Written by the Convera Market Insights team

Geopolitics driving markets

Global markets are digesting the contrasting newsflow out of Japan and the Middle East, which was holding the US dollar in a range-bound position at the weekly open.

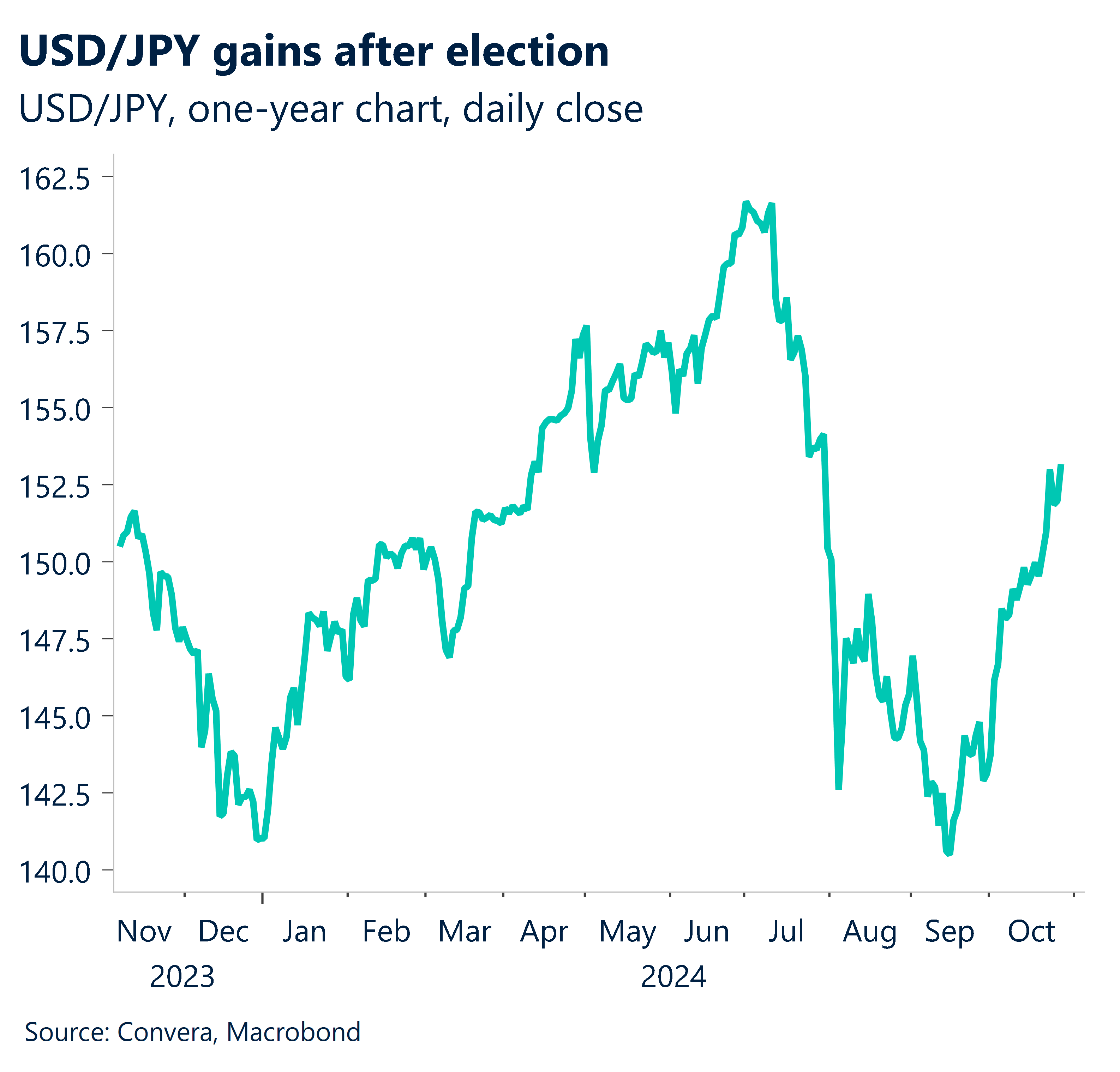

The ruling coalition in Japan lost the majority in parliament for the first time in 15 years as voters zoomed in on high inflation and political scandals. USD/JPY jumped by about 1% after losing some of the momentum in the US session. However, the currency pair is still on track for a fifth weekly advance.

Capping overall dollar gains was the easing tension in the Middle East after the previously flagged retaliation attack from Israel avoided crude and nuclear facilities in Iran.

Brent oil is now down around 13% from its earlier October peak as investors gear up for the US election, non-farm payrolls report, and next FOMC decision.

US election to buck economic history?

Markets continue to move in the direction of pricing in a higher probability of a Trump presidency.

Inflation remains the single most important issue for voters, followed by immigration, and the overall state of the economy. All three remain nuanced and complex topics, which is contributing to polls remaining within the margin of error.

Since 1929, the incumbent party has never lost an election if the US economy avoided a recession in the two previous years.

On the surface, this condition does seem to apply. However, two caveats are complicating the matter. 1) The US did technically contract for two consecutive quarters in 2022 in what has been called the phantom recession. However, the NBER did not class it as one. 2) Around 60% of voters describe the state of the US economy as bad. This perception, largely fueled by inflation, makes it less likely that the Democrats will benefit from the economy.

US “jobs week” data kicks-off

Away from geopolitics, the economic calendar sees major US labor market releases, although their impact might be overshadowed by other influences.

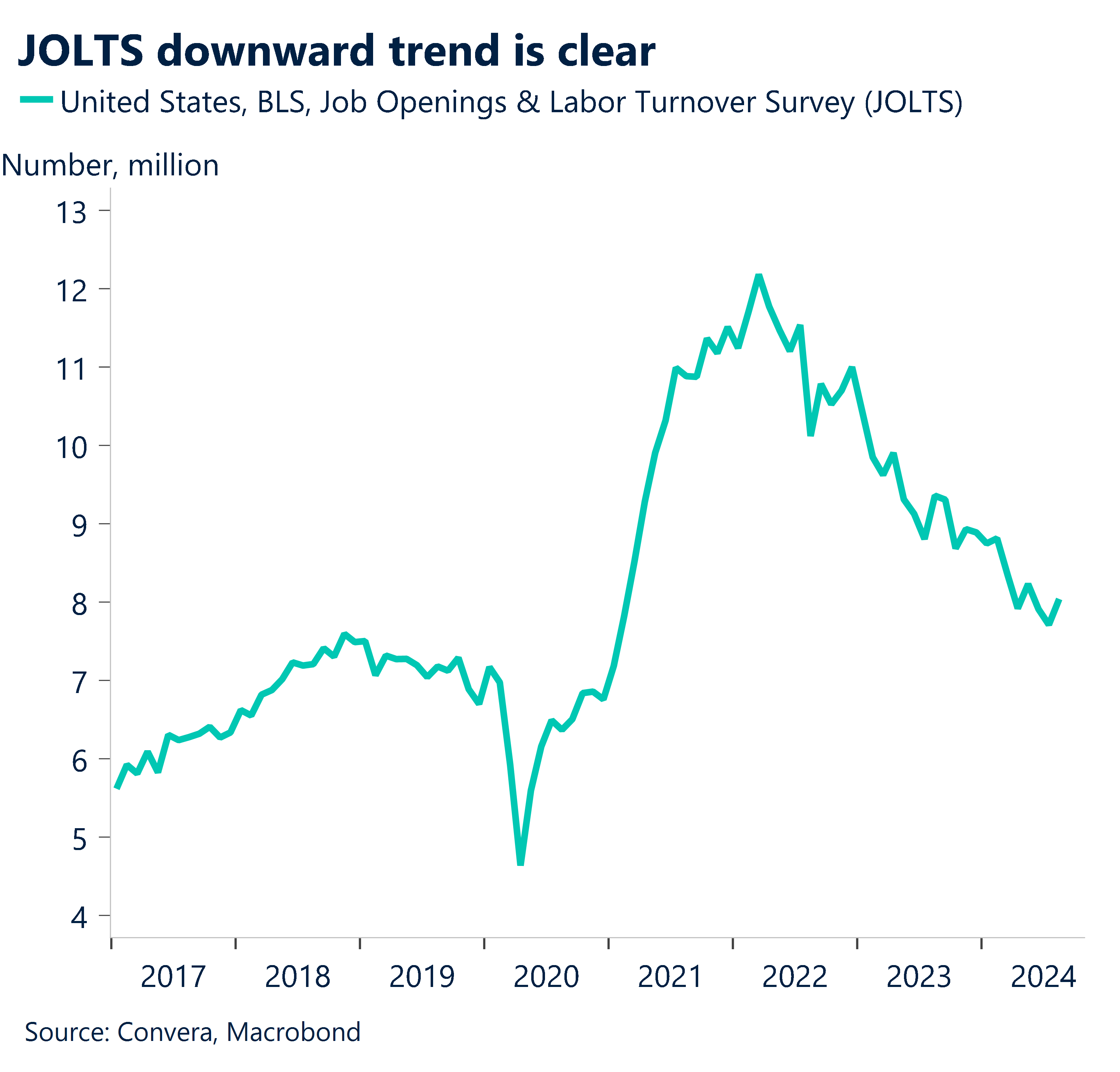

Tonight, the flurry of US jobs data commences, with the JOLTS – job openings and labor turnover series – due. The market is looking for openings to remain broadly steady at around 8.00m.

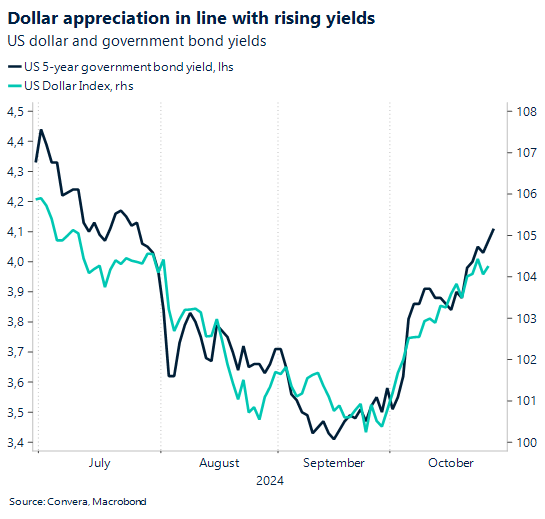

With the USD well supported in October, another strong data point could see further greenback gains.

USD remains strong

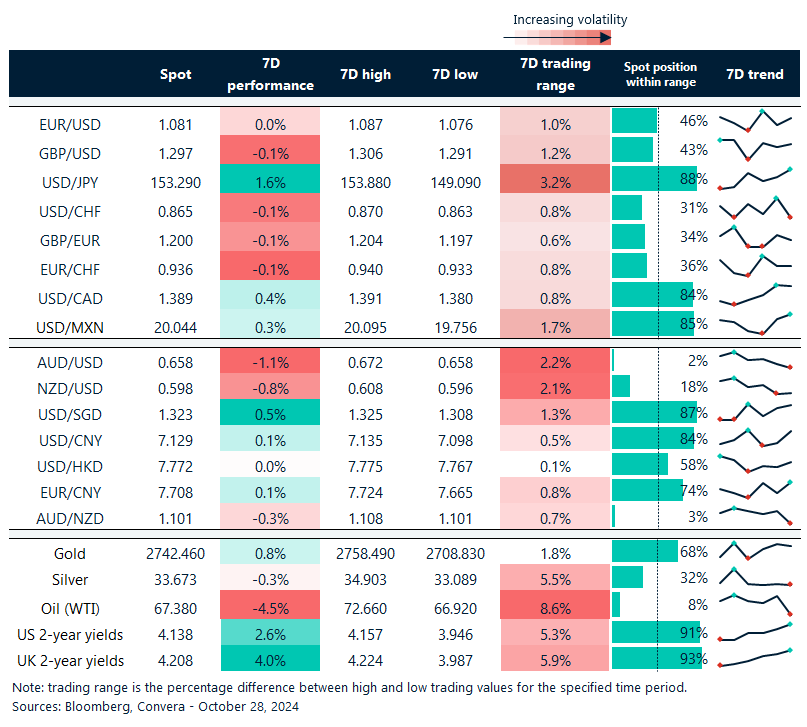

Table: seven-day rolling currency trends and trading ranges

Key global risk events

Calendar: 28 October – 1 November

All times GMT

Have a question? [email protected]

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.