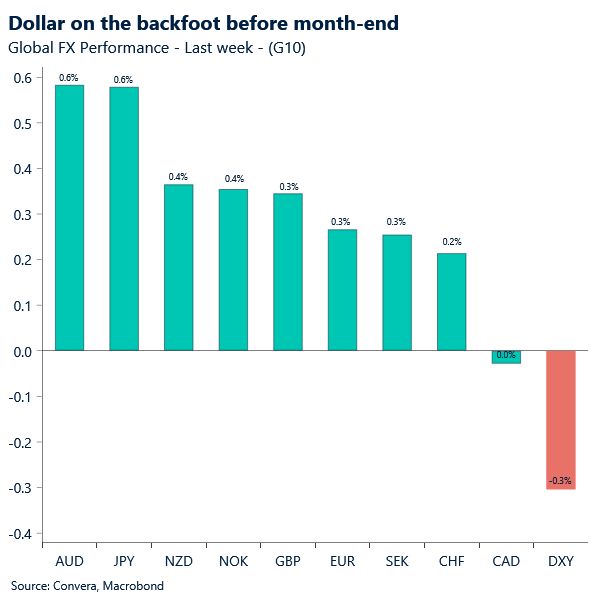

USD: US-Japan trade dialogue lifts yen, hits buck

The US dollar index is flirting with its 21-day moving in average. If it breaks below, we could witness an extended period of dollar softness in the near-term. The latest catalyst weighing on the buck follows discussion between the US and Japan on trade and exchange rates. The rhetoric appears optimistic on the former, while FX traders are reading the latter as a reminder that the US administration would prefer a weaker dollar.

President Trump struck a more conciliatory tone on trade during his meeting with Japanese Prime Minister Sanae Takaichi. The yen outperformed all G10 currencies, buoyed by the meeting’s outcome and fresh signals from Japanese officials that they’re closely watching the impact of currency weakness. Separately, Treasury Secretary Scott Bessent met with Japan’s Finance Minister Katayama to discuss exchange rates — a joint signal that both sides are uncomfortable with further yen depreciation, but also that the US maintains its preference for a softer dollar.

Markets remain upbeat following constructive trade talks and softer US inflation. September’s CPI showed housing inflation cooling, with owners’ equivalent rent rising just 0.1% — its slowest pace since 2020. This gives the Fed more room to ease, reinforcing expectations for a rate cut this week.

Despite the dovish setup, FX markets stayed calm. The dollar index (DXY) has traded within one standard deviation of its 3-month average nearly 80% of the time, reflecting low volatility. Even with two cuts priced in, USD remains firm — suggesting a sharper drop would require labour market deterioration, which isn’t evident yet. Attention now turns to the Fed’s ability to navigate with increasingly delayed data, though today’s Conference Board consumer confidence and expectations figures offer a timely read on household sentiment.

EUR: Euro lacking conviction, for now

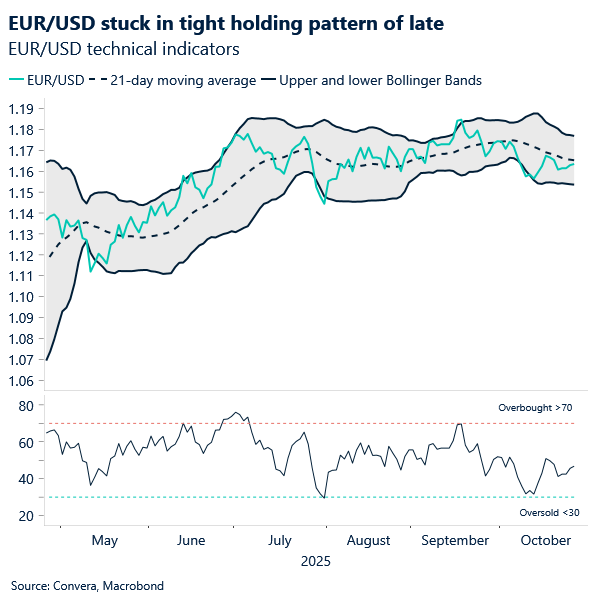

EUR/USD is up roughly 0.7% month-to-date, but the move reflects a lack of fresh catalysts rather than renewed conviction. The forces that drove euro strength earlier this year — softer US data and dovish Fed signals — have stalled, and with the US government shutdown ongoing, directional momentum remains limited. Trade optimism has helped prevent a break below $1.16, yet upside traction is clearly lacking.

Domestically, Germany’s Ifo business climate index rose to 88.4 in October, driven by a notable jump in expectations — now at their highest since mid-2022. However, the current assessment fell for a third straight month, highlighting persistent economic fragility. Optimism from Germany’s spring fiscal pivot has faded, with external headwinds — including US tariffs and euro strength — weighing on sentiment. Thursday’s Q3 GDP print will be pivotal. After a Q2 contraction, another negative reading would confirm a technical recession and likely test the euro’s resilience.

That said, while a dovish surprise from the Fed on Wednesday remains a low-probability scenario, it’s not off the table. Should policymakers strike a more accommodative tone than expected, EUR/USD could break back above key technical levels clustered around the upper $1.16s — potentially setting the stage for another test of $1.18.

GBP: Sleepy sterling searching for signals

The British pound is trading below its 21-day moving average versus both the euro and the US dollar — a signal that near-term momentum has turned cautious. This technical setup suggests waning bullish conviction, with traders likely reassessing the UK’s macro outlook amid fiscal concerns and diverging central bank paths. Unless incoming data or policy signals shift sentiment, sterling may struggle to regain traction in the short term.

However, zooming out and looking at our annual FX report – the technical picture for GBP/USD is quite striking. GBP/USD has held above its 100-month moving average for two straight months — something we haven’t seen since before the financial crisis. Even more notably, the 21-month average has crossed above the 100-month for the first time since 2003. Back then, we saw another year of gains north of 7%.

Whether history repeats is a tougher call. In the early 2000s, the UK had stronger growth, higher yields, and a supportive policy mix. Today, growth is much more subdued. But short-term UK rates are still relatively attractive versus other G10 currencies. Add in a more dovish Fed, and you’ve got a setup that could push sterling higher, especially if the Bank of England (BoE) holds its hawkish line and maintains credibility.

But that’s a big “if.” If inflation cools too quickly or the labor market softens, markets could start pricing in more BoE rate cuts — and that would flip the narrative fast. Plus, with US growth reasserting itself and most Fed easing already priced in, the dollar could regain strength. On its own, that might not drag GBP/USD below $1.30 — but if you layer in fiscal concerns and gilt market stress, a move back into the $1.20s isn’t off the table either.

In FX, conviction is rare and certainty rarer still — the only constant is recalibration.

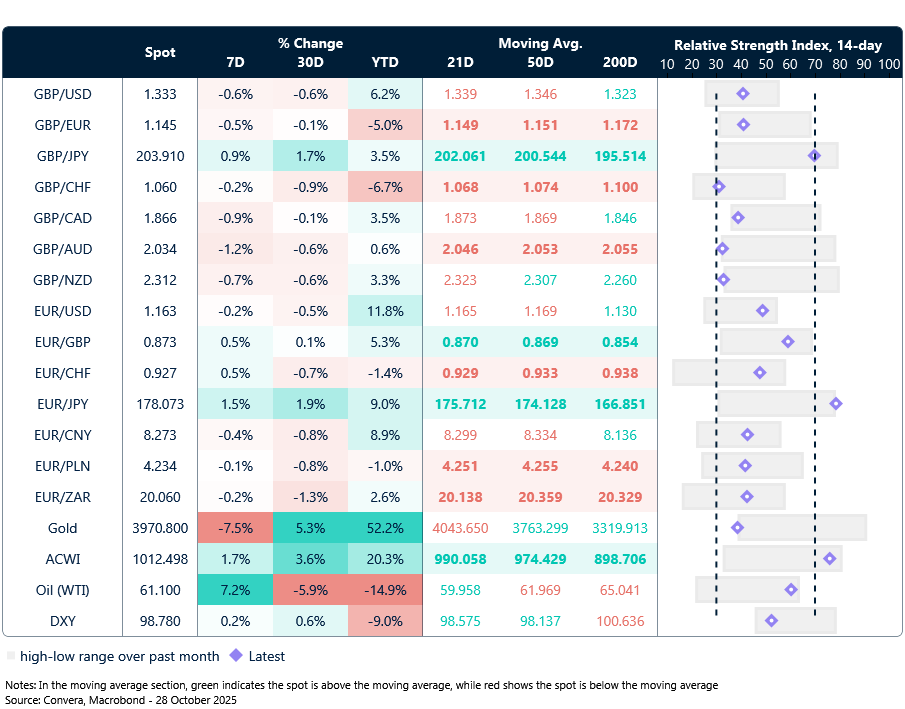

Gold slumps 7.5% in a week

Table: Currency trends, trading ranges and technical indicators

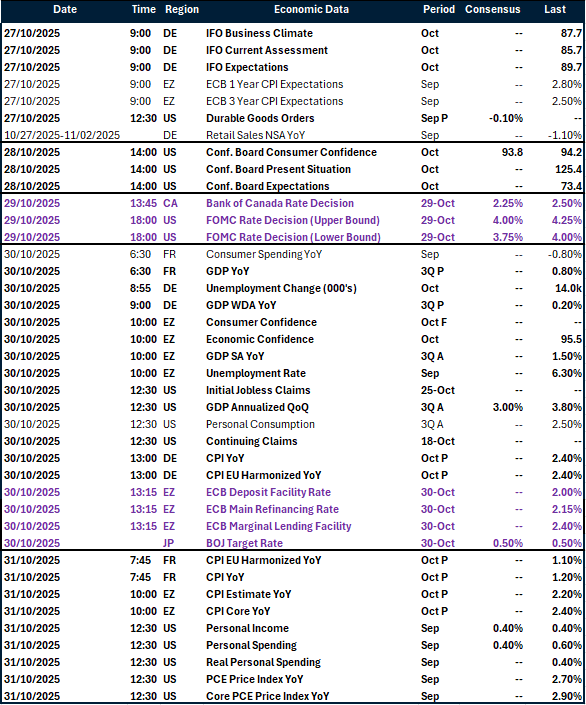

Key global risk events

Calendar: October 27-31

All times are in GMT

Have a question? [email protected]

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.