Written by Steven Dooley and Shier Lee Lim

Check out our latest Converge Market Update Podcast as volatility across assets remains low despite the ambiguity surrounding the future policy path of central banks. What’s driving this low volatility? The synchronization of policy pricing. Join our macro analyst Boris Kovacevic as he breaks down this week’s global market news.

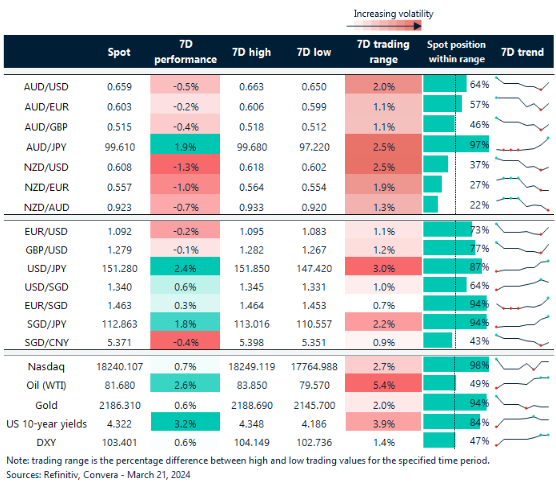

USD lower after Fed

The US dollar was lower after last night’s Federal Reserve decision saw the US central bank maintain its view that it would likely cut interest rates three times this year with chair Jerome Powell seemingly unfazed by recent hotter inflation reports.

The USD index was down 0.4% – falling from three-week highs – after the Fed announcement.

The AUD/USD outperformed, up 0.8%, while the NZD/USD gained 0.4%.

The EUR/USD and GBP/USD both gained 0.5%.

In Asia, the USD/JPY climbed 0.2% – extending recent gains after Tuesday’s Bank of Japan decision to end its negative interest rate regime.

The USD/CNH was flat while USD/SGD lost 0.2%.

Bank of England rate decision due tonight

Looking ahead to tonight’s Bank of England decision, market pricing indicates that there is virtually little chance of an interest rate change at this meeting. Any modifications to the voting pattern and guidelines will be notably more significant.

At the February meeting, Dhingra cast the first vote in favour of a rate drop, while Greene, one of the three members who had previously voted in favour of increasing rates, modified his vote to remain unchanged. Internal members have recently stated that rate reduction are “some way off” (Pill) and that inflation persistence is still “elevated” (Ramsden), implying that no other member is likely to vote with Ms. Dhingra in favour of a cut.

Over the last month, sterling has climbed against the dollar and declined against the euro. Tonight’s outlook from the BoE will be critical for the GBP.

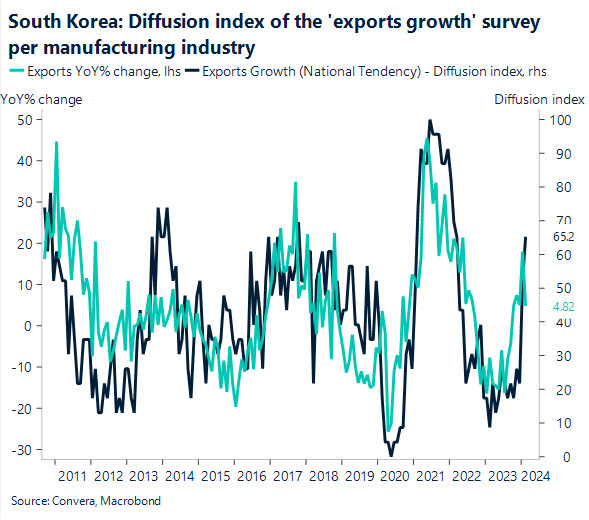

Korea trade in focus

Over the first 20 days of March, we anticipate that export growth will increase to 9% y-o-y from -7.8% in February. Though weaker auto exports have offset robust chip exports, we still predict daily average export growth to drop slightly to 9% y-o-y in March from 9.9% in February.

We believe that the weaker demand for other types of chips has restrained the growth of chip-led exports, even while the need for high-speed processors is still driving chip exports.

We remain moderately bullish on the Korean won. Why? (a) Ongoing recovery in the electronic exports; and (b) ongoing equity inflows especially since foreign ownership remains low.

Greenback lower after Fed

Table: seven-day rolling currency trends and trading ranges

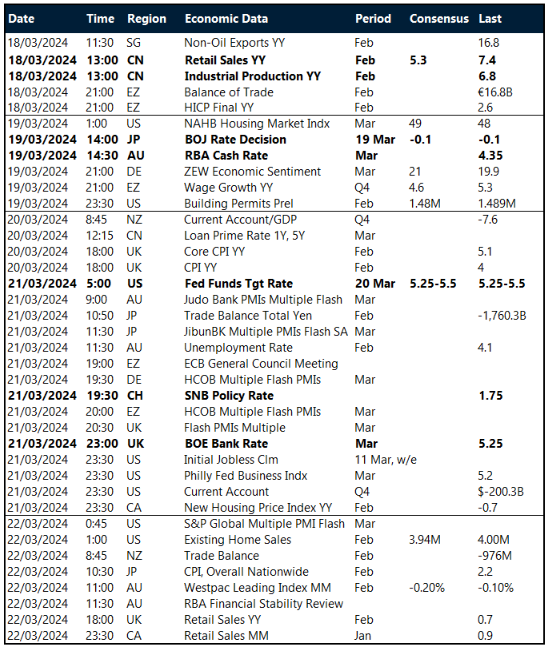

Key global risk events

Calendar: 18 – 22 March

All times AEDT

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.

Have a question? [email protected]

Take a deep dive into the trends shaping cross-border payments with our podcast, Converge.