Lower inflation dents the dollars appeal

Global financial markets have been delighted by the positive after effect of the recent US inflation print, which showed consumer price growth falling to the lowest level in more than two years. EUR/USD struck a fresh 16-month high at $1.1250, while the S&P 500 index breached 4,500 on Thursday as US stocks climbed for a fourth day running, finding fresh 15-month highs.

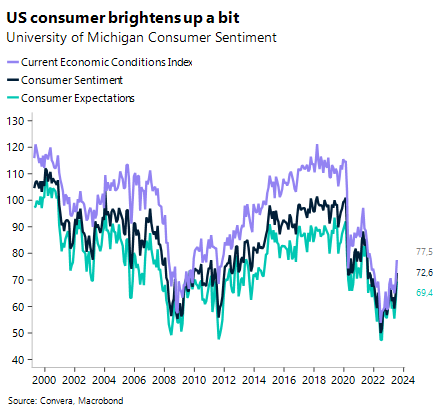

The risk rally did take a breather on Friday, with stocks and the euro pushed slightly lower against the backdrop of US two-year yields rising from 4.61% to 4.77% on the last day of the week. One reason for the push back can be found in investors probably deleveraging just before the weekend after multiple sessions of above 1% gains. Another factor might be the macro data itself, given that US consumer sentiment improved for a second month, rising to the highest level since September 2021, according to the Michigan University. The lower risk appetite on Friday, however, did not dent the euro’s weekly performance. EUR/USD continues to trade near the highest level since February of last year, having just finished its best week (+2.33%) since November 2022.

Looking back at the last week, we have been right in predicting a sharper-than-consensus inflation fall in the US. However, the dollar sell-off has been over proportional to what we would have expected given the current 1. yield curve, 2. rate differentials and 3. Fed pricing. A large contributing factor to the current period of euro strength has been the pro-cyclical capital rotation into risk assets like stocks and the euro and pound. Weaker inflation data has trumped the continued resilience of other US macro data. It will be interesting to see if this trend continues this week.

UK inflation to determine size of rate hike

Despite signs of a cooling UK labour market, we saw nominal wage growth stuck at record high levels, keeping the pressure on the Bank of England (BoE) to continue raising interest rates in its fight against inflationary pressures. This week, the UK inflation report will be published, and might clarify whether the August hike will be 50- or a 25-basis points. Sterling is taking a breather this morning after scaling fresh 16-month peaks above $1.31 last week.

The BoE’s June’s meeting made it clear that it is laser-focused on the consumer price index (CPI) and wage numbers. With wage growth continuing to beat expectations along with other macro data points and inflation figures also surprising higher in recent months, the hawkish repricing of UK rate expectations has bolstered the pound. That said, most of its rise last week was a function of a weaker US dollar, hence GBP/EUR actually suffered a weekly decline and GBP/JPY fell for a third week running. This week though, all eyes will be on UK inflation and we should see a notable dip in headline CPI, though this is largely because of base effects due to last June’s circa 10% surge in fuel prices. Food inflation should also decline modestly, not least because producer price inflation has been easing for several months now. Whilst core inflation is expected to slide too, it’s the services component that matters most to the BoE, and if this remains at its post-Covid high of 7.4%, then August’s BoE meeting will remain a close call. But if services inflation prints fresh cyclical highs, it will probably nudge the dial in favour of a larger 50-basis point hike, possibly supporting further sterling demand amid widening yield differentials.

GBP/USD has recovered over 21% since its record low last year and reclaimed the key $1.30 threshold, but if we analyse the post-Brexit period, the pound has spent more than 50% of its time below $1.30 against the US dollar. Currently, sterling is considerably above its 1-, 2- and 5-year average rates, but for how long will above-target UK economic and inflation data and rising rate expectations help sterling hold the crown as the best-performing major currency year-to-date. Extended USD weakness is a key upside risk, but looming recessionary fears cloud the outlook.

Will ECB hawkishness fade with falling inflation?

Europe has been left in the shadows with investors primarily focusing on developments in the US. The irrelevance of the old continent has, however, played into the cards of the euro, as investors mostly ignored the weaker-than-expected macro data out of Germany. It is important to note that most of the move higher in rate differentials (EZ vs. US) has been driven by factors outside the European Central Bank’s (ECB) control. The crucial factor going forward will be to determine what the ECB will do in the third quarter.

Some governing council members like Boris Vujcic have said that the September meeting continues to be data driven when it comes to the possibility of a further rate hike. While markets fully price in an increase of the benchmark interest rate by 25 basis points in July, the meeting after that seems to be more nuanced. Other policymakers have become more cautious with their hawkish language as recent data suggests weaker inflationary pressures going forward as the manufacturing sector falls deeper into recession. Last week, Eurozone industrial production rose less than economists had anticipated in May, with output increasing 0.2% on a monthly basis. Looking back at the last twelve months, production fell 2.2%.

If this trend continues, it will be harder for the ECB to justify a hike beyond July. It is important to note that we do expect EZ and UK inflation to suffer the same fate as in the US, just with a time lag. This time lag will decide for how long the EUR/USD and GBP/USD strength will continue.

DXY down over 2% in seven days

Table: 7-day currency trends and trading ranges

Key global risk events

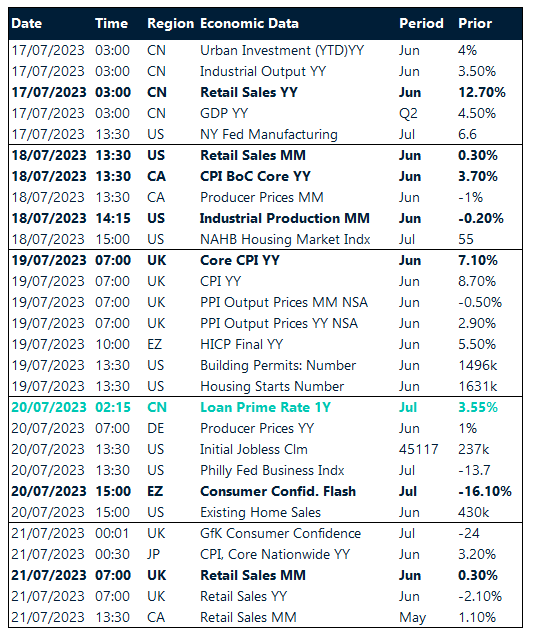

Calendar: July 17-21

Have a question? [email protected]

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.