Global overview

Tepid risk sentiment along with stubbornly high inflation across the Atlantic helped the U.S. dollar keep above recent 5-week lows against a basket of currencies. Sterling fell from one-year highs against the greenback after the latest UK inflation figures failed to improve. British consumer prices steadied at an elevated annual pace of 8.7% in May, cementing the case for the Bank of England Thursday to hike borrowing rates by at least 25 basis points from current 15-year highs of 4.50%. Optimism about the outlook for global growth has dissipated this week after China cut interest rates to help shore up weakness in the world’s No. 2 economy. The buck is shaking off some of its recent declines ahead of key congressional testimony today and tomorrow on Capitol Hill by Fed Chair Jerome Powell. Mr. Powell may not shed much new light on the road ahead for American monetary policy, but he could make the case for lending rates to remain higher for longer, a theme that has helped to undercut bouts of dollar weakness this year. Canada’s dollar hovered near nine-month highs ahead of data today on Canadian consumer spending.

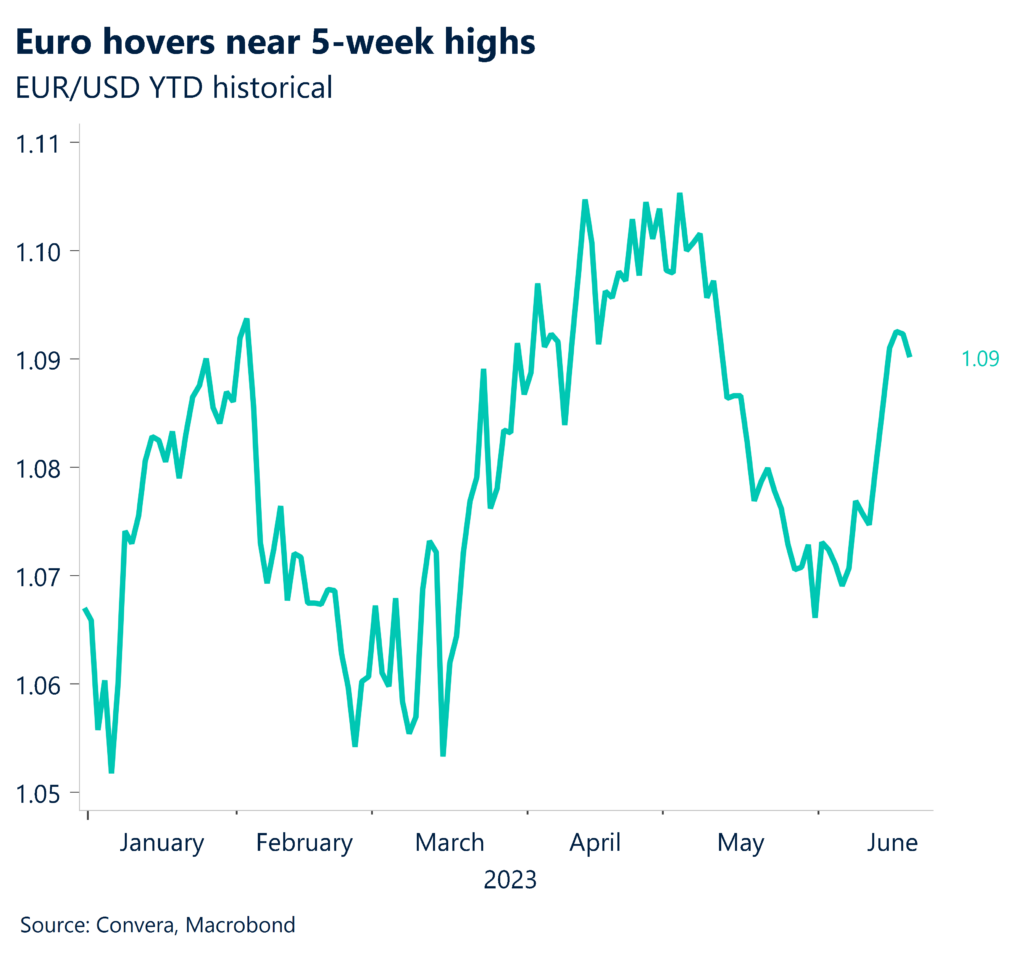

Euro ticks below mid-May high

The euro held below last week’s five-week high against the U.S. dollar on caution ahead of remarks today and tomorrow by the head of America’s central bank. Upward momentum for the euro petered out after it latest surged stopped just short of the psychologically important 1.10 threshold. The euro remains underpinned by the view that the ECB could outpace the Fed in raising interest rates over the latter half of 2023, an outlook that if realized would narrow the buck’s yield advantage.

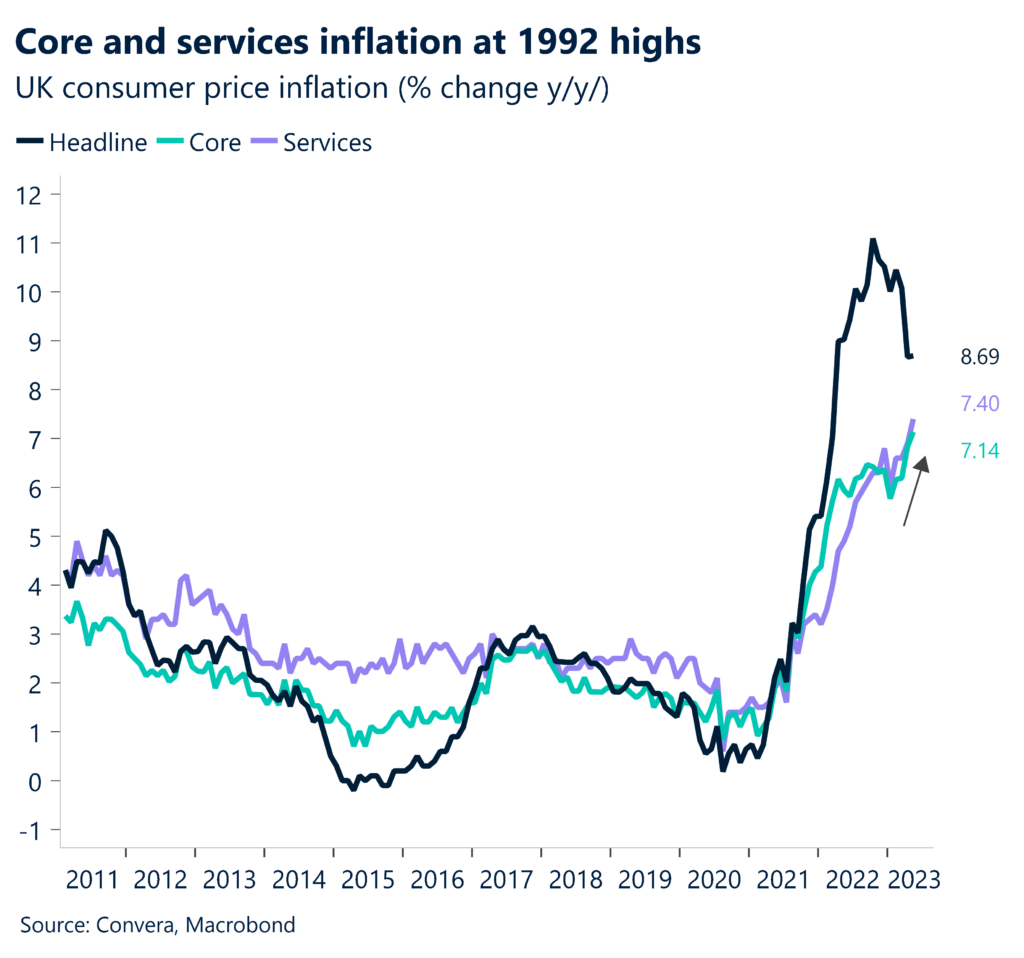

Sterling’s surge cooled by unexpectedly hot UK inflation

Sterling fared choppy after domestic inflation unexpectedly held at a stubbornly hot 8.7% annual rate in May, wrongfooting expectations to cool to 8.4%. The news was even grimmer for underlying inflation which accelerated by 7.1% over the last 12 months, the fastest pace in over 30 years, from 6.8%. While inflation has slowly receded from 41-year highs above 11% last year, it remains the highest among major economies. Markets are spooked as chronically hot inflation means a higher risk of the Bank of England raising rates Thursday by more than 25 basis points from 4.50% and suggests rates may need to climb as high as 6% by year-end. While the prospect of higher rates tends to buoy sterling, they also carry downside risks for growth and cast a darkening cloud over the economy.

Robust Canadian spending boosts C$

Canada’s dollar firmed and kept within striking distance of nine-month highs against its U.S. rival after better-than-expected news on the country’s consumer kept the door open to higher interest rates. Retail sales topped forecasts with a 1.1% rise in April that partially offset a 1.5% fall in March which compared to forecasts of a 0.2% increase. Canada forecast retail spending in May would rise 0.5%. Fresh signs of a resilient Canadian economy kept Ottawa on track to raise rates from 22-year highs of 4.75% as soon as its coming meeting on July 12. USD/CAD last week fell to around 1.3175, its lowest level since September 2022.

Dollar off lows ahead of Fed chair’s remarks

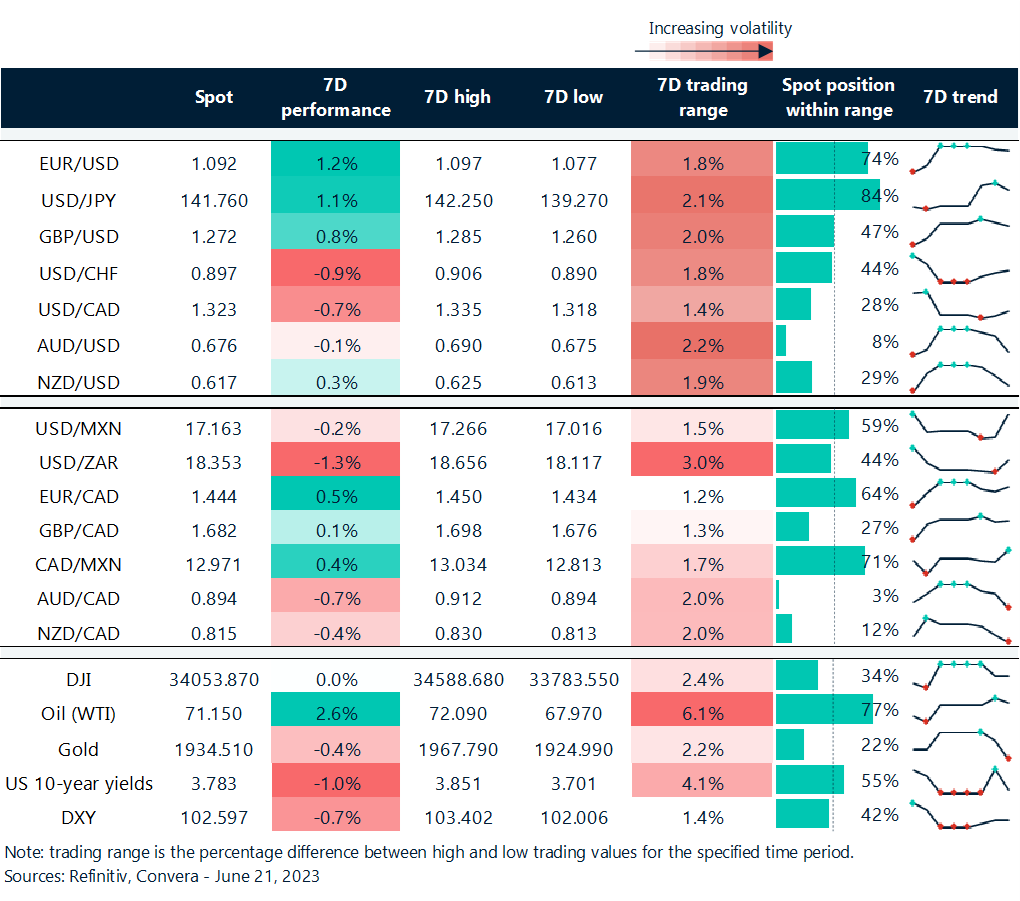

Table: rolling 7-day currency trends and trading ranges

Key global risk events

Calendar: Jun 19-23

Have a question? [email protected]

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.