Written by Steven Dooley, Head of Market Insights, and Shier Lee Lim, Lead FX and Macro Strategist

USD boosted by hot PMI

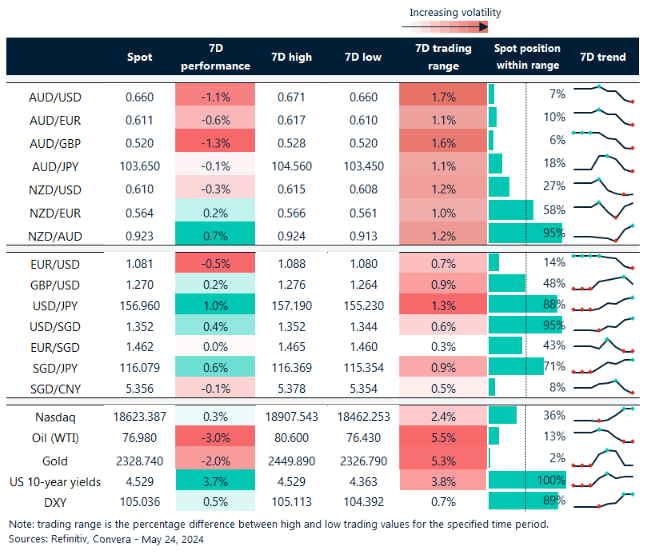

Key FX markets were mostly lower overnight – and the US dollar gained – after more strong data from the US suggested rate cuts from the US Federal Reserve are now less likely.

US purchasing manager index (PMI) numbers sharply beat expectations with the manufacturing PMI at 50.9 versus 50.0 expected while the services produced a massive result – at 54.8 versus 51.2 expected.

The PMI numbers were another example of the US economy’s outperformance – recently less impressive but still markedly stronger than peers. Money markets now have only one 25-basis point rate cut fully priced in (source: Reuters).

Falling rate cut expectations have boosted the USD this week. Overnight, the AUD/USD fell 0.2%, NZD/USD was flat, while USD/CNH gained 0.1%.

Notably, PMI numbers in other parts of the world also improved, with manufacturing better in Europe, UK and Australia, and services mostly in line or better than forecasts apart from misses from the UK and France.

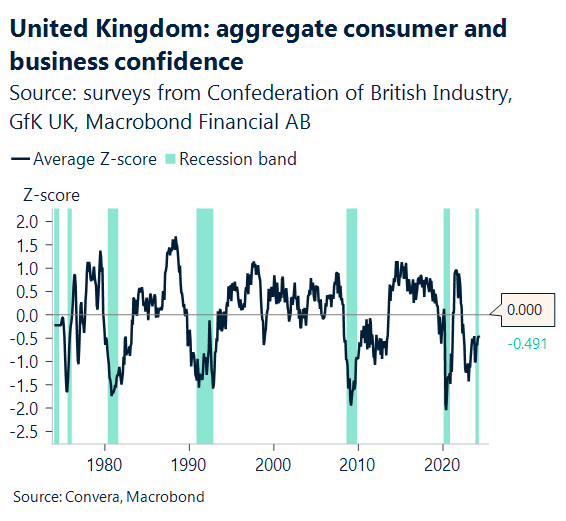

UK consumer confidence might improve…but not for long?

The GBP remains in focus with May consumer confidence likely to climb from -19 to -16.

This figure, which is not seasonally adjusted, usually shows improvement in April and May, most likely due to an improvement in the UK’s grim weather.

Also, confidence may also be bolstered by the news of a far better-than-expected GDP figure and the end of the recession. However, any boost in mood might be short lived as the UK faces six weeks of electioneering.

The wider range resistance for GBP/USD is between 1.2892-1.2915 which suggests the British pound is at greater risk of reversal.

MYR falls from four-month highs

After a surprisingly stable 1.8% in March, we anticipate headline Malaysian CPI inflation to rise to 2.0% y-o-y in April.

This is because we believe that the delayed pass-through effects of the 2-percentage point increase in the services tax at the beginning of March likely materialized more completely in key services components, such as lodging and recreation.

In addition, the tax increase is probably having some knock-on effects on other CPI basket goods at a time when labor markets are holding up and economic activity is also growing.

As BNM continues to work with government-linked enterprises to convert their export revenues, MYR has fared better than it has in the last month. However, we are cautious whether this leads to a significant shift in the conversion behavior of exporters.

The USD/MYR recently rebounded from four-month lows as the MYR’s recent strength wanes.

NZD/AUD hits two-month highs after RBNZ

Table: seven-day rolling currency trends and trading ranges

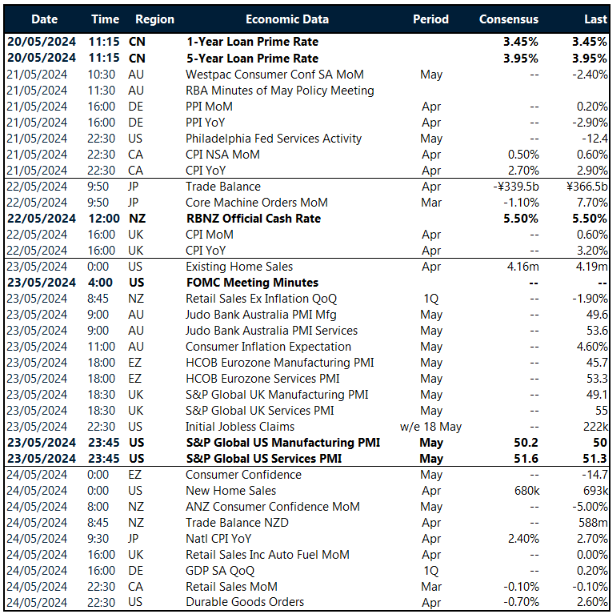

Key global risk events

Calendar: 20 – 24 May

All times AEST

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.

Have a question? [email protected]