The markets are feeling pretty tense this morning. The Japanese bond market is going through a historic meltdown. The 30-year yields spike 38bp in only two sessions—the second-largest jump ever, trailing only the 42bp move after “Liberation Day” last April—and since Prime Minister Sanae Takaichi took over in October, the 20- and 40-year yields have climbed roughly 80bp. This selloff is already rippling through the global macro scene, and there’s a sense that the consequences will only intensify once bonds finally find a floor. At the same time, the US Dollar is wiping out its year-to-date gains. The historically weird combination of a weakening dollar and higher yields raises the question of whether this is just a spillover from Japan or a broader “sell US” sentiment is coming back, fueled by the escalating Greenland tariff drama with Europe.

USD: King Dollar’s heavy golden crown

Richmond Fed President Tom Barkin stripped away the pleasantries last week when he noted that “Today’s economy has two engines – AI and the rich.” It is precisely this top-heavy reality that the U.S. administration is scrambling to rebalance as the headlines turn relentless and focus shifts ahead of the midterms. This shift—marked by everything from defense sector buyback changes and credit card rate caps to new restrictions on corporate home ownership—serves as the aggressive tactical front for Treasury Secretary Scott Bessent’s “3-3-3” agenda, mentioned a few days ago on an interview. By targeting 3% growth, a 3% deficit, and 3 million new barrels of oil daily, the administration is attempting to broaden the current rally into an industrial renaissance. Bessent is betting that running the economy “hot” and deregulating aggressively can spark enough organic growth to outpace the nation’s $38 trillion debt burden. It is a calculated attempt to pivot from a government-led economy to a private-sector one, but it forces the U.S. into a delicate experiment: trying to inflate the engines of growth without blowing the gaskets of fiscal stability. If the administration succeeds, that narrow “AI and the rich” rally broadens into a full-blown industrial revival, leaving the deficit hawks screeching into the void while the U.S. GDP prints numbers Europe hasn’t seen since the 90s.

However, the assumption that markets are simply swallowing this pill without side effects is naive. While the dollar remains preferred in the basket of global fiat currencies, a deeper fracture is appearing elsewhere. Gold and safe-haven metals are pushing all-time highs, signaling a profound shift in how capital perceives safety. This isn’t just about inflation hedging; it is a vote of no confidence in institutional credibility. The diplomatic feuds over Greenland and the overt threats to Federal Reserve independence—echoed in the “Shadow Fed” proposals—have investors seeking assets that cannot be debased by a tweet or a policy shift. Capital is bypassing the fiat system entirely for hard assets, creating a bifurcated reality where the dollar reigns supreme over the Euro and Yen, but loses ground to Gold.

However, there’s a key nuisance. While the headlines scream about “institutional erosion” and “debt spirals,” bond and equity markets are quietly pricing in a different reality: American Exceptionalism 2.0. When the Fed Governor’s Lisa Cook removal was announced, the bond market didn’t panic with a spike in yields as many feared; instead, long-end breakevens fell. This suggests the bond market believes it remains the “final arbiter”—a disciplinarian that will force yields up and choke off the economy if the administration gets too reckless. Investors know that no administration, regardless of its rhetoric, can afford to let mortgage rates spiral and crush the housing market. The bond market is effectively acting as the guardrail that politics cannot dismantle, providing a floor of sanity that keeps the dollar viable even as the political noise gets louder.

Yet the simultaneous flight to gold reveals that the current administration’s trust premium is thin. We are walking a tightrope where the “3-3-3 gamble” must deliver perfect execution: if the growth materializes, the debt becomes manageable and the dollar holds; if the institutional erosion continues without the economic payoff, the bond vigilantes will eventually revolt, and the safety valve of gold will become the main event. The dollar is winning the currency war but fighting a harder battle for long‑term institutional trust.

CAD: Sticky inflation, stagnant outlook

The CAD is finding some relief on a weaker US Dollar today, trading closer to 1.3820, key weekly support level. Further gains will depend on exacerbated US Dollar selling pressure and a broader global bond market sell-off.

On the macro front, the December 2025 inflation data presents a complex picture where technical “base-year effects” are masking a gradual cooling in underlying price pressures. While the headline Consumer Price Index (CPI) accelerated to 2.4% year-over-year—exceeding both the November reading of 2.2% and market expectations—this jump was primarily driven by the expiration of the temporary GST/HST holiday from December 2024. Because prices for items like restaurant food (+8.5%) and snacks (+7.9%) were artificially low a year ago, their return to normal levels created an upward push on the annual calculation. However, the Bank of Canada’s preferred core measures tell a different story: CPI-Median slowed to 2.5% and CPI-Trim to 2.7%, both down from the 2.8% levels seen in November. This suggests that once volatile food and technical tax adjustments are stripped away, inflation is continuing its slow descent toward the 2% target.

These mixed signals have solidified expectations that the Bank of Canada (BoC) will remain on an extended hold for the first half of 2026. With core inflation still sticky and above the 2% target, market pricing via Overnight Index Swaps (OIS) indicates a near-zero chance of any rate adjustments at the upcoming January or March meetings. Interestingly, the market has shifted toward a slight “tightening bias” for the later half of the year; the implied policy rate is projected to rise from the current 2.25% to approximately 2.38% by December 2026. This suggests that investors believe the BoC may need to eventually firm up rates to combat persistent cost-push factors, such as potential trade tariffs and high prices for essentials like beef (+16.8%) and coffee (+30.8%).

For the year ahead, Bloomberg analysts anticipate the Canadian dollar (CAD) will gradually strengthen against its U.S. counterpart as monetary policy paths begin to converge. Despite the USDCAD spot rate currently sitting near 1.39, median forecasts project a steady decline throughout the year, targeting 1.38 in Q1 and reaching 1.36 by the end of 2026. This expected appreciation of the Loonie is largely supported by narrowing interest rate differentials. As technical distortions in Canadian inflation data clear, the CAD is positioned to recover slightly from its current undervalued state, though it will likely remain within last year’s trading range.

Emerging Markets: Rally resumed

The global financial landscape in early 2026 is defined by a sustained period of suppressed currency volatility that has paved the way for a highly profitable regime in the foreign exchange carry trade. Following a structural shift in market dynamics during the second quarter of 2025, the inverse relationship between market turbulence and yield-seeking behavior has become more pronounced, allowing the carry index to climb steadily as investor confidence returns. This environment of relative calm has fundamentally lowered the risk premium required for cross-border investments, encouraging a broad-based migration of capital toward high-yielding assets as the fear of sudden exchange rate swings continues to dissipate.

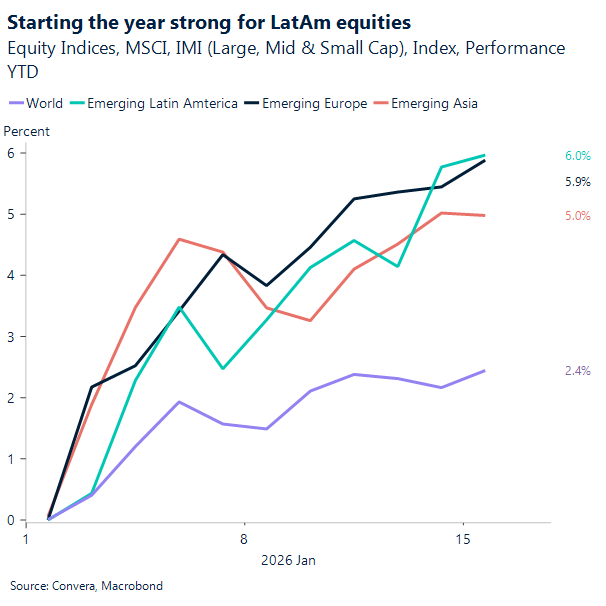

This macro-level stability has acted as a powerful tailwind for emerging market equities, which are aggressively outperforming global benchmarks in the opening weeks of the year. Capital flows are concentrating in regions that offer the most attractive combination of yield and growth potential, with Latin American and Emerging European markets leading the pack and delivering returns that significantly outpace the broader world index. The synergy between a maturing carry trade and surging local equity valuations indicates a robust “risk-on” cycle, where the convergence of currency stability and high-growth prospects is currently rewarding investors who have pivoted toward developing economies.

The Mexican Peso is staging a surprising technical breakout, slicing through key psychological support levels near the 17.60 handle to mark its most significant weekly advance since November last year. This move has effectively invalidated several bearish divergence signals from late 2025, reclaiming momentum with enough conviction to suggest the 50-day moving average, a level it has respected for months, is no longer a ceiling but a launchpad. With USD/MXN now trading at its lowest levels since July 2024, the path of least resistance appears skewed toward further appreciation. However, sustaining double-digit returns remains a high bar for Latin American currencies as they contend with the gravity of a firming Greenback. Should 2026 see even a modest recovery in the US Dollar Index, the Mexican Peso’s yield advantage will likely struggle to drive further spot appreciation.

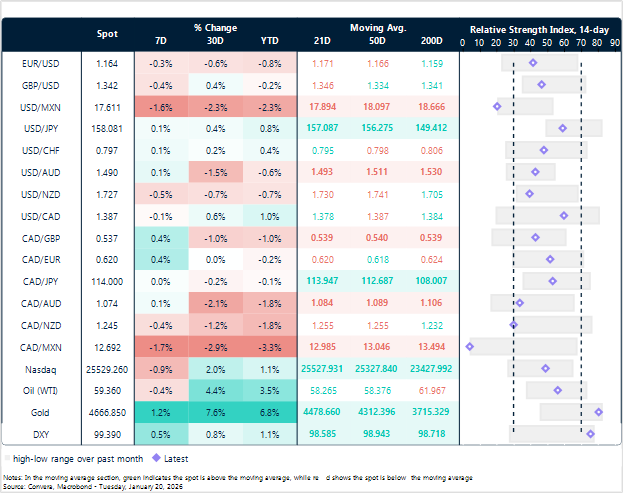

Market snapshot

Table: Currency trends, trading ranges & technical indicators

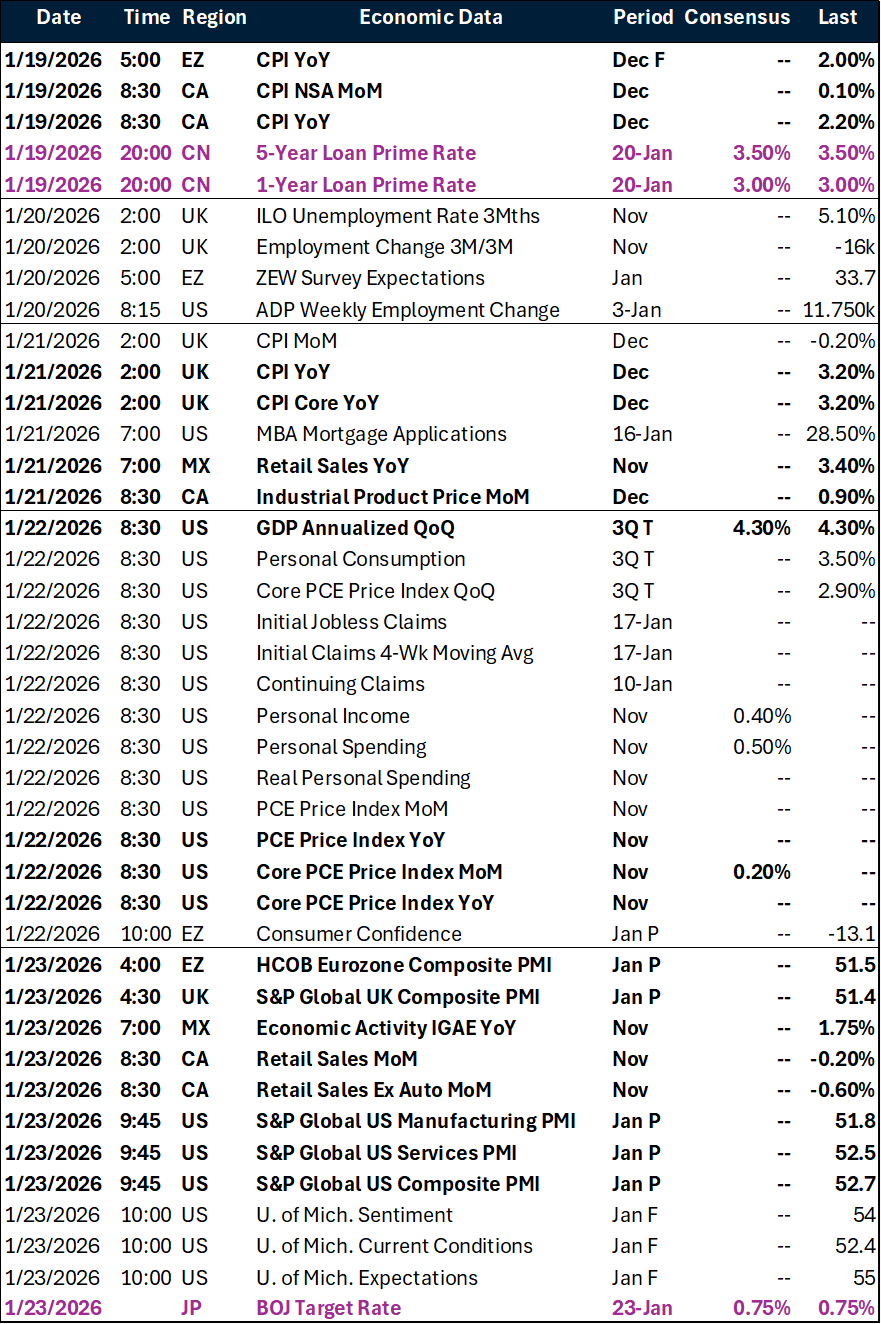

Key global risk events

Calendar: January 19-23

All times are in EST

Have a question? [email protected]

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.