Written by Convera’s Market Insights team

Dollar gains, but so do stocks, after hot US CPI

Boris Kovacevic – Global Macro Strategist

The US dollar index has risen for two days on the bounce, in line with US Treasury yields, which touched 1-week highs yesterday after a hot US CPI print sparked a modest hawkish repricing of Federal Reserve (Fed) policy expectations. However, stock markets brushed the news off, with the S&P500 and Nasdaq rising over 1% in a sign that investors were fearing a larger upside surprise.

Still, US inflation came in hotter than expected once again in February, confirming the increase in consumer prices from the month prior. The main surprise came from core inflation posting a second consecutive monthly print of 0.4%, putting the annual growth rate at 3.8%. While still down from the 3.9% posted in January, the fall of underlying inflation continues to lose momentum as shelter inflation remains stubbornly high at 5.7%. This will most likely confirm the Fed’s cautiousness to start the easing cycle before June, given that the 1- and 3-month annualised core inflation rates increased to twice the central bank’s target at 4.4% and 4.2%. Markets remained calm though despite the recent inflation surprises because the overarching theme of easier monetary policy ahead remains in place.

Flying under the radar, but arguably more important, was the NFIB survey of small businesses, which offered investors some relief as the compensation plans of companies – a leading indicator for wage growth and therefore inflation – ticked down to its lowest since the beginning of 2022 in February. While the Q1 reflation has dampened hopes of a March or May rate cut, June is still seen as the beginning of the easing cycle.

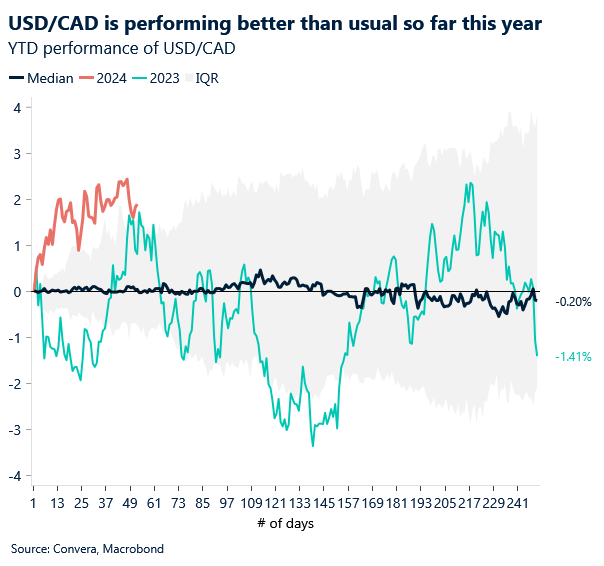

USD/CAD posts minor gains below 1.3500 barrier

Ruta Prieskienyte – FX Strategist

Pressure from a rising US dollar saw the Canadian dollar from a one-month high of $1.345 to trade around $1.3500 as of Wednesday morning. The stronger-than-expected US inflation number weighed on market sentiment and but did not change FOMC rate expectations. Thus, the initial spike in post-data FX volatility dissipated quickly.

Similarly to the G3 central banks, the Bank of Canada may not want to diverge too much from the Fed as it could weaken the Canadian dollar and result in higher import costs – a threat to the BoC’s own fight in taming inflation back to its 2% target. Canada is a major producer of commodities, including oil, so the loonie tends to be sensitive to the global economic outlook. WTI crude futures rose to around $79/barrel on Wednesday, on a strong outlook for global demand. In its monthly report, OPEC expect global oil demand to increase by 2.25 million bpd in 2024 and by 1.85 million bpd in 2025 while raising its economic growth forecast for the current year.

Despite the recent spike in oil futures, the Canadian dollar was not able to capitalise on it and depreciated for the fourth consecutive session against the US dollar. With today’s calendar empty, we expect USD/CAD to trade rangebound between $1.3470 – $1.3520.

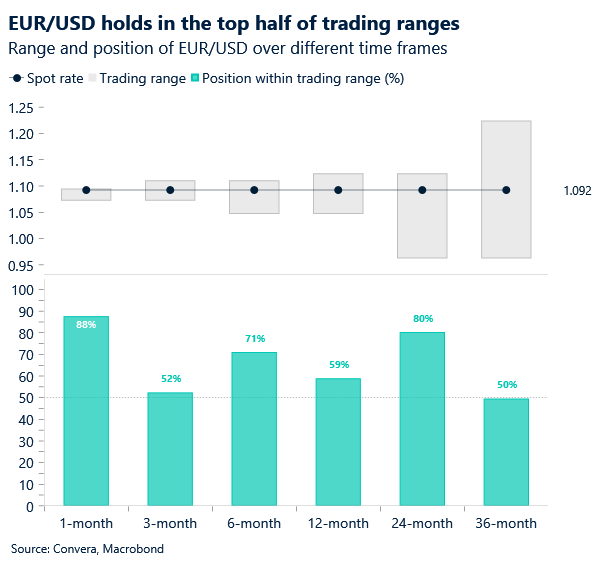

Euro puts up a good fight

Ruta Prieskienyte – FX Strategist

EUR/USD declined to the lower $1.0900s after the release of US CPI inflation showed inflationary pressures were higher than expected in February. The fact that gasoline and energy prices were two of the biggest contributors to elevated inflation limited EUR/USD decline, with the pair closing unchanged on the day at $1.0924.

A consensus appears to be emerging among Governing Council members on the timing of the ECB rate cuts with June emerging as the most likely contender to kickstart policy easing cycle, no earlier. In an interview yesterday, Robert Holzman – among the most hawkish rate setters – confirmed that a rate cut is more likely in June, than April, but does not remain a done deal. The policymaker cautioned that cutting interest rates before the Fed could cause an investor reaction and would be euro negative. While the ECB remains optimistic about the inflation progress thus far, “there are some residual doubt” about the convergence to 2% in 2025 as per latest ECB staff projections. The central bank has been misled by projections before, so staying data-dependent and open to acting when needed, but also not prematurely, remains the best course of action for now. As it stands, it seems June rate cuts are 1/1 for all G3 central banks, with probability of an ECB rate cut now at 83%.

Today’s calendar is looking light yet again, with speeches by two dovish European Central Bank members, the Executive Board’s Piero Cipollone and the Governing Council’s Yannis Stournaras, due later today. EZ Feb industrial production dropped the most in 10 months, but was largely ignored by the markets as suggested by EUR/USD overnight ATM option price. Expectations is for EUR/USD to be largely range bound $1.0870 – $1.0950.

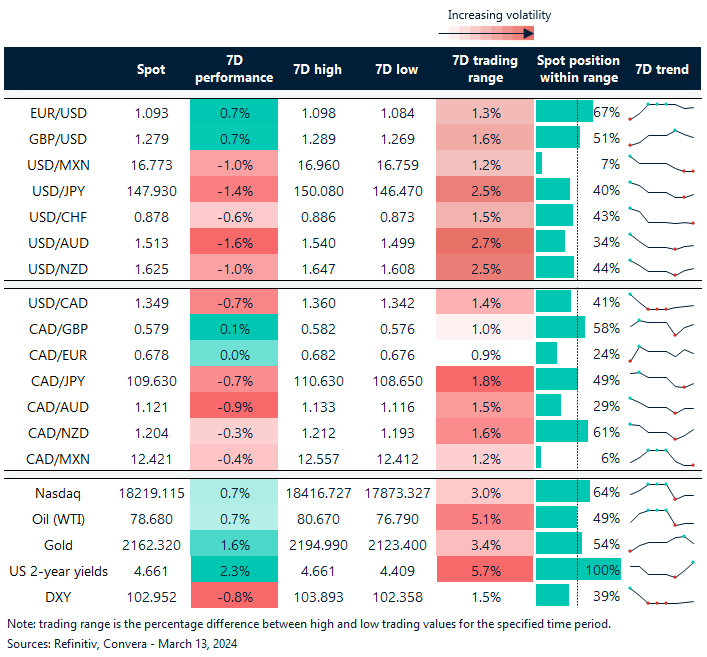

Global stocks up almost 2% since last week

Table: 7-day currency trends and trading ranges

Key global risk events

Calendar: March 11-15

Have a question? [email protected]

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.

Join us for Convera Live! A series of in-person events discussing the future of global payments.