bank to remain on hold according to an 18 March survey by Reuters.

SNB chairman Thomas Jordan said: “The easing of monetary policy has been made possible because the fight against inflation…has been effective.”

The stronger US dollar saw the EUR/USD fall 0.6% and the USD/JPY gain 0.3%.

The AUD/USD outperformed, down only 0.2%, thanks to a whopping February jobs report that saw 116k new jobs added and the unemployment rate fall from 4.1% to 3.7%.

The Aussie was higher in most other markets.

Pound tumbles after BoE

The GBP/USD saw the biggest losses overnight after the Bank of England decision kept interest rates on hold but saw two board members switch from hawkish to neutral. The BoE board voted 8-1 to hold rates. The GBP/USD fell 1.0%.

UK retail sales are due this evening. February looks likely 0.5% decline in retail sales excluding vehicle purchases.

Although there are likely complex seasonality factors to account for, which should have subsided by February, we noticed a strong jump of 3.2% month-over-month in January.

The bad weather certainly had a factor in the low retail sales. Given that February was the second wettest in a century, some customers could have stayed home. Additionally, February’s high frequency credit card data was lacking.

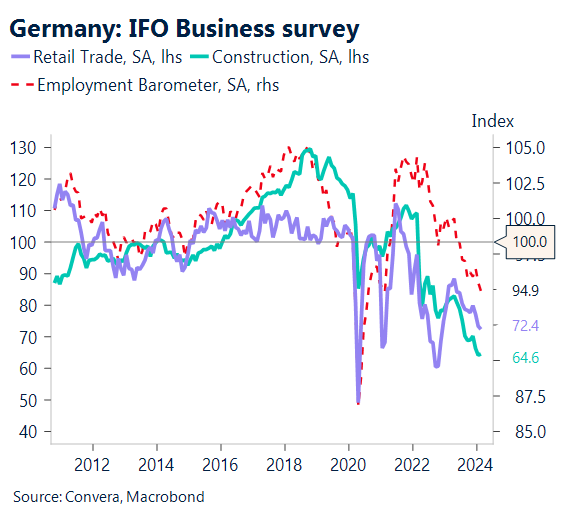

Germany Ifo survey likely weak

The German Ifo business survey for March will probably worsen, and the business environment index will likely drop by 0.6 points to 84.9.

Weakness is anticipated to originate from both components of expectations and present circumstances.

In particular, the business environment index looks likely to print 83.7 (after 84.1 previously) and the former to print 86.2 (following 86.9 previously).

The euro’s weakness overnight saw the EUR/USD fall from near the key 1.1000 level that has been a significant resistance level for all of 2024.

Kiwi underperforms post Fed

Table: seven-day rolling currency trends and trading ranges

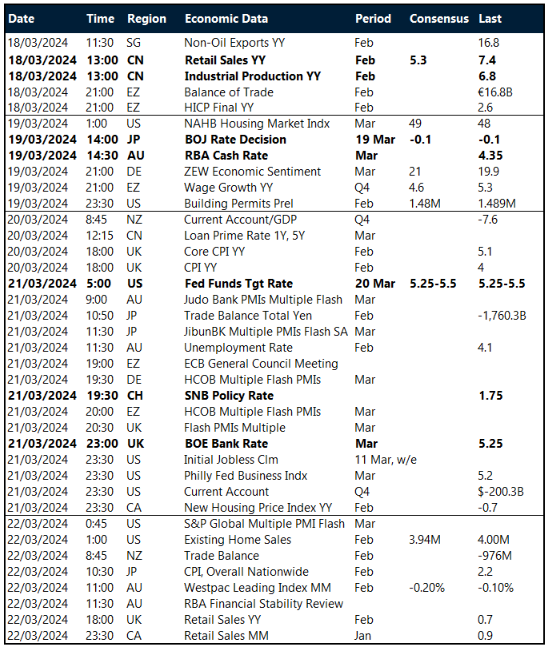

Key global risk events

Calendar: 18 – 22 March

All times AEDT

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.

Have a question? [email protected]

Take a deep dive into the trends shaping cross-border payments with our podcast, Converge.