Written by Convera’s Market Insights team

Dovish signals mount ahead of ECB decision

Ruta Prieskienyte – FX Strategist

Wednesday’s Eurozone data releases have helped to cement the case for the ECB to pause its tightening cycle, which saw the deposit rate move to an all-time high of 4%. The common currency continued to lose momentum and shed a further 0.2% on the day, following a large correction on Tuesday amid growing signs of a deteriorating economic outlook and general risk-off mood in markets.

Germany’s Ifo Business Climate indicator surprised with a strong rebound in October, in a stark contrast to the declining PMIs seen on Tuesday. The indicator increased to 86.9 in October, up from 85.7 in September, marking the first increase in six months. It also represented the highest level in the past three months as companies have grown less pessimistic about both their expectations for the coming months and their current business situation. While one month does not constitute a trend, the current index is still consistent with slowing GDP growth, thus indicating that Europe’s largest economy is now in a double-dip technical recession. Elsewhere, the money supply data reinforced the message from the ECB’s bank lending survey that tighter monetary policy is now weighing on private loan growth. M3 money supply fell by 1.2% y/y in September, rebounding marginally from a 1.3% decline in August. The growth in loans to the private sector slowed further and will soon fall into negative territory on a year-over-year basis. The slowdown in private sector lending is consistent with the message from the ECB’s bank lending survey that tighter monetary policy is now being forcefully transmitted to the economy.

Yesterday’s deteriorating risk sentiment has left its mark on the euro as well. European stocks are currently hovering near their 6-month lows, indicating low risk appetite. Such an environment has made it hard for the euro to advance much beyond the $1.06 level versus the US dollar. Overall, the euro could stay under some pressure on expectations that the ECB may have to sound more dovish given the deteriorating economic outlook. A continued negative momentum in EUR/USD is likely on the cards going into the ECB announcement later today.

Dovish BoE outlook weighs heavy on pound

George Vessey – Lead FX Strategist

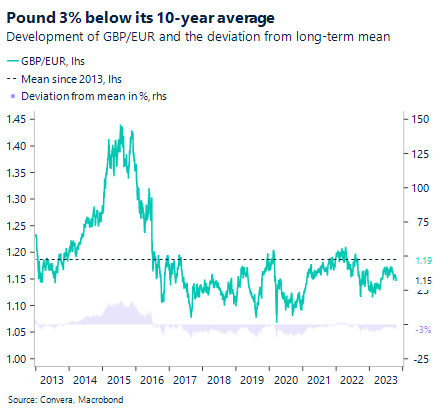

The British pound extended Tuesday’s losses after gloomy economic data affirmed the view that the Bank of England (BoE) will likely hold rates at 5.25% when it announces its policy decision next week. The economic outlook is increasingly weakening in the UK. PMIs remain in contractionary territory across the board, unemployment has increased to 4.2% (up from lows of 3.5%), retail sales and GDP growth is muted. GBP/USD has fallen to a 3-week low and looks poised to test its 2023 low nearer $1.20, whilst GBP/EUR is on track for a second monthly decline in a row and now sits 3% below its 10-year average.

The probability of a BoE rate hike next Thursday has fallen from 50% to less than 10% in just a few weeks. There’s also only a 30% chance the BoE will hike again at all in this tightening cycle according to money market pricing. Falling interest rate expectations have weighed heavily on sterling, but relative economic growth rates are also playing their part due to their influence on how long interest rates will remain high. At the start of the month, no BoE rate cuts were being priced in for 2024, now over 30 basis points are following a slew of gloomy flash PMIs on Tuesday. Although PMIs are not a perfect predictor of economic growth and preliminary results especially should be taken with a pinch of salt, it’s obvious that UK economic momentum is slowing.

Like other central banks, the BoE remains highly data dependent, so if data continues to disappoint and if headline inflation continues to fall markedly lower in October, given base effects from last year’s increase in energy prices, then the conclusion of the BoE’s hiking cycle is likely to limit any sterling recovery in the short-term.

Mortgage rates hit 23-year high

Boris Kovacevic – Global Macro Strategist

Global investors have been facing multiple headwinds in recent weeks with the US earnings season in full swing, treasury volatility remaining at elevated levels and geopolitical developments being monitored on a daily basis. At the same time, investors have continued gauging the impact of tighter global financial conditions on consumers and companies. The verdict for yesterday’s news patch has been negative, explaining the weak risk taking across financial markets.

The Nasdaq closed at its lowest level in more than four months, having shed around 10% of its value since July. Both oil and gold pushed higher, after being less bid at the start of the week, due to geopolitical tensons having eased a bit over the weekend. The US dollar profited from commodity prices rising and equities falling, while getting support from the fixed income space. US 10-year treasury yields continued their ascent, closing only slightly below the important 5% mark. The Greenback rose for a second consecutive day and is now once again less than 1% away from its multi-month high reached in October.

Economic data has been scarce. The rise of mortgage rates to a new 23-year at 7.9% has continued pressuring mortgage activity, with applications for new housing loans falling to the lowest level since 1995. However, the new housing market continued its more than 1-year long recovery. New single-family home sales surged by 12.3% in September, reaching the highest level since February 2022. The conclusion of the last two week’s data patch has been that US data remains, on average, better than expected. While the effect of high interest rates is working its way through the economy, the pass through has been significantly slower than in the UK and Eurozone. Economists are expecting the upcoming GDP print for Q3 to be a testament to this US exceptionalism narrative with growth forecast to come in at 4.3%, the strongest pace in more than two years.

Pound slips to 3-week low versus USD

Table: 7-day currency trends and trading ranges

Key global risk events

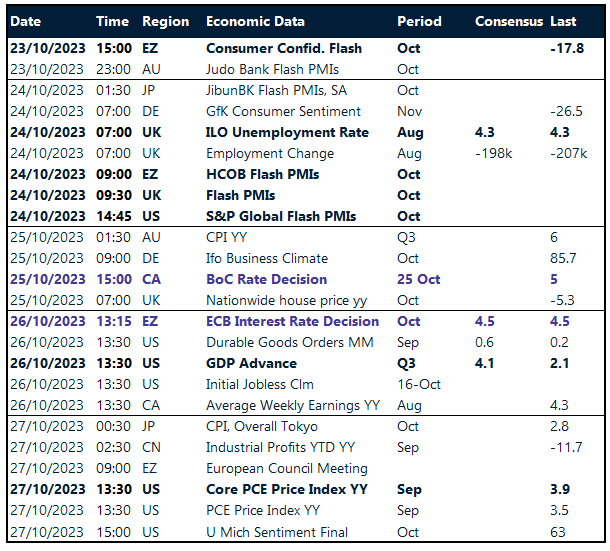

Calendar: October 23-27

Have a question? [email protected]

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.