Written by Steven Dooley, Head of Market Insights, and Shier Lee Lim, Lead FX and Macro Strategist

USD higher as retail sales stay hot

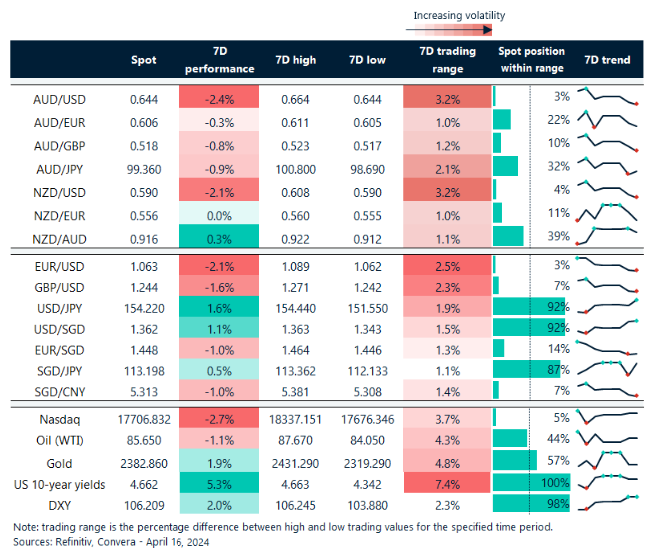

The US dollar was higher again, with the USD index reaching new six-month highs, after a red-hot retail sales number continued to cause markets to wind back expectations for Federal Reserve rate cuts.

US retail sales were up 0.7% in March, above the 0.4% forecast, with the February result upgraded to 0.9%. The US economy continues to outperform.

The probability for a June rate cut from the Federal Reserve fell to 22% according to the CME Fedwatch tool.

US shares fell with the S&P 500 down 1.2% and the greenback jumped.

The USD/JPY saw the biggest gains with the pair up 0.6% as it neared 155.00 – increasing the chance of intervention from Japanese authorities.

The AUD/USD fell 0.3% and NZD/USD lost 0.5%.

The USD/SGD and USD/CNH were broadly flat.

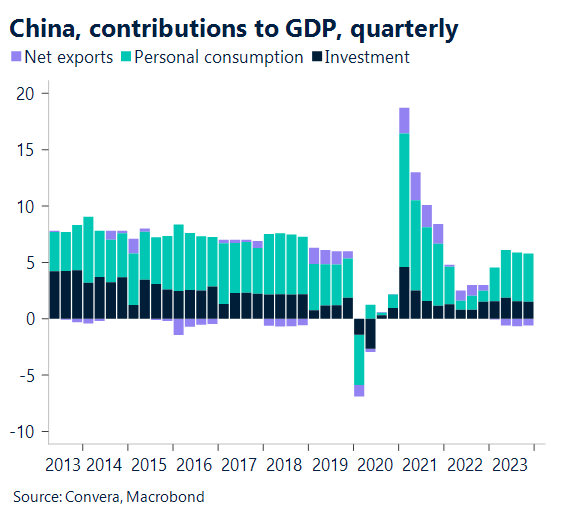

China GDP seen as likely to slow

Today’s major regional release is the all-important Chinese March-quarter GDP. Real GDP growth looks likely to slow to 5.0% y-o-y in Q1 from 5.2% in Q4.

Because of a high base and waning pent-up demand over the Lunar New Year (LNY) holiday season, retail sales growth looks likely to fall to 3.0% y-o-y from 5.5% in January-February.

We anticipate that after the LNY break, industrial production (IP) growth slowed to 4.9% y-o-y from 7.0% in January and February. This was partly because of a larger base and a later-than-usual resume of output.

We anticipate that fixed asset investment growth will also decelerate to 3.3% year-over-year from 4.2% in January and February due to a more delayed than anticipated return to production and the fact that construction activity remained mild in March.

We remain bearish on CNY with slow growth and expectations for further stimulus potentially weighing on the currency.

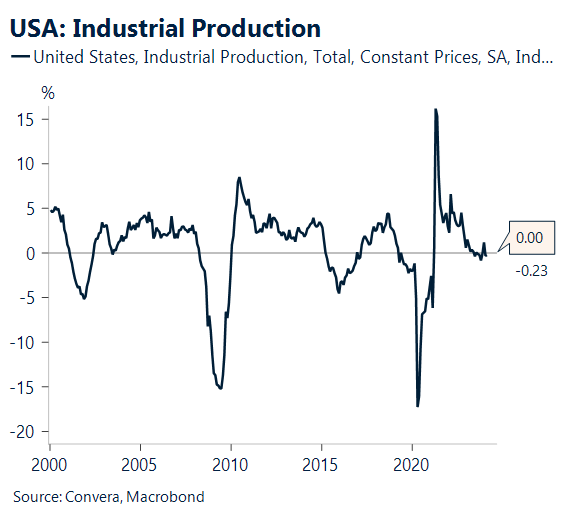

US industrial production due

The US dollar could see a further boost with US industrial production due tonight.

Following 0.1% in February, headline industrial output looks likely to increase 0.4% m-o-m in March.

Core manufacturing probably expanded by 0.3% during the month, and vehicle output also increased.

After a sharp decrease in February, we anticipate utilities to rebound. It’s probable that mining fell throughout the month, mostly due to a significant decrease in coal production.

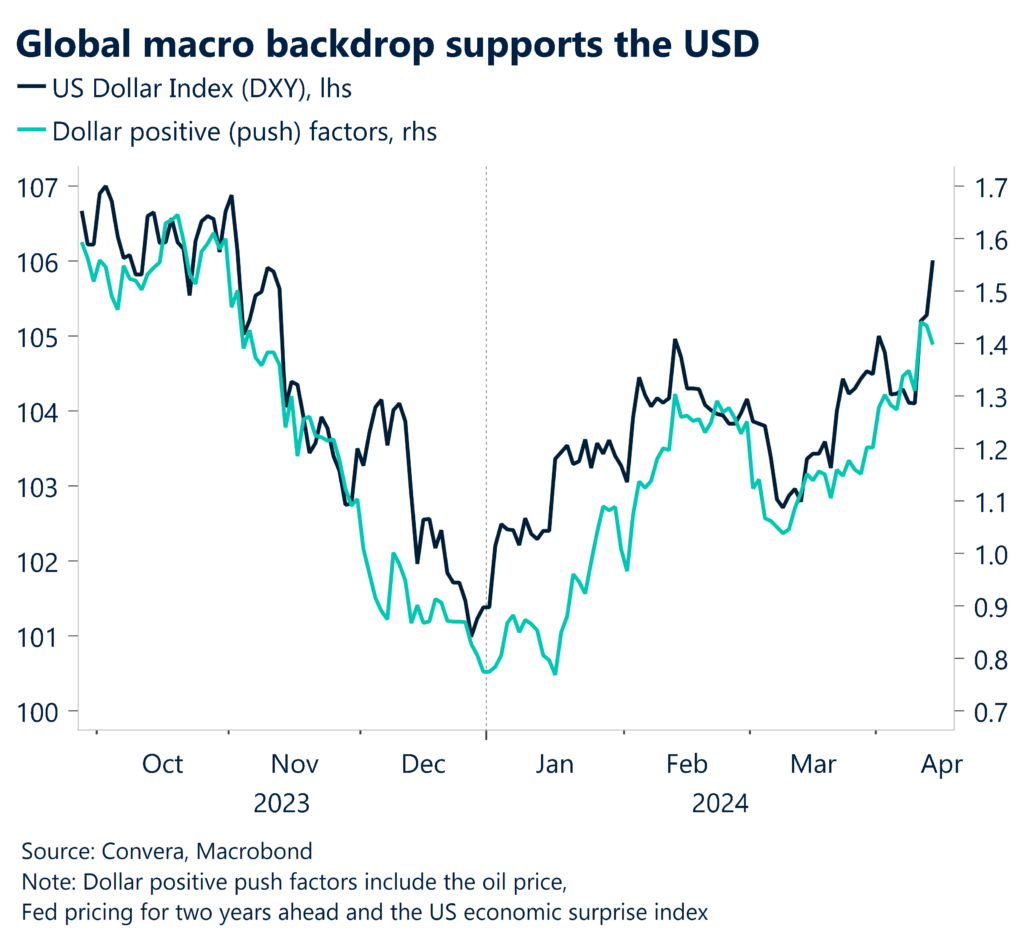

The USD has reached all-time highs due to falling expectations of Fed easing – this theme could continue to support the currency moving forward.

USD at new highs

Table: seven-day rolling currency trends and trading ranges

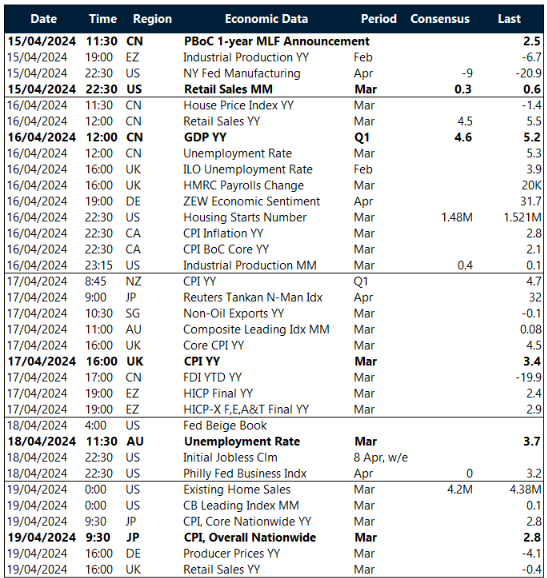

Key global risk events

Calendar: 15 – 19 April

All times AEST

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.

Have a question? [email protected]

Take a deep dive into the trends shaping cross-border payments with our podcast, Converge.