Written by Steven Dooley, Head of Market Insights, and Shier Lee Lim, Lead FX and Macro Strategist

US job worries weigh on greenback

The US dollar took another step lower overnight after the weekly unemployment claims series jumped to 231k – the highest number since August last year.

The increase in the number of new persons claiming unemployment benefits was another sign of a slowdown in the US labour market after last week’s weaker-than-expected non-farm employment report.

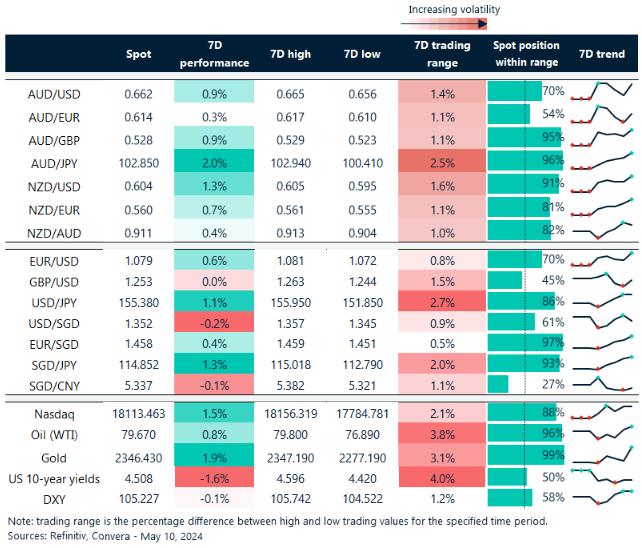

The USD index lost 0.3%.

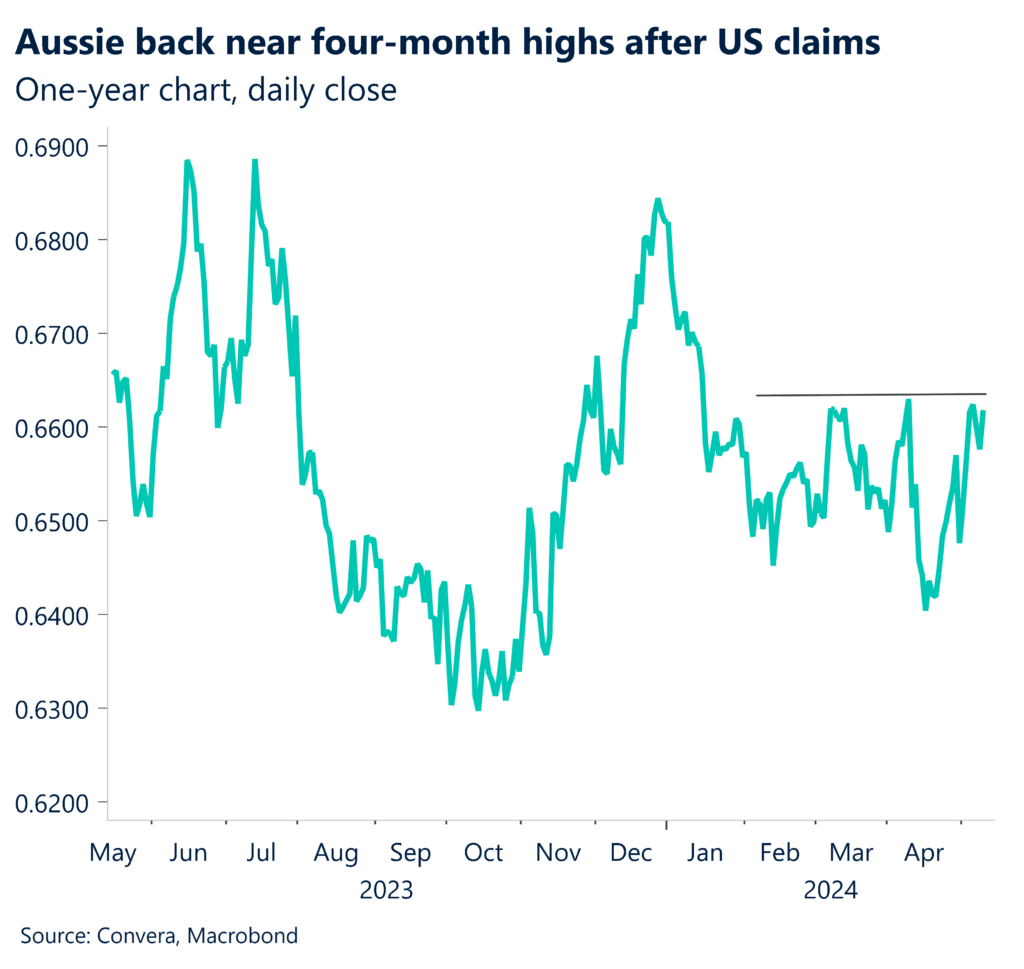

The AUD/USD climbed 0.6% as it returned to near four-week highs.

The NZD/USD climbed 0.5% to hit one-month highs.

In other markets, the focus was on the British pound, initially weaker after Bank of England decision. The BoE board saw a 7-2 split in favour of keeping rates on hold, with an additional board member now calling for cuts compared with last month.

The USD/CNH and USD/SGD were both lower.

US slowing amid economic headwinds

The disappointing US weekly unemployment claims overnight provides further evidence of a slowing in the US economy.

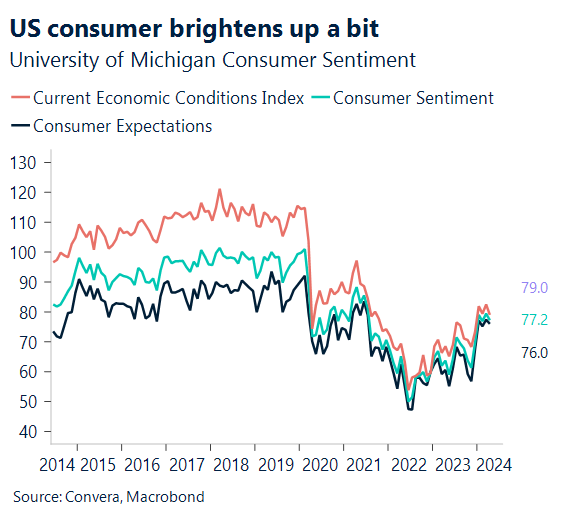

Looking forward, we have University of Michigan consumer sentiment. The preliminary reading of the University of Michigan consumer sentiment index decreased little from 77.2 in April to 76.0 in May.

During the study period, stock prices fell while gasoline prices remained flat.

Furthermore, the employment, inflation, and GDP reports for Q1 corresponded with the survey reference period. Reactions to slower economic growth, higher prices, and slower job creation are probably coming to a head.

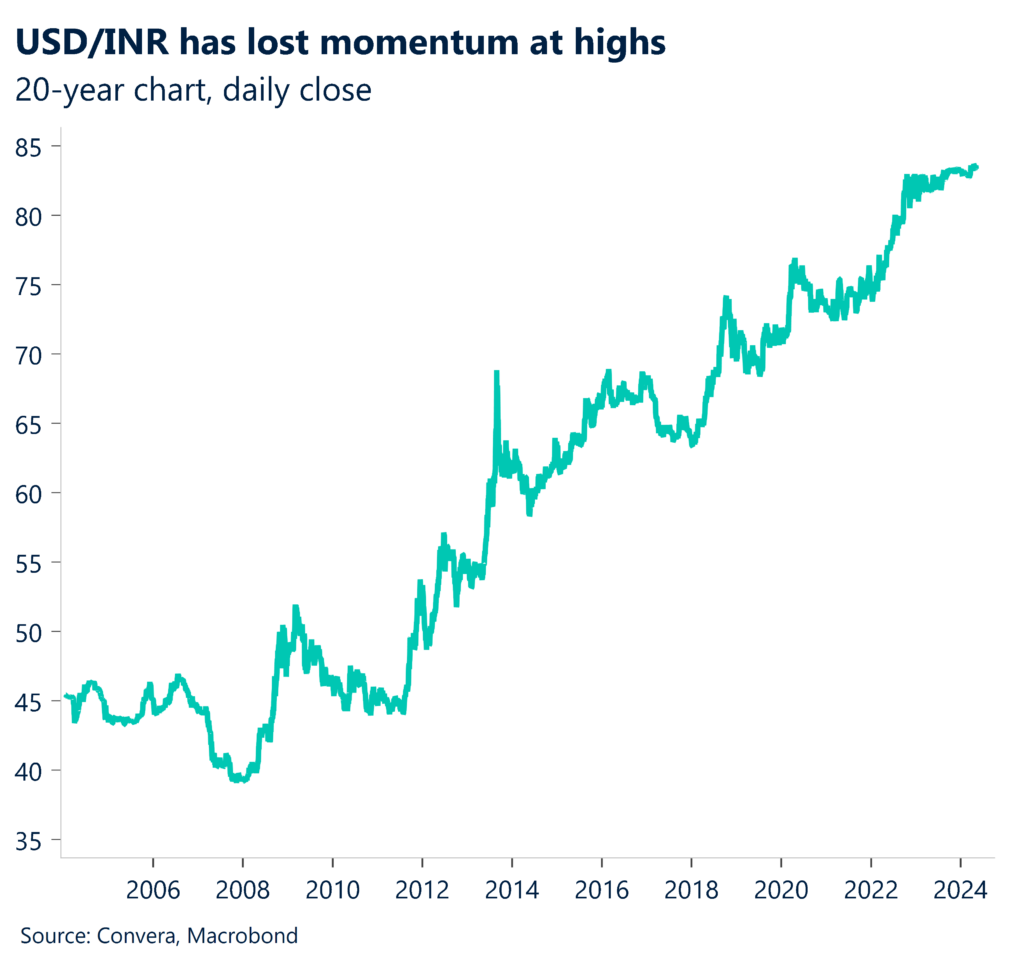

INR at lows, but resilient growth might boost

The Indian rupee has recently been trading near all-time lows versus the US dollar but any greenback weakness might see the INR gain.

Indian industrial production (IP) is due today and looks likely to fall to 5.3% y-o-y in March from 5.7% in February.

This indicates that the sequential momentum will weaken to -0.4% m-om (sa) from a robust ~1.1% average over the preceding three months.

We anticipate that capital goods and infrastructure will continue to propel the overall index, while consumer durable goods will gradually rebound. However, we are still concerned about potential weakening in the consumer non-durable sector.

The ability of the markets to withstand a difficult risk shock from rising core rates has strengthened our belief in the India macro story, potentially supporting the INR.

Aussie and kiwi back at highs

Table: seven-day rolling currency trends and trading ranges

Key global risk events

Calendar: 29 April – 3 May

All times AEST

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.

Have a question? [email protected]