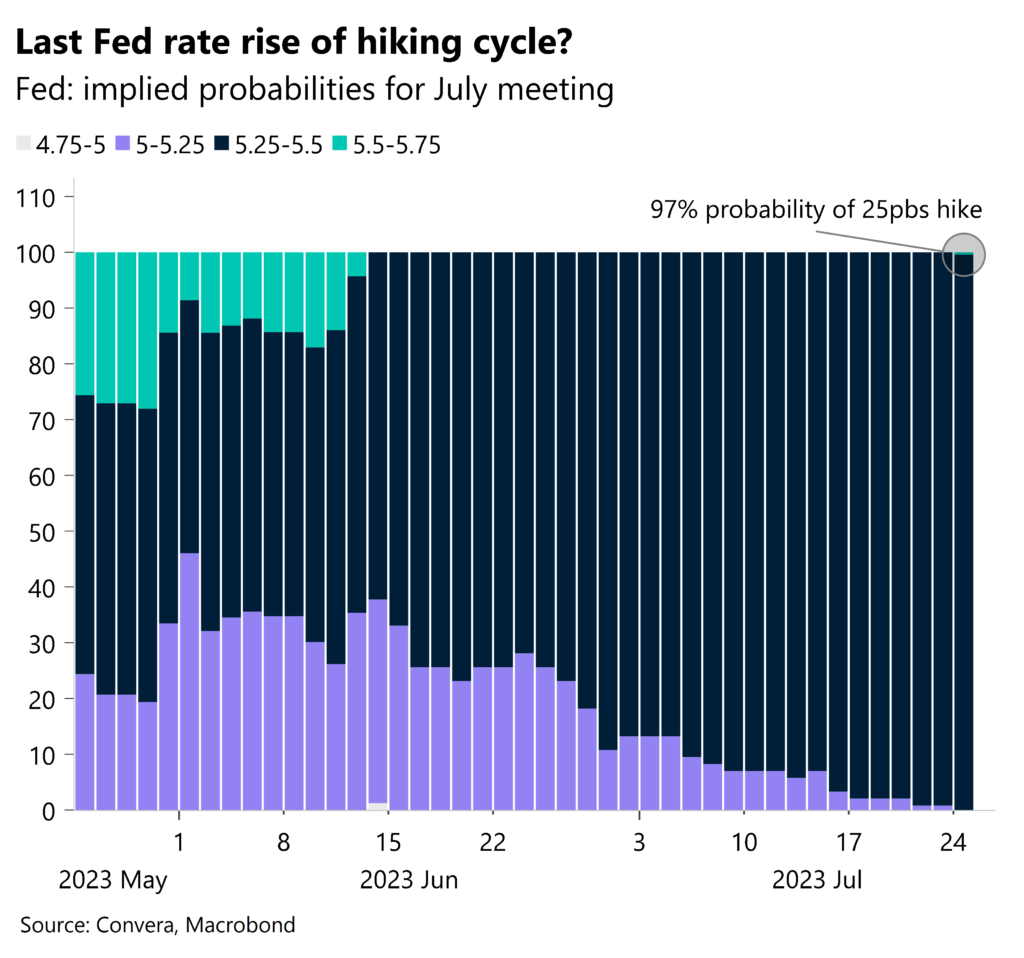

Fed hike priced in, communication is key

In line with market expectations, we expect the US Federal Reserve (Fed) to hike interest rates by 25 basis points this evening, bringing its benchmark rate to a range of 5.25% to 5.5%. The more important question though is what the US central bank has to say about the future. Will it allude this is the last hike of the tightening cycle (USD negative) or will it signal a bias towards an additional hike and push further back against 2024 rate cut bets (USD positive)?

Although we are seeing many recession-warning flags in several leading indicators, especially the breadth and depth of yield curve inversions, there are still signs of a resilient US economy. The manufacturing sector has been in contraction for some time, but the services sector continues to prop up the economy, the labour market remains tight and even consumer confidence hit a 2-year high, helping to keep the pressure on the Fed to maintain its hawkish tilt. Moreover, Fed officials will be wary of just how “risk on” the climate has been in financial markets of late, with numerous equity indices stretching towards all-time highs amid easing financial market conditions. With all this in mind, it’s hard to see the market pricing less Fed tightening than at present and the US central bank is unlikely to sound too downbeat given the latest data. Hence, we see the risks for US rate expectations and the USD as being to the upside, potentially dragging EUR/USD under $1.10 and GBP/USD below $1.28.

A 25-basis point hike is 97% priced in, and that’s what the Fed is likely to deliver. So, any market volatility will likely come during the post-meeting presser with Fed Chair Jerome Powell, therefore we cannot rule out any surprisingly dovish comments potentially hurting the USD, espeically given the cooling inflationary pressures in the US.

Pound supported by upbeat data

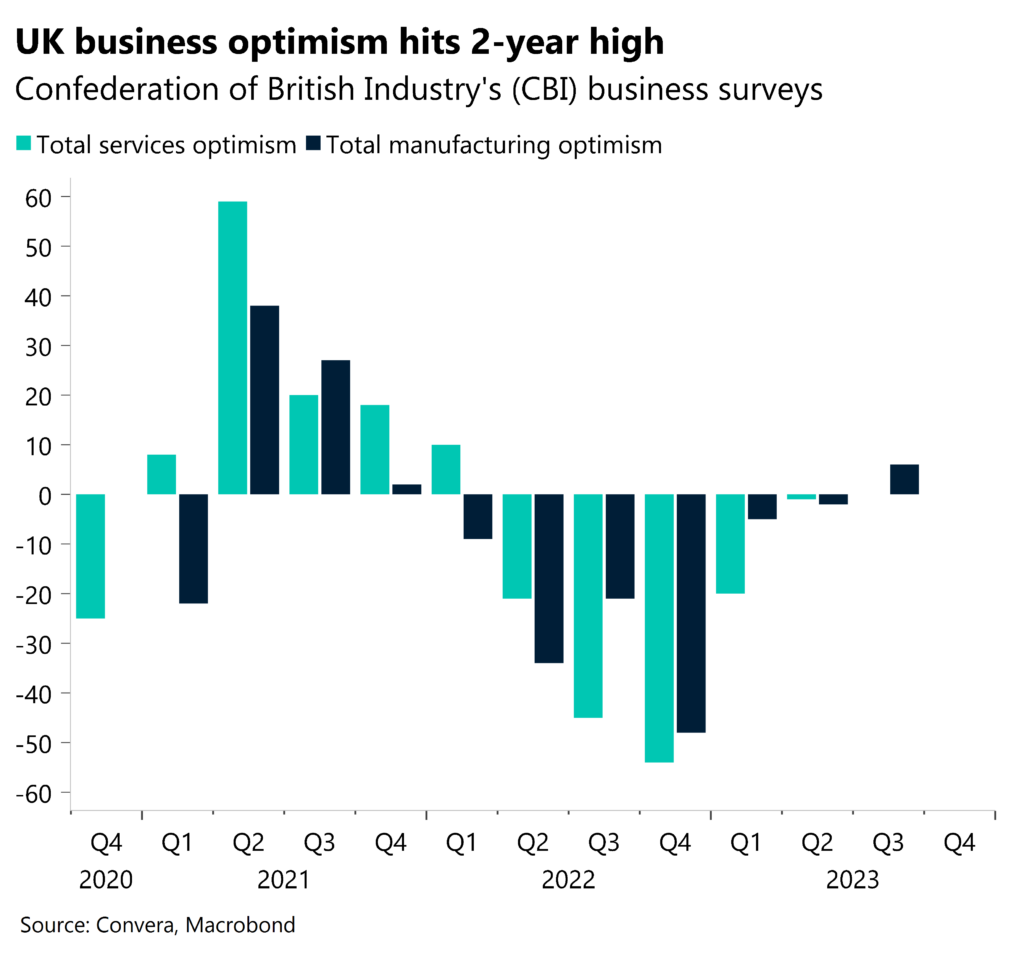

The International Monetary Fund (IMF) raised its outlook for the world economy this year and considers that the UK would now avoid recession, boosted by strong consumer spending, falling energy prices and a resilient financial sector. Meanwhile, Confederation of British Industry (CBI) surveys painted a slightly rosier picture of the UK economy compared to the disappointing flash PMIs on Monday.

The CBI surveys revealed the quarterly gauge of manufacturing optimism in the UK hit its strongest level since the third quarter of 2021 and suggested that most respondents were more confident about the future. Meanwhile, the total order book balance rose to the highest level in seven months and above its long-run average. The pound remains pressured by downsized UK interest rate expectations though. Sterling enjoyed an acceleration in strength against many peers at the start of the month amidst markets pricing in a terminal Bank of England (BoE) rate of 6.5%. However, now markets think that the BoE rate will peak at about 5.8% after a wave of weaker macro data and a cooler-than-expected UK inflation report adding to the disinflation story gaining traction globally.

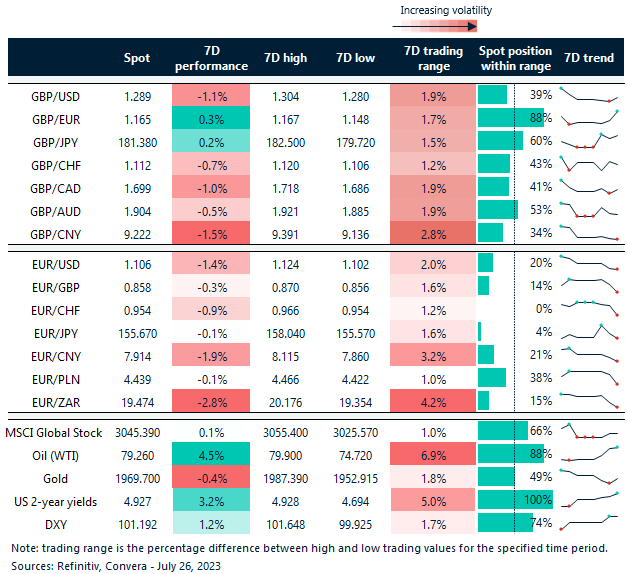

GBP/USD has fallen in line with the UK-US two-year yield differential, toying with the $1.28 handle yesterday but rebounding to $1.29 on profit taking on GBP-shorts ahead of the Fed’s decision later today. GBP/EUR is around 1% off its 10-month high and has erased all of last week’s losses due to the dismal data out of Europe.

Euro struggling to ignore recession risks

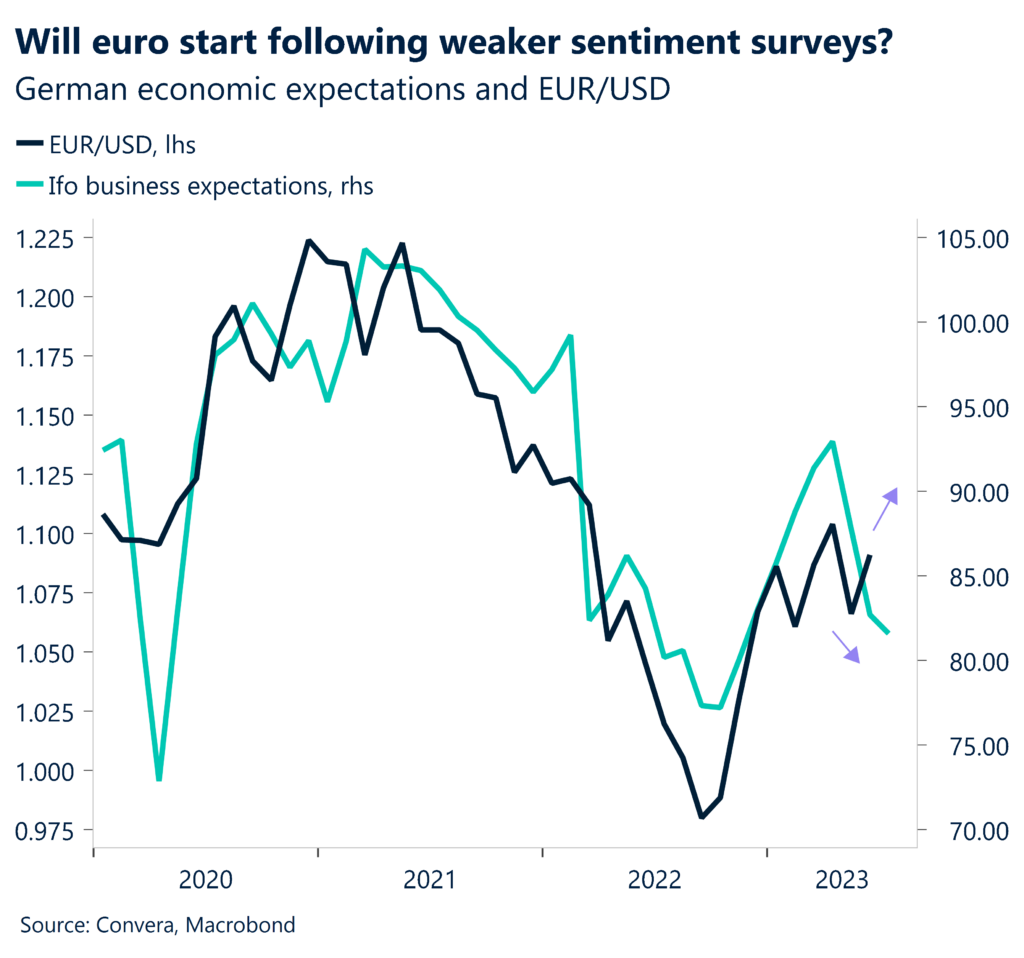

The euro has held up surprisingly well this year given the bleak European economic backdrop and outlook. The hawkish European Central Bank (ECB) helps to explain some of the euro’s resilience, but it’s largely a result of upbeat investor sentiment since the hawkish policy divergence (ECB vs. Fed) has narrowed recently.

Although all eyes are on the Fed and ECB meetings this week, market participants will surely find it hard to ignore the feeble European fundamentals, hence it wouldn’t be surprising to see a continuation of euro weakness to sub-$1.10 against the USD, especially if risk sentiment wavers. After a grim PMI reading on Monday, Tuesday saw the Ifo Business Climate indicator for Germany fell for a third month running. Firms’ assessments of their current situation turned notably more pessimistic, while expectations for the upcoming months also turned more negative. The latest readings of leading indicators suggest that the dire economic situation in Europe’s biggest economy could get worse before it gets better. Indeed, according to the IMF, Germany’s economy will suffer the only the contraction in the Group of Seven this year.

Given the disinflationary forces going into the second half of the year, and recession worries inflating, rate hikes by the ECB beyond September seem unlikely. We await communication from the ECB on Thursday after its expected 25-basis point hike. Although positive rates are a game changer for the euro, upside beyond $1.15 this year will likely be limited given the growth outlook, and the latest insight from the ECB Bank Lending Survey suggesting an on-going and substantial cumulative tightening in credit standards and weak credit demand.

Dollar firms near 2-week high

Table: 7-day currency trends and trading ranges

Key global risk events

Calendar: July 24-28

Have a question? [email protected]

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.