Written by Steven Dooley, Head of Market Insights

Global overview

The greenback fell overnight as bond yields drifted lower despite a stronger US GDP number. The ECB kept rates on hold. The USD/JPY will be closely watched after the pair broke above 150.

ECB on hold

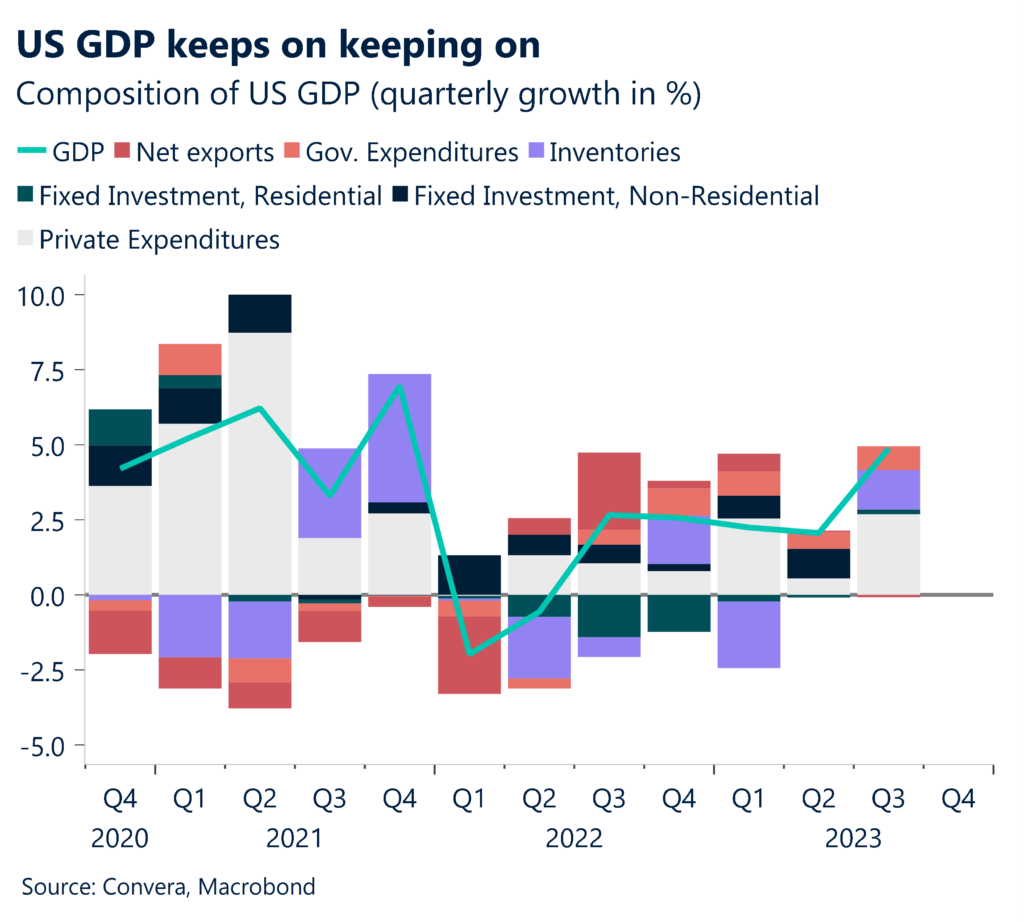

The US dollar was weaker overnight despite a stronger result from September-quarter GDP as bond yields eased.

US GDP was better-than-expected at a roaring 4.9% in annualised terms for the quarter. The market had forecast 4.5%.

However, some weaker inflation numbers within the GDP numbers saw the US ten-year bond yield reverse again from the 5.00% level. The greenback fell.

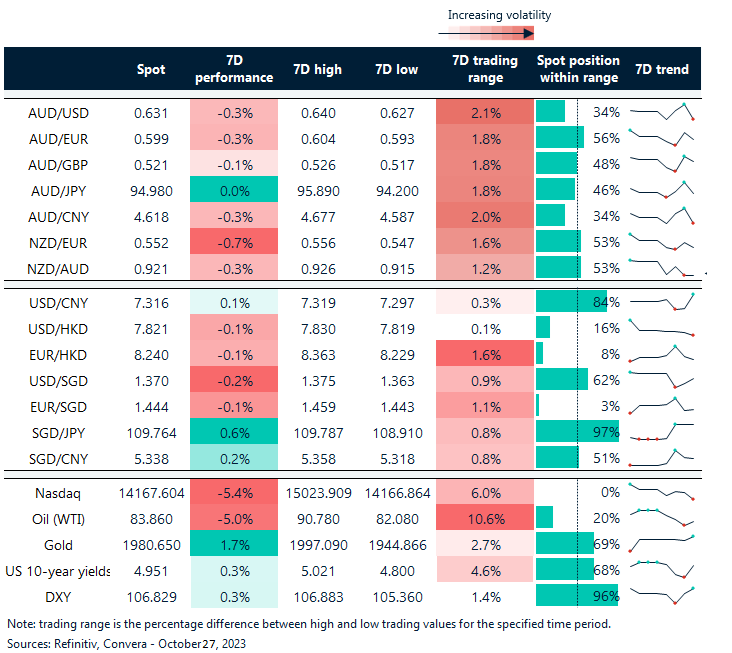

The AUD/USD and NZD/USD both gained 0.3%. The USD/SGD and USD/CNH both fell 0.1%.

The EUR/USD fell 0.1% after the European Central Bank kept rates steady. The GBP/USD gained 0.1%.

USD/JPY breaks 150

The USD/JPY climbed above 150 overnight and the key risk now is for intervention from the Ministry of Finance. In order to stop the yen’s sell-off, the MoF might step in somewhere between 150 and 155 levels.

Japan’s Tokyo CPI Ex-Fresh Food is likely to see 2.8% YoY inflation in the Tokyo core CPI in October 2023, up from 2.5% in September. Tokyo’s core-core CPI inflation might climb from 3.8% to 3.9% this month according to the BOJ’s interpretation. October Tokyo CPI energy inflation is expected to be -14.4% YoY, which is a slower rate of price fall than September’s -18.7%.

In the energy sector, we anticipate that although gasoline costs will press downward on inflation, electricity and city gas prices will push inflation higher. The main reason we anticipate an increase in inflation in electricity and city gas prices is that the government will reduce its subsidies for gas and electricity by half, effective October 1st. That said, stronger (and higher) inflation expectations are likely required for 2% inflation target to be sustained.

PCE due

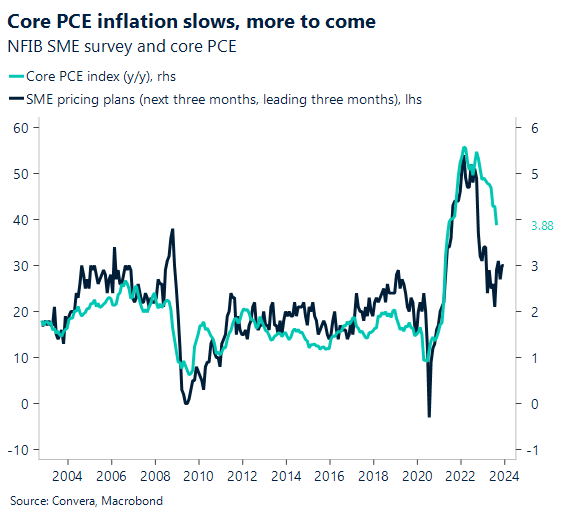

US personal consumption and expenditure is due Friday night. The market projects September core PCE inflation at 0.3% MoM, up from 0.1% in August, based on PPI and CPI data.

On an unrounded basis, it would be the highest monthly core PCE inflation figure since March of this year. Backward adjustment to PPI’s airline tickets indicates there may be a chance of somewhat negative revisions to the August core PCE price index, even if we do not anticipate any changes to the previous months.

Supercore components are the primary cause of the anticipated increase of core PCE inflation in September.

That said, we do expect Core PCE inflation to slow (see chart green line), led by SME pricing plans (dark blue line) by 3 months.

USD, EUR lower

Table: seven-day rolling currency trends and trading ranges

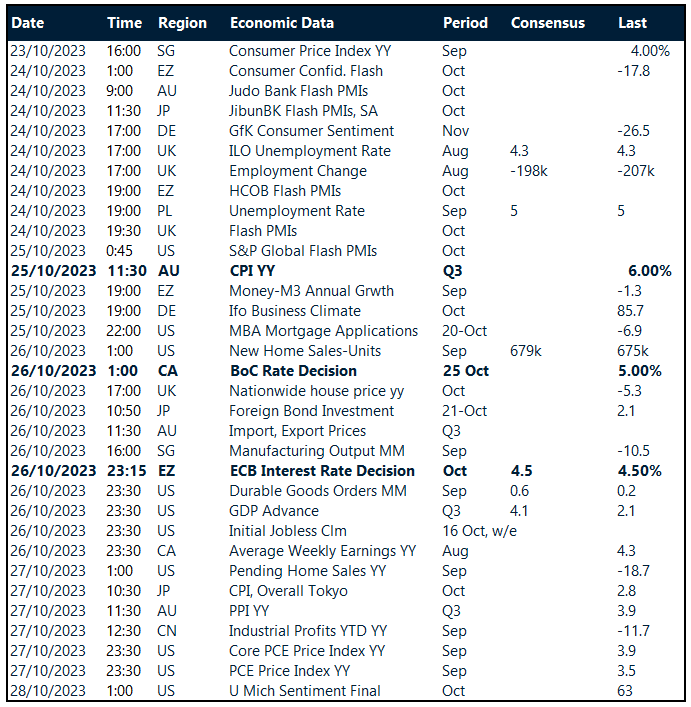

Key global risk events

Calendar: 23 – 28 October

All times AEDT

Have a question? [email protected]

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.