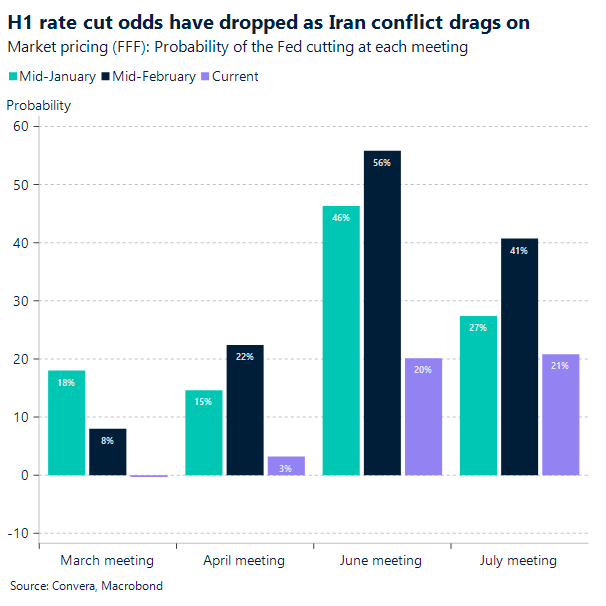

Fed navigates Hormuz oil shock

The Fed’s template for oil shocks is clear: guard inflation expectations while avoiding overreacting to volatile energy prices. In practice, that means watching whether higher gasoline and diesel feed through to core inflation and wages, not just headline CPI. Powell underscored this approach in 2022, focusing guidance on core PCE and expectations rather than one‑off energy spikes. The strategy sits inside the Fed’s 2020 framework shift to average inflation targeting, which tolerates temporary overshoots if expectations stay anchored.

History backs the playbook. In 2008, when crude first surged and then collapsed during the financial crisis, the Fed cut rates to the effective lower bound and deployed balance‑sheet tools as growth and stability risks dominated. In 2020, when WTI futures briefly printed negative on storage stress, policy again prioritized market functioning and the real economy. When Russia invaded Ukraine in 2022 and oil jumped, liftoff still began in March with a 25 bp hike, and communication acknowledged energy as an inflation risk while keeping the focus on broader persistence.

Today’s context adds a tougher oil shock. The US–Iran war and the effective chokepoint at the Strait of Hormuz have pushed Brent above $100 and introduced what the IEA calls the largest supply disruption on record. Today’s FOMC meeting brings an updated SEP, so any shift in core and growth projections will signal how much of this shock they see as persistent.

Baseline expectations point to a hold with tougher language. The Committee will likely reiterate that energy‑driven headline bumps warrant vigilance, but decisions hinge on breadth and pass‑through to core, wages, and expectations. If the disruption eases, the Fed can stick to a glide path that keeps policy restrictive enough to secure 2% over time. If the choke persists and inflation expectations drift, the bar for renewed tightening falls, but the Fed will want corroborating evidence in the core data and the labor market before moving. Either way, communication remains the tool of first resort: acknowledge the shock, highlight the reaction function, and keep expectations anchored.

Against this backdrop, while markets push out 2026 rate‑cut hopes, dollar’s resilience should keep coming from a safe‑haven and terms‑of‑trade bid, meaning that the bar for a decisive USD downtrend is de‑escalation and visible normalization of physical oil flows. The Fed’s communication today can reinforce that staging by acknowledging the oil shock, insisting on data‑validated persistence before changing the policy rate, and letting the dots reflect a slower disinflation if pass‑through broadens, all of which would keep the policy narrative aligned with the view of a gradual DXY mean‑reversion on de‑escalation, not a snapback.

While a further leg up for the Greenback hinges on a flare-up in energy prices and market volatility, in the very short run, that leaves the USD biased firm into the meeting on repriced Fed‑cut odds, with dips likely limited until shipping, storage, and insurance conditions around Hormuz improve and the conflict premium bleeds out.

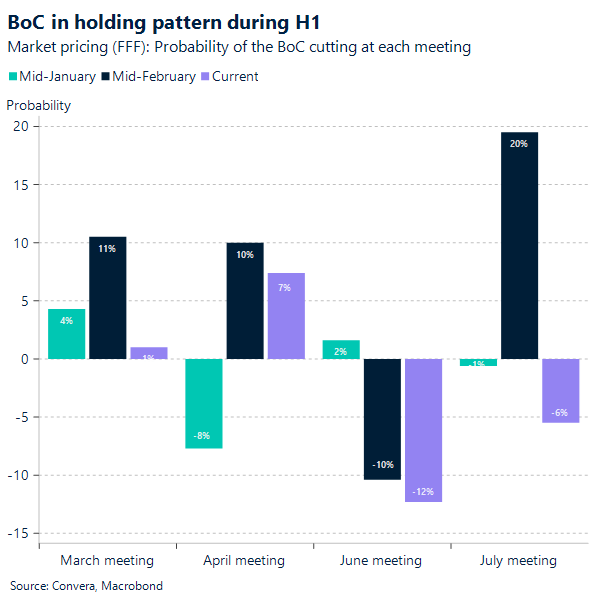

Canada’s two‑sided oil test

The Bank of Canada’s record shows a flexible, two‑sided response to oil moves: ease on sustained collapses that hit growth and lean against persistence when price pressures risk entrenchment. In January 2015, the Bank delivered a surprise 25 bp “insurance” cut as the oil slump threatened activity and inflation. Governor Poloz later described a “two‑track” economy, with resource weakness dragging while non‑resource sectors recovered more slowly than hoped.

BoC’s framework in December 2021 formalized the flexibility: a symmetric 2% CPI target within a 1–3% band, with an explicit nod to maximum sustainable employment and shock‑dependent horizons back to target. Through 2022’s “perfect storm” of commodity and supply shocks, the Bank tightened quickly and emphasized the 1970s lesson on keeping expectations anchored.

The current shock cuts both ways for Canada. Higher crude supports national income and royalties, yet it also squeezes households through fuel and food, so the net macro impact depends on duration and pass‑through. The global picture is severe: the IEA describes unprecedented disruption around Hormuz, which amplifies price volatility and complicates the forecast. Governor Macklem has already flagged increased financial and energy market volatility tied to the conflict.

Into today’s decision, the policy rate sits at 2.25% and markets expect a hold. The likely message is steady policy with a firmer warning on upside inflation risks from energy, paired with a reminder that the Bank will adjust if core pressures broaden or expectations drift. If the oil shock proves brief, the control range and flexible horizon allow the Bank to tolerate a temporary headline bump while monitoring real‑income effects and credit conditions. If disruption endures, guidance can tighten quickly, but as in past episodes the Bank will seek evidence of persistence before changing course.

For the scheduled presser we should expect Macklem to acknowledge the oil shock, potentially show scenario analysis, and keep the 2% anchor front and center while Canada’s two‑sided oil exposure plays through.

Against this backdrop, the notion of “CAD exceptionalism”, with oil support cushioning the Loonie, should be challenged amid broad USD strength and softer domestic data. Even a de‑escalation‑driven risk‑on turn would likely see CAD lag higher‑beta G10 rebounders once the conflict premium fades. That view aligns with a BoC hold at 2.25% and guidance that tolerates a temporary headline bump while stressing that any policy shift hinges on core breadth and expectations, not the crude tape, keeping near‑term USD/CAD choppy and headline‑driven.

In practice, CAD should keep tracking oil headlines but stay range‑bound if the Bank maintains a measured hold and the market continues to reward the dollar’s geopolitical role; only when supply lanes normalize and domestic data improve should the mean‑reversion map translate into more durable CAD gains.

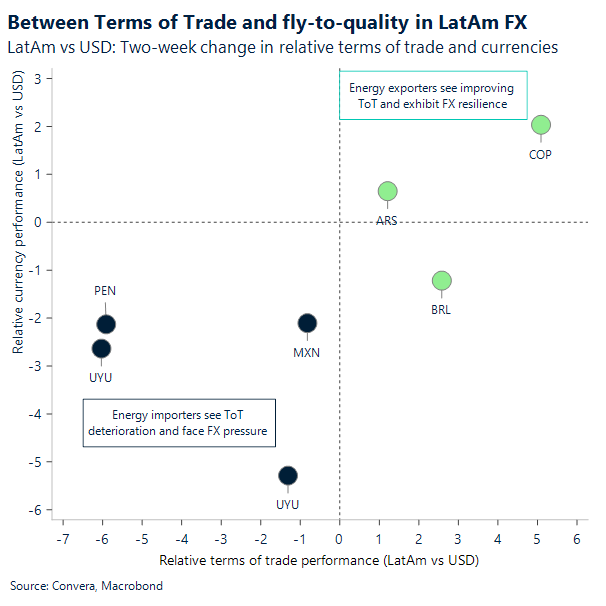

Shifting dynamics in LatAm FX

The recent spike in geopolitical tensions has pushed emerging market volatility higher and disrupted the previously stable carry trade environment. Despite this broader uncertainty, the FX divide between energy exporters and importers is playing out in LatAm as well. The Brazilian Real sits firmly on the resilient side of this spectrum. Benefiting from a positive shift in its terms of trade, Brazil is leveraging its status as a major commodity and oil exporter to provide a solid foundation for its currency. Alongside these robust export dynamics, the BRL continues to be supported by attractive carry, offering a helpful buffer against recent market headwinds.

The Mexican Peso, however, is navigating a much trickier landscape as an energy importer facing heightened global uncertainty. This recent risk-off environment hit the MXN, sparking intense selling pressure that erased most of its early-year gains and pushed trading levels from the lower 17s up past 18, before recently stabilizing near 17.7. Domestically, the Mexican economy actually remains quite stable, with inflation in check and the government expected to use oil revenue windfalls to smooth out consumer gas prices. Ultimately, the Peso’s primary vulnerability is external. It remains highly sensitive to risk-on environment, but if broader market conditions manage to stabilize, the MXN looks like a candidate to bounce back from these recent dips.

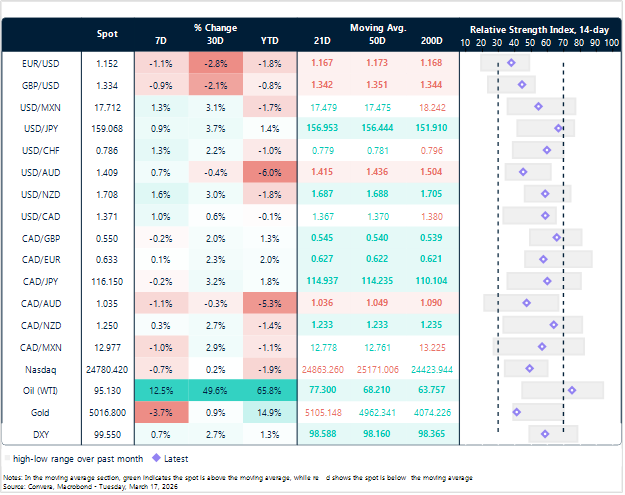

Market snapshot

Table: Currency trends, trading ranges & technical indicators

Key global risk events

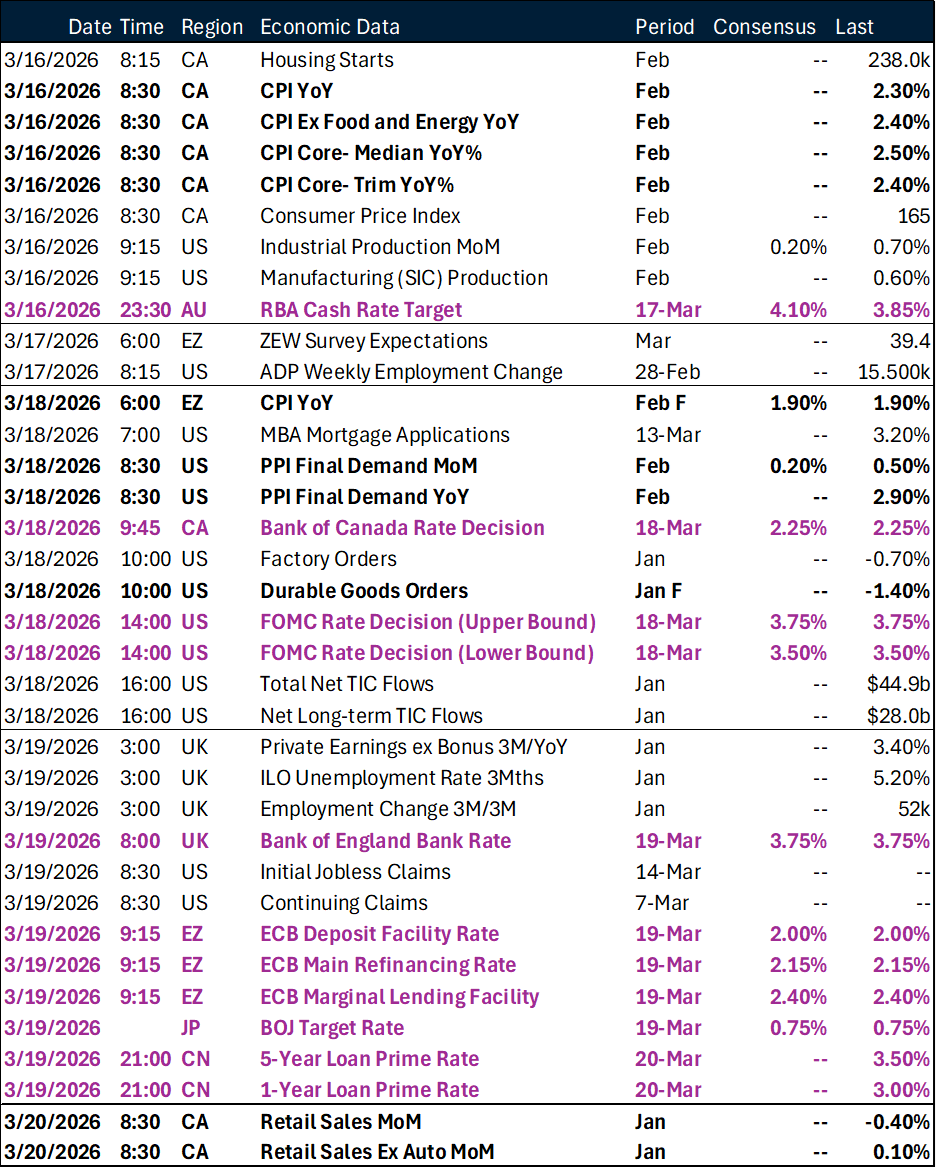

Calendar: March 16 – 20

All times are in EST

Have a question? [email protected]

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.