Written by Convera’s Market Insights team

Check out our latest Converge Market Update Podcast which looks at how recent economic data has called into question the timing of rate cuts and triggered some significant volatility across financial markets. Could this become more frequent as central banks begin policy easing this year? Join Lead FX Strategist George Vessey as he breaks down the latest in the global macroeconomic and FX landscapes.

First weekly drop of 2024?

George Vessey – Lead FX Strategist

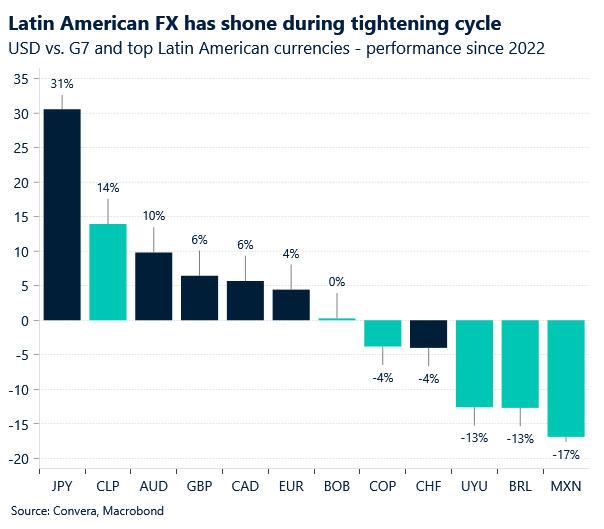

The US dollar index looks set to record its first weekly drop in 2024 despite rebounding from a 3-week-low yesterday after resilient US economic data helped pare dollar losses. After hitting a 3-month high last week, the US currency has been largely consolidating, benefiting from divergences with other countries as the US economy looks relatively stronger. In the short-term, the USD might continue profiting from its status as a high yielder and high growth currency, but we think upside remains limited. USD/JPY has risen over 30% over the last year or so and GBP/USD remains 6% weaker since the global tightening cycle really kicked off in early 2022.

Flash US manufacturing PMI rose to 51.5 in February from 50.7 in January, beating forecasts of 50.5. The reading pointed to the strongest growth in the factory sector since September 2022, as output increased for the first time in three months, and at the fastest pace since April 2023, due to stronger client demand and a sharper uptick in new orders which rose the most since May 2022. However, despite ongoing US economic resilience and rising US yields, there’s clearly some signs of fatigue emerging in terms of USD demand and the dollar seems more sensitive to weak data compared to strong. We saw US jobless claims unexpectedly fell after the PMI data dump, which sent the dollar lower across the board once again.

There are no top tier economic data releases out today as market participants brace for next week’s Personal Consumption Expenditures reports – the Fed’s preferred measure of inflation.

UK recession in rearview mirror

George Vessey – Lead FX Strategist

Stronger-than-expected UK PMIs yesterday suggests the technical recession in the UK is already over. UK private sector output expanded for the fourth consecutive month, the fastest since May 2023, supported by a strong service sector (PMI of 54.3), which is performing better than the Eurozone (PMI of 50). GBP/EUR remains south of the €1.17 handle though, whilst GBP/USD remains north of $1.26, having staged a sharp reversal from a 3-week high above $1.27 – as the currency pair braces for its best week of 2024.

UK headline PMI figures came in stronger than expected but it’s inflation that is more important for the Bank of England (BoE) and the warning in the accompanying PMI data is that service-sector price pressures remain high. This will likely delay the chance of a rate cut by the BoE any time soon. Indeed, although services inflation and wage growth should show further progress lower by the summer, we expect both to remain sticky in the near-term, so the pound should remain supported by favourable yield spreads. Money markets are now pricing in just over 60 basis points of rate cuts by the BoE this year, down from 75 basis points last week. UK 2-year yields are up over 60 basis points since the start of the year and the pound has now appreciated against 60% of 57 global peers month-to-date, up from 40% at the start of February.

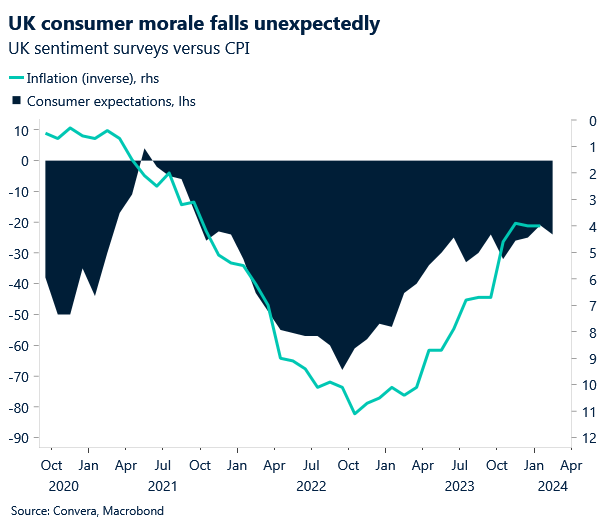

The pound remains steady this morning despite data showing consumer sentiment fell for the first time in four months in February as households took a gloomier view of their recent personal finances and the broader economic outlook. GBP/USD looks to have found some decent support at its 50-week moving average and is showing signs of another run towards the top of its 2-month range. The 50-day moving average, at $1.2675, is the next upside barrier in our eyes, after which the 200-week moving average at $1.2850 comes into focus.

Rate cuts are coming

George Vessey – Lead FX Strategist

As well as flash Eurozone PMI data for February, the minutes of the European Central Bank’s (ECB) policy meeting were released yesterday and confirmed that rate cuts are on the horizon, but highly unlikely by Spring. The ECB will want to wait for final first quarter data on inflation, output and wages before pulling the trigger. After rising to a 3-week high, EUR/USD recoiled back towards $1.08 and under its 50-week moving average.

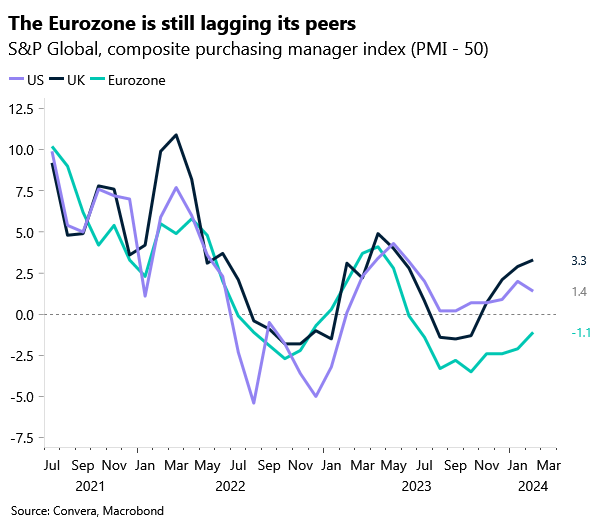

The Eurozone’s composite PMI figure for February rose from 47.9 to 48.9, indicating that the bloc’s economic slump is easing. The gap between Eurozone economies is widening though, as France experienced the best PMI in nine months, while Germany’s decline accelerated for a fourth successive month, deeper into contraction territory. The Eurozone as a whole saw a stabilisation of output in the service sector, which offset a further steep downturn in manufacturing, but the bloc is still lagging that of the US and UK. In the ECB’s meeting minutes, whilst policymakers remain satisfied that the disinflationary process of 2023 will continue, the assessment of economic developments sounds more cautious. The minutes indicated that the dovish shift in the ECB council is underway but remains gradual as a fair share of the council cautioned against the premature easing of policy.

The euro is on track to record its best weekly performance against the US dollar since late last December in the wake of a 5-week slump as EUR/USD continues to grapple with its 50-week moving average around $1.0840. A strong finish to February increases the chances of the currency pair staging a recovery back towards $1.12 by the summer.

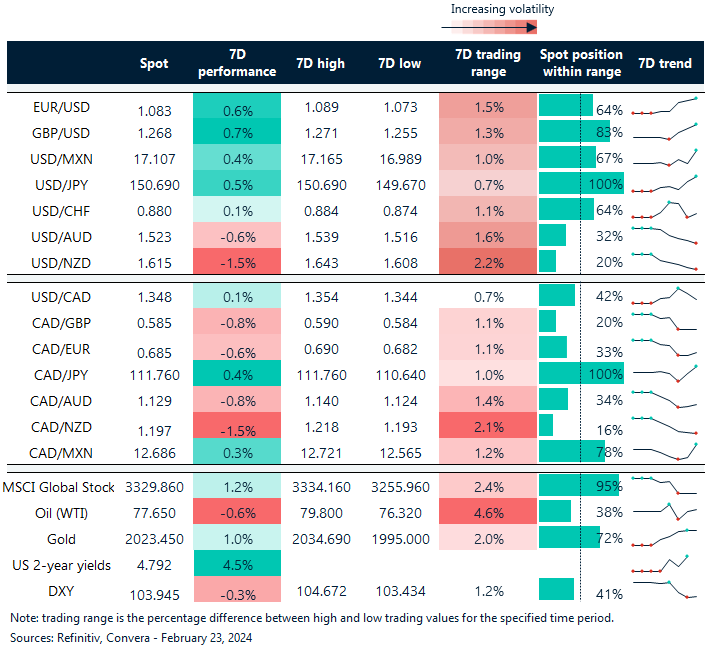

Dollar index on track for first weekly fall of 2024

Table: 7-day currency trends and trading ranges

Key global risk events

Calendar: February 19-23

Have a question? [email protected]

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.

Join us for Convera Live! A series of in-person events discussing the future of global payments.