Written by Steven Dooley and Shier Lee Lim

Check out our latest Converge Market Update Podcast covering the global market’s start to 2024, central bankers’ fight against investors, the US macro outperformance, China’s watershed moment and geopolitical developments featuring global macro strategist, Boris Kovacevic.

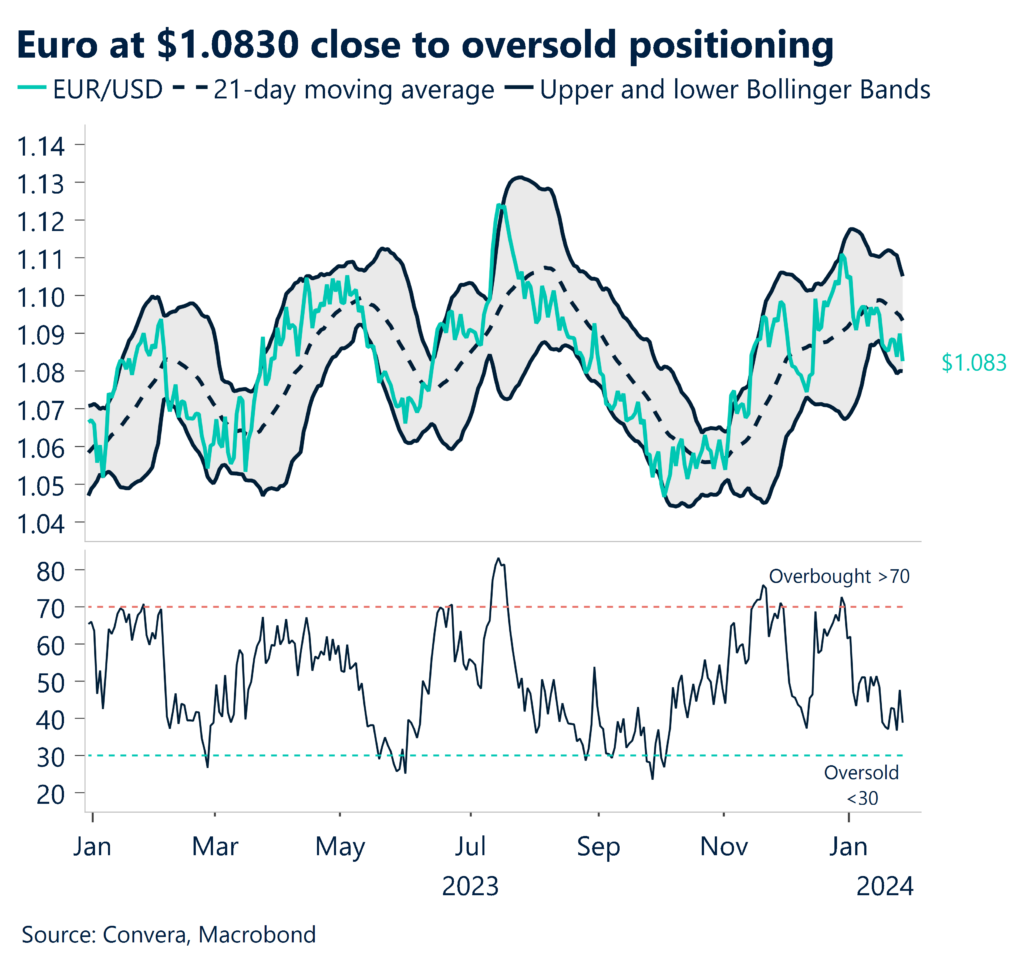

EUR/USD at six-week lows after ECB

The euro fell versus most currencies overnight after the European Central Bank’s policy meeting suggested the ECB was nearing a move to cut European interest rates.

The ECB kept interest rates on hold – with the main refinancing rate at 4.50% – but commentary from the ECB president Christine Lagarde warned that economic risks were now “tilted to the downside”.

Financial markets now see two 25-basis point cuts priced in by mid-year.

The EUR/USD fell 0.5% to six-week lows.

The euro was lower in other markets with the NZD/EUR nearing six-week highs and the EUR/SGD nearing six-week lows.

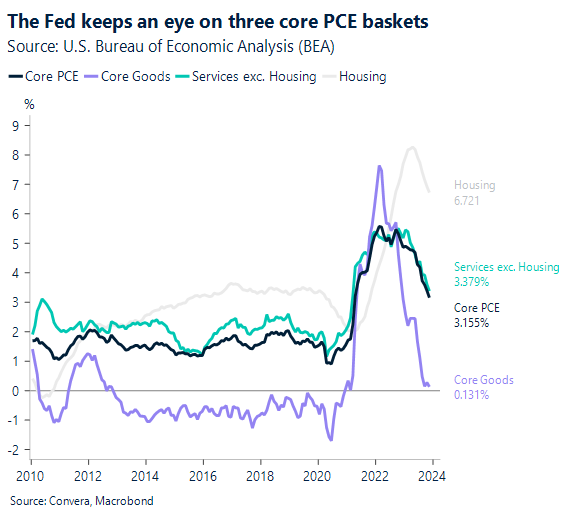

PCE key for Fed

Otherwise, the US dollar was stronger again overnight after a better-than-expected December-quarter GDP number. The USD index gained 0.2%. However, the USD index continues to find resistance at both the six-week highs and the 200-day moving average.

Tonight’s US inflation report – personal consumption and expenditure (PCE) – is critical for expectations around the Federal Reserve’s next move – and market sentiment more generally.

The PPI’s pertinent components and variations in item weightings allowed us to estimate another mild print of 0.154% m-o-m for monthly core PCE inflation in December, despite a 0.3% m-o-m increase in the core CPI.

The 3-month and 6-month annualized core PCE inflation would continue to decrease to 1.45% (from 2.16% in November) and 1.83% (from 1.87% in November), respectively, if our projection comes to pass.

Core PCE inflation most likely refrained from dramatically returning due to weakness in rent inflation and non-auto core goods prices. Nevertheless, we anticipate that supercore component inflation will increase to 0.255% m-o-m in December from 0.124% in November.

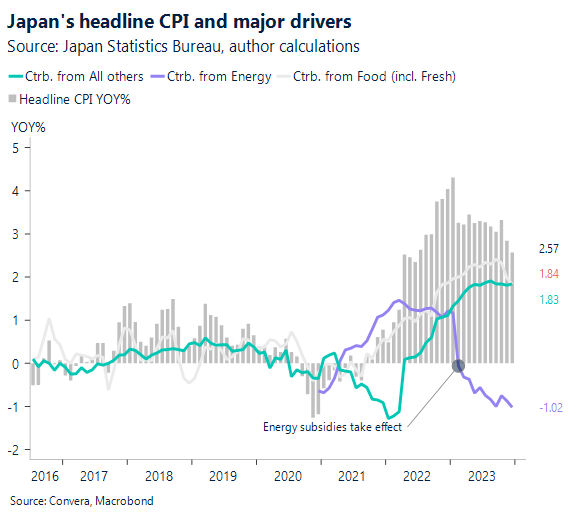

Japan inflation due

Before US inflation, Japan January 2024 Tokyo CPI is due.

We project 1.7% year-over-year inflation in the Tokyo Ku-area core CPI (all items minus fresh food) in January 2024, down from 2.1% in December 2023.

With the exception of fresh food and energy, we predict that the BOJ’s interpretation of core-core CPI inflation will be 3.1% year over year, down 0.4 percentage points from 3.5% in December.

Tokyo core CPI inflation looks likely to have slowed in January, caused in part by the MIC’s version of the core-core CPI (all categories minus food (excluding alcoholic drinks) and energy), core foods (food excluding fresh food, and energy).

While the USD/JPY has recently weakened, the short-term USD/JPY support range of 145.97–146.97 would need to be broken to validate this trend reversal.

Euro down after ECB

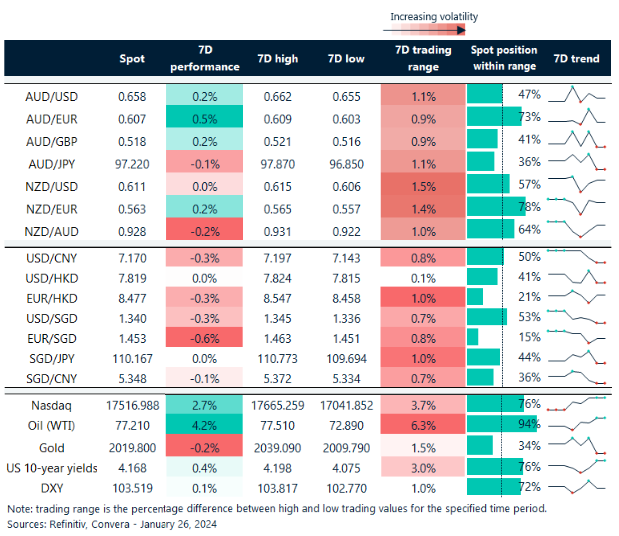

Table: seven-day rolling currency trends and trading ranges

Key global risk events

Calendar: 22 – 27 January

All times AEDT

Have a question? [email protected]

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.