Written by Steven Dooley, Head of Market Insights, and Shier Lee Lim, Lead FX and Macro Strategist

Aussie, kiwi ease from highs

The US dollar rebounded from more than one-year lows on Friday helped higher by the Bank of Japan’s decision to keep interest rates on hold.

Earlier last week, the US dollar had tumbled as the Federal Reserve cut interest rates by a larger-than-usual 50bps.

The Fed’s move fuelled a rally in risk-sensitive markets like global shares and FX markets like the Australian, NZ and Singapore dollars.

On Friday, however, the greenback staged a small recovery, helped by the 0.9% gain in USD/JPY after the Bank of Japan kept rates on hold. The BoJ’s recent decision to hike rates – on two occasions since March – has been one key driver of the USD’s weakness over the last three months.

In other markets, the AUD/USD stalled up at the 2024 highs while the NZD/USD also eased from levels near the year’s highs.

In Asia, the USD/SGD and USD/CNH both eased lower.

Dollar eyes manufacturing data for momentum

Looking forward, US dollar momentum might be driven by September’s S&P manufacturing PMI, due at 11.45pm AEST. This number could rebound helped by this month’s regional Fed polls, which have shown promise.

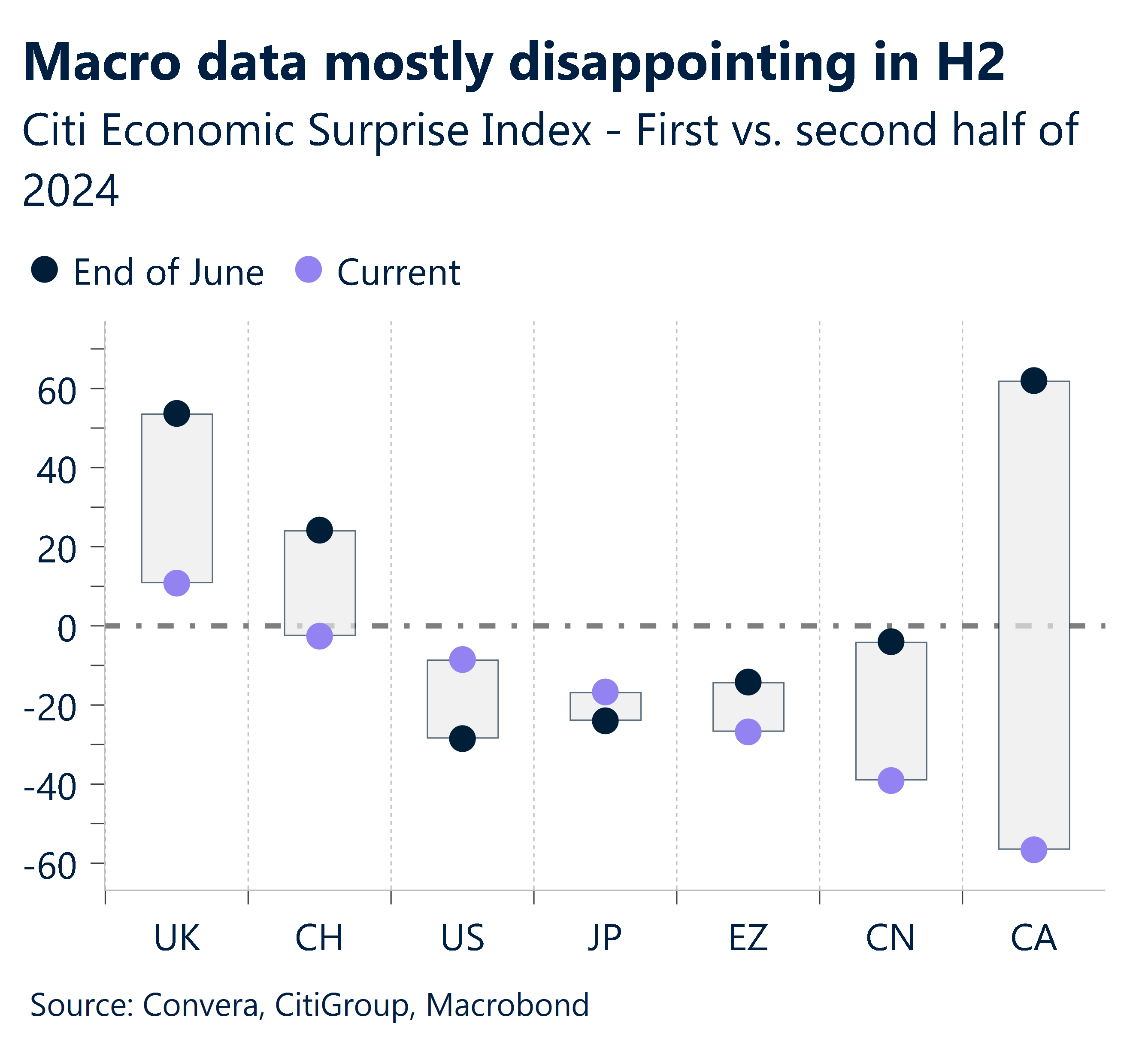

For the first time since November 2023, the Empire State Survey increased significantly (see chart, note it is ISM manufacturing PMI shown), and the Philly Fed manufacturing index also increased.

The most dollar-bearish scenario would be a soft landing everywhere, not just in the US, but this is priced-in and markets need time to process US labor market softening, so the road to USD weakness won’t be easy.

Following the Fed’s 50bps jumbo rate cut last week, the US dollar is near 14-month low but may rebound from oversold RSI condition.

Central banks and global economic pulse in focus

FX markets will be driven by central bank decisions and key economic indicators this week, with policy announcements due from the Reserve Bank of Australia, Riksbank, and Swiss National Bank.

The Reserve Bank of Australia’s decision on Tuesday (2.30PM AEST) will be closely watched, as markets assess the potential for further policy adjustments.

China’s medium term lending facility numbers are due on Wednesday.

Important economic releases include PMI data from major economies, US durable goods orders, and personal income and spending figures. These indicators will provide insights into economic growth and inflation trends, potentially influencing currency movements.

Aussie, kiwi start new week just off highs

Table: seven-day rolling currency trends and trading ranges

Key global risk events

Calendar: 23 – 28 September

All times AEST

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.

Have a question? [email protected]