Written by Steven Dooley, Head of Market Insights, and Shier Lee Lim, Lead FX and Macro Strategist

US shares hit new all-time highs

The US dollar extended its two-week long rebound overnight helped by strong gains in US shares.

The Dow Jones index gained 1.0% while the S&P 500 gained 0.7%. Both indexes hit new all-time highs. The tech-focused Nasdaq climbed 0.8% and is just 2.0% from the all-time highs seen earlier in the year.

The stronger US dollar saw most other key currencies weaker.

The AUD/USD fell 0.5% and is now down 2.4% over the last week. The Aussie’s been hit by growing expectations the Reserve Bank of Australia might be moving towards rate cuts.

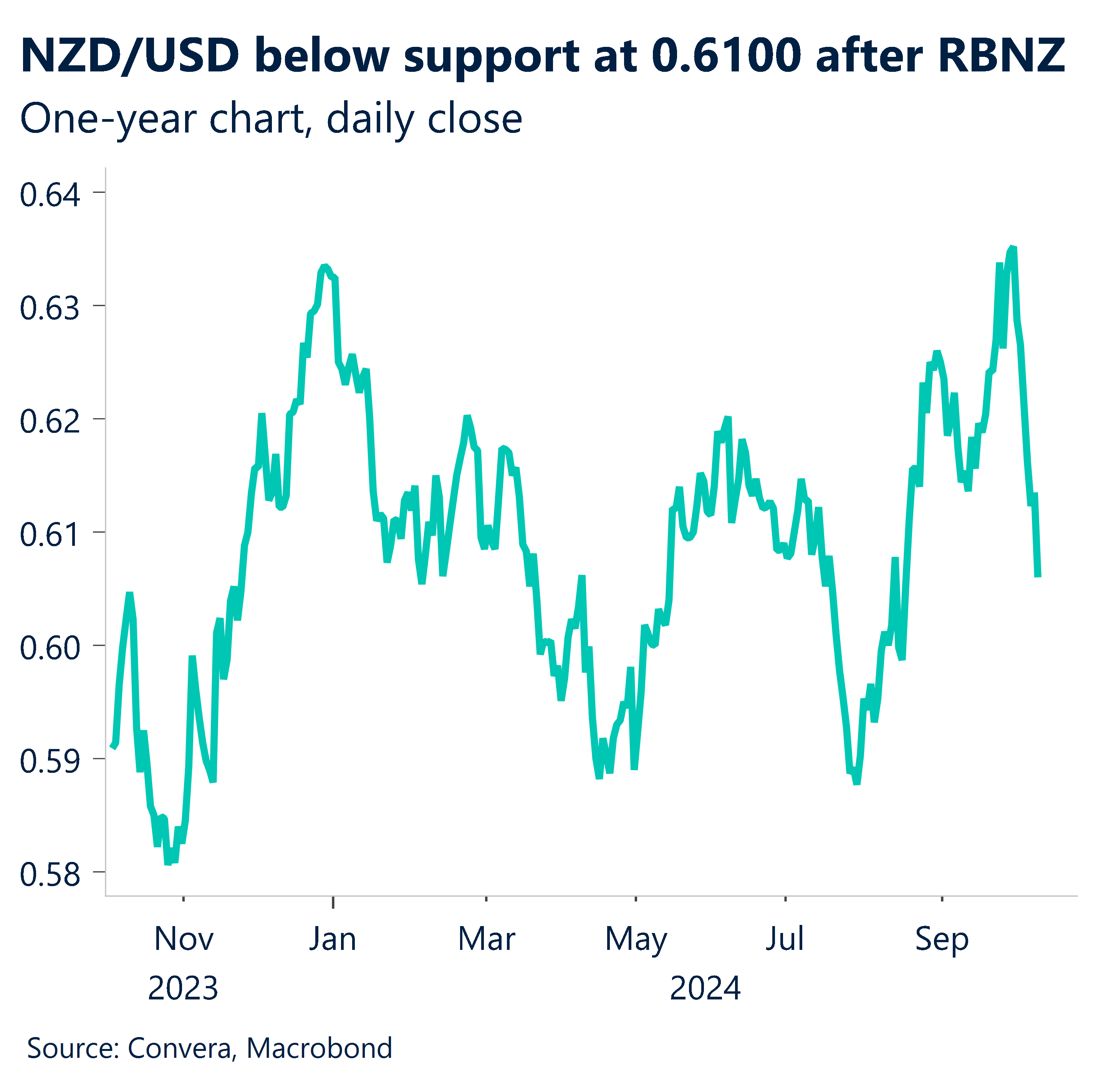

The NZD/USD fell 1.2% after yesterday’s 50-basis point rate cut from the Reserve Bank of New Zealand. The NZD/USD broke below key support at 0.6100.

In Asia, the greenback also gained, with USD/JPY up 0.6% and USD/SGD and USD/CNY both up 0.3%.

USD eyes CPI data for direction

Following an increase of 0.281% in August, core CPI inflation in September most likely stayed steady at 0.265% m-o-m.

Following two months of positive surprises, we anticipate a slowing in the inflation of core services, mostly due to a deceleration in OER.

Core goods prices provide upside risks to core inflation in the next month, notwithstanding rent disinflation. This ought to motivate the Fed to reduce its rate of easing to 25 basis points each meeting until the end of the year.

The dollar’s market movement from last week serves as a reminder that, in this cycle, UST yields—rather than growth regimes—have been the key indicator of the general direction of the USD.

In the medium run, the USD index remains in a short-term uptrend.

JPY depreciation – too fast too furious?

The USD/JPY and AUD/JPY both traded back near two-month highs overnight as the JPY fell.

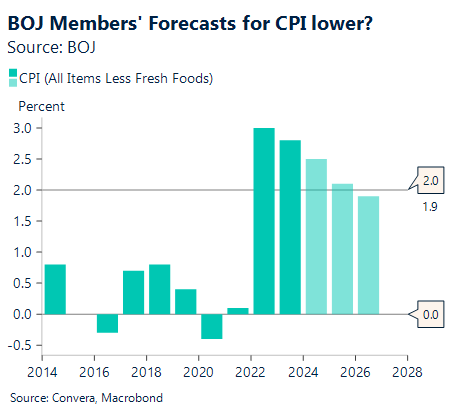

Looking forward, the BOJ’s 99th Opinion Survey on the General Public’s Views and Behavior will be released today.

Household inflation forecasts in the June 2024 poll were 10.0% y-o-y for the next year and 5.0% for the next five years.

We believe that expectations for inflation will be high for the next year as well as the next five years, given that energy prices have remained high since June 2024.

Views on the recent price increase are equally significant. The proportion of respondents who choose “Rather Favourable” in response to this question is sometimes used by families to gauge how tolerant they are of price rises.

This proportion decreased by 1.5 percentage points on a quarterly basis to 3.1% in the June 2024 poll, suggesting that families were becoming somewhat less acclimated to price increases.

It will be fascinating to see whether the September survey finds it lower.

On FX, JPY might have depreciated too fast and too furious with the USD/JPY now at key resistance at the 150.00 level. Any reversal might see a move back to 146.45 and 145.55 next.

NZD hit after RBNZ

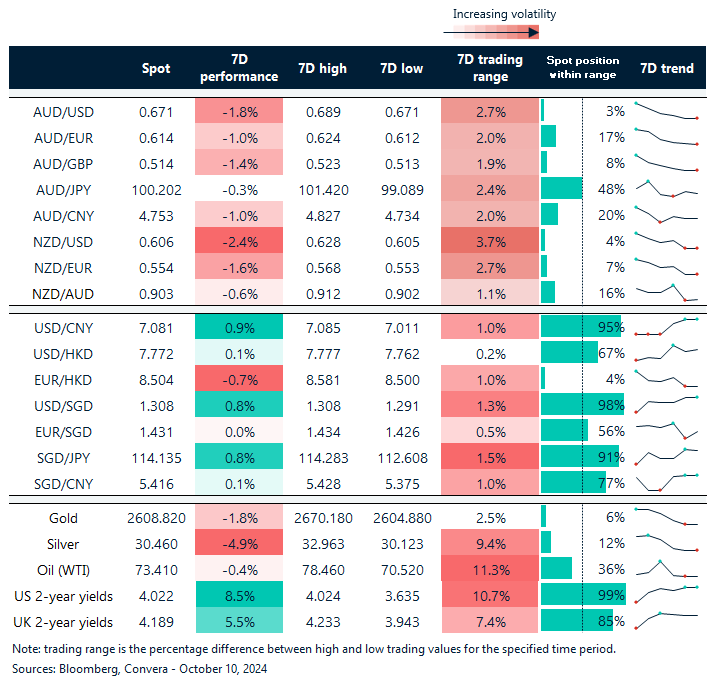

Table: seven-day rolling currency trends and trading ranges

Key global risk events

Calendar: 7 – 12 October