Written by Steven Dooley and Shier Lee Lim

Check out our latest Converge Market Update Podcast which looks at how this week’s rare mainstream media appearance from Fed chair Jerome Powell has impacted markets, why the US economy continues to outperform, and whether wages growth might be more important than inflation this year, featuring Head of Market Insights Steven Dooley.

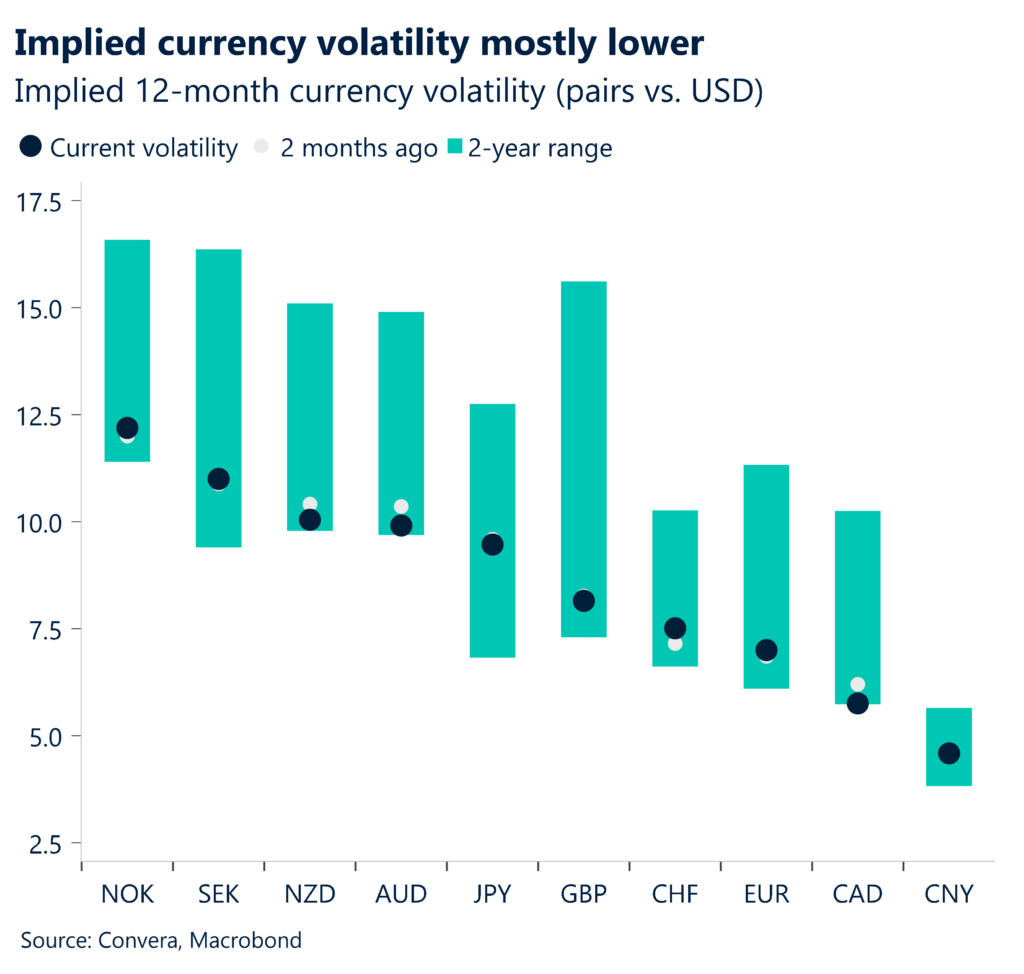

USD weaker in Europe, but mostly stronger in Asia

The US dollar eased for a second day, but remains broadly near three-month highs, as US shares continue to dominate the action in financial markets.

The Dow Jones gained 0.4% while the S&P 500 jumped 0.8% as it neared the 5000-point level for the first time ever. The Nasdaq gained 1.0%. All three indexes closed at new all-time highs with low volatility boosting sentiment across markets.

In FX, the euro and British pound were stronger versus the US dollar, while APAC currencies were mostly weaker.

The NZ dollar bucked the trend in Asia, however, with the kiwi higher after a stronger than expected employment reading.

USD/CNH nears three-month high ahead of Lunar New Year

On a stronger base, we forecast CPI inflation of -0.7% y-o-y in January, down from -0.3% in December. On a sequential basis, CPI inflation is anticipated to grow to 0.4% m-o-m in January from 0.1% in December, on increasing food costs and rising core inflation in the runup to the Chinese New Year vacation.

Because of a low base, we predict that PPI inflation will slightly increase to -2.6% yo-y in January from -2.7% in December.

PPI inflation may continue to decline sequentially in January, perhaps reaching -0.3% m-o-m, which would be higher than the -0.4% reported in January 2023 and unchanged from December.

The Chinese economy’s ongoing slowdown has seen the Chinese yuan weaken with the USD/CNH near three-month highs.

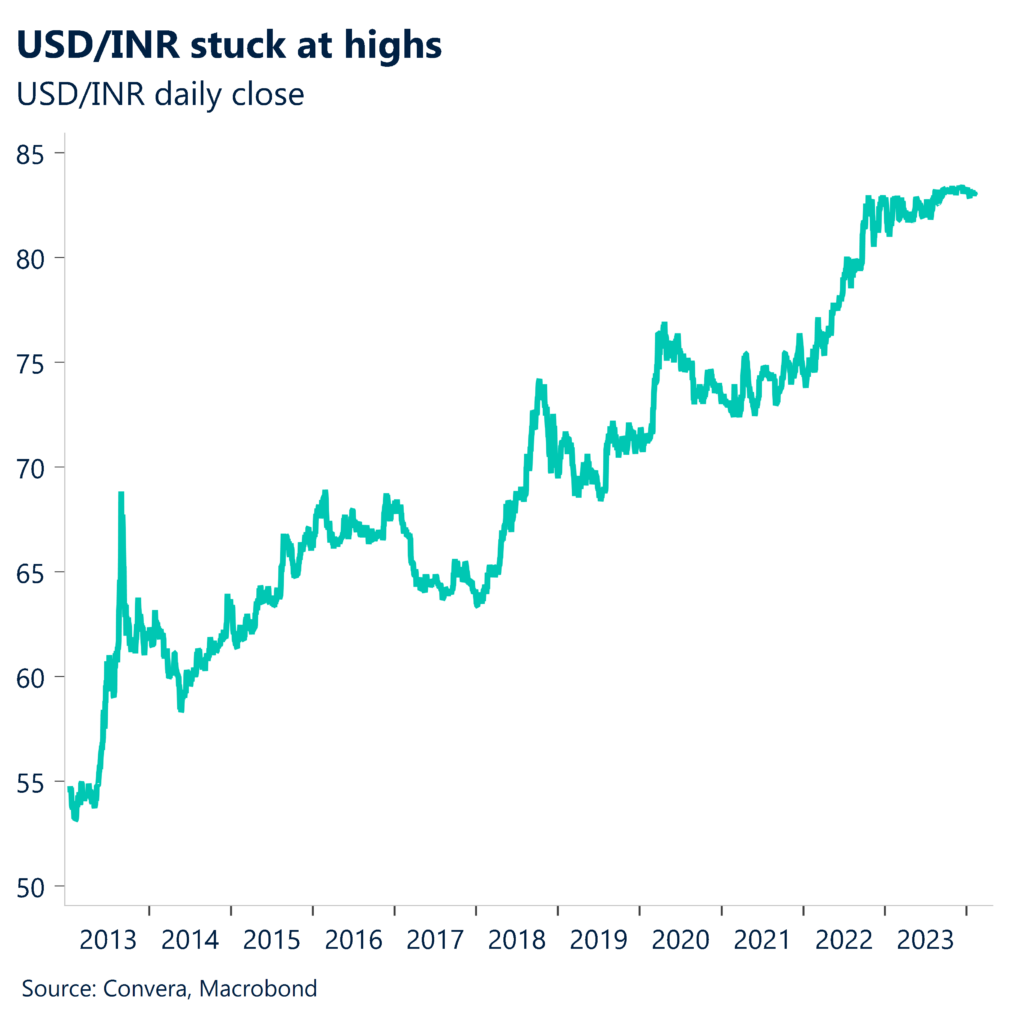

RBI decision due

At the policy meeting in February, we anticipate that the Monetary Policy Committee (MPC) of the Reserve Bank of India (RBI) would unanimously decide to take a break. Inflationary pressures have been contained since the policy meeting in December amid persistent core deflation. Consequently, we anticipate that the RBI would stick to its CPI inflation forecasts of 5.4% for FY24 (the year ending in March 2024) and 4.5% for FY25.

The economic momentum has unexpectedly increased, thus we anticipate that the RBI will increase its GDP growth predictions for Q3 (October–December) and Q4 (January–March) of FY24 from 6.5% and 6.0%, respectively, to 7.0% and 6.7%. This would lift the growth forecast for the entire year of FY24 from 7.0% to the advance estimate of 7.3%.

We also anticipate that the RBI will increase its forecast for FY25 GDP growth from 6.5% to 6.7%.

The INR’s solid macro appeal should provide support to the currency, but for now, the Indian rupee remains stuck near historic lows.

USD/CNH stronger ahead of holiday break

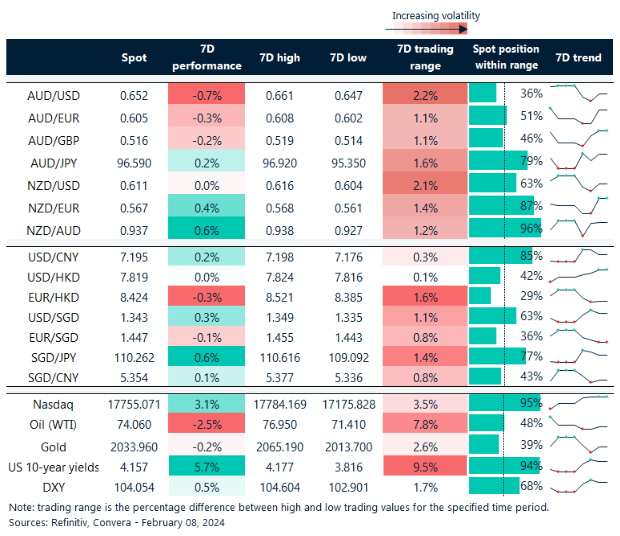

Table: seven-day rolling currency trends and trading ranges

Key global risk events

Calendar: 5 – 10 February

All times AEDT

Have a question? [email protected]

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.