Written by Steven Dooley and Shier Lee Lim

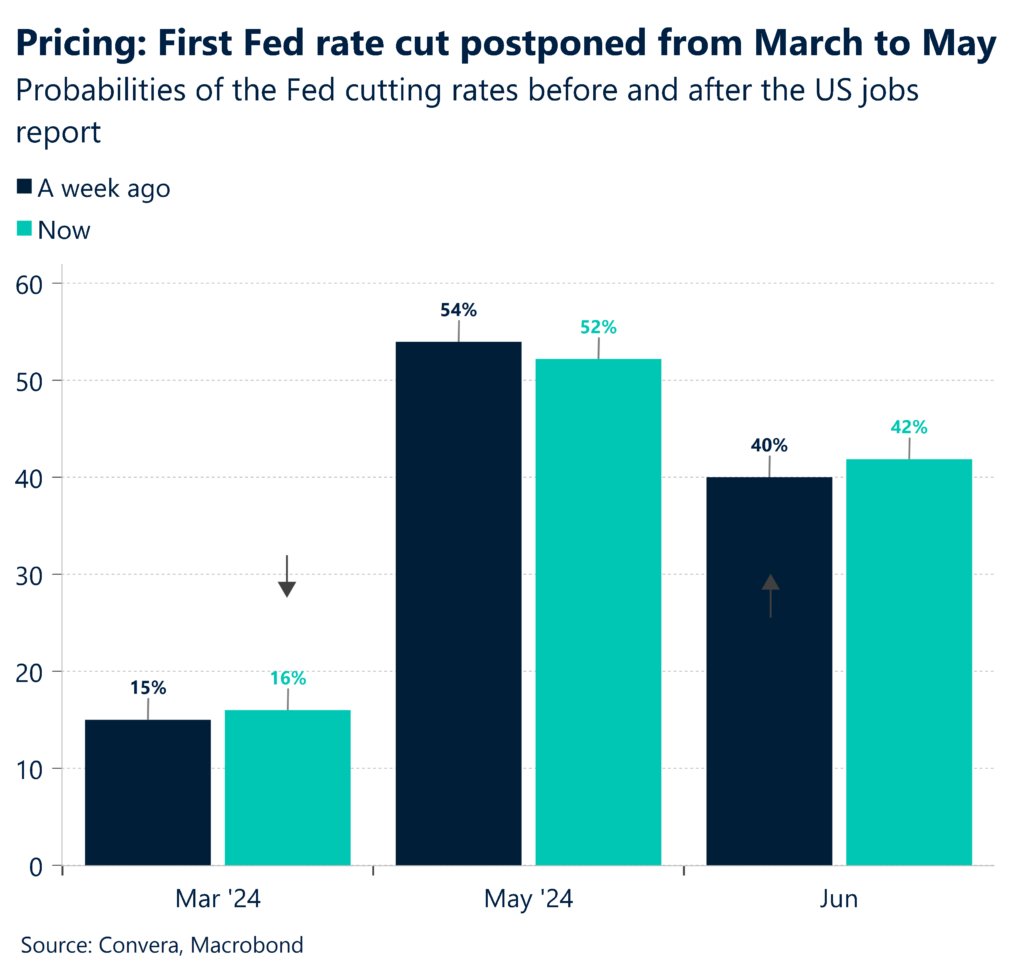

Much-feared CPI revisions turn out tame

The US dollar ended lower on Friday after a much-feared CPI revision had little impact with US inflation mostly revised lower and keeping the door open to Federal Reserve rate cuts.

Early this month, Federal Reserve chair Jerome Powell said the seasonally adjusted CPI will be a major risk that might stand in the way of rate cuts.

While the USD index fell on Friday, it ended up 0.5% for the week. The USD index hasn’t had a losing week in five weeks.

The AUD/USD reached one-week highs while the NZD/USD neared four-week highs.

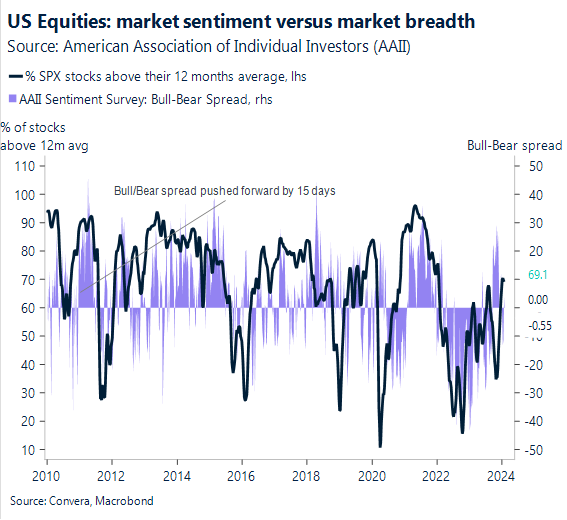

US sharemarkets at new all-time highs

After US equities reached new all-time highs on Friday, markets are looking for signs the rally can continue. Unless the Fed does cut rates rapidly, we anticipate a more difficult macro environment for equities in 2024.

The current state of the equity market is one of relative wealth, with volatility close to historical lows and increasing political and geopolitical threats. We anticipate severe reductions to unrealistic consensus growth expectations and another year of flat to low-single-digit profit growth in developed countries.

In the backdrop of sticky and lagging wage patterns, the recent disinflationary trend should constitute a significant headwind for corporate profits after a period of unprecedented pricing power. We predict reduced sequential sales growth, little margin expansion, and smaller buyback executions.

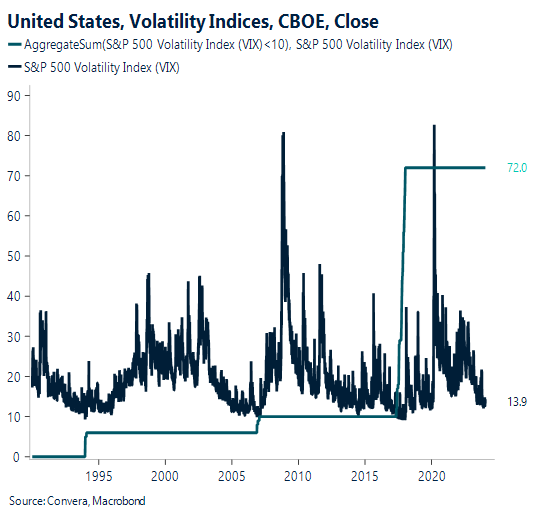

Low volatility to be watched

One of the reasons global shares have mostly been higher, is due to low volatility. (Lower volatility has been particularly beneficial to the NZD so far this year also.) This year’s extremely low volatility was caused by both technical considerations and longer-than-usual delays in the transmission of monetary policy.

Given the high rates, slowing growth, difficult stock market conditions, and elevated geopolitical risks, we anticipate the VIX to trade higher in 2024 than it did in 2023.

The magnitude of this increase will depend on the timing and severity of an eventual recession, which is still a real risk.

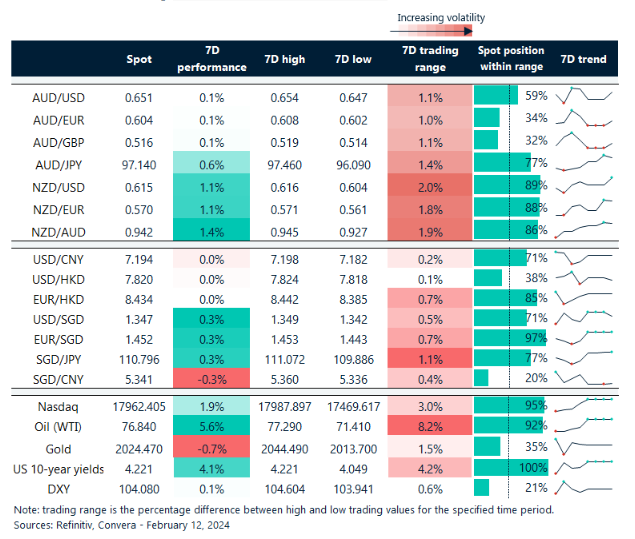

Kiwi ends week at highs

Table: seven-day rolling currency trends and trading ranges

Key global risk events

Calendar: 12 – 17 February

All times AEDT

Have a question? [email protected]

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.