Tariff tensions rise again

After a tumultuous first half, the three pillars of Trumponomics, fiscal stimulus, deregulation, and trade, are finally beginning to take shape. With the fiscal bill now signed and deregulatory discussions underway, investors are looking to the final piece of the puzzle: progress on tariffs. Hopes for clarity on this front are high heading into the week.

But the market’s reaction to the latest trade developments has been far from upbeat. Investors were caught off guard by news that the U.S. will impose a 25% tariff on imports from Japan and South Korea starting August 1. President Trump doubled down, warning that any retaliatory tariffs would trigger an additional 25% levy from the U.S. Given that Japan and South Korea are among America’s top seven trading partners, the unexpected escalation adds a fresh layer of uncertainty to the economic outlook for the second half of the year.

In parallel, the administration has issued additional letters detailing new tariff rates, effective August 1, for Malaysia, Kazakhstan, South Africa, Laos, and Myanmar. While there are some rate adjustments from the previous April 2 levels, Myanmar drops from 44% to 40%, Laos from 48% to 40%, and Kazakhstan from 27% to 25%, South Africa remains at 30% and Malaysia edges up to 25%, aligning with the rate for Japan.

Amid these revisions, the more significant development is the extension of the July 9 deadline to August 1. That provides three more weeks for negotiations and potentially more deals to be finalized. Notably, no such letters have been sent to Europe or Canada, a detail that hasn’t gone unnoticed by markets. But the impact was immediate: volatility, which had been hovering at 2025 lows, spiked. Major equity indexes pulled back close to 1%, and the dollar rallied roughly 0.3% on the news.

Taken together, this moment underscores just how complex U.S. trade policy has become. The Trump administration’s ambition to lock in a high volume of deals within 90 days now faces the reality of protracted negotiations. With the clock ticking toward August 1, the coming weeks could be a critical window for countries looking to get ahead of rising trade barriers.

CAD remains unchanged

Yesterday, after the tariff announcement the CAD lost 0.57% to reach 1.3684, its largest single-day percentage gain since June 17, 2025. The CAD has also lost for two consecutive sessions, with a cumulative loss of 0.74%, the weakest two-day performance since June 18, 2025. However, the USD/CAD is finding some resistance that’s bringing it below its 20-day moving average at 1.365. The USD/CAD is 5.9% below its 52-week high of 1.4535, recorded on January 31, 2025, and it’s still away almost 2% from its 52-week low of 1.3432, set on September 24, 2024.

Tariffs and tough talk: the Trump playbook in action

Amid yesterday’s flood of tariff-related headlines, the core takeaways are: Letters sent to trading partners outlined tariff levels that were nearly identical to those announced on Liberation Day. The July 9th implementation deadline was quietly pushed back to August 1st. Even that revised date feels flexible, with Trump suggesting it isn’t “100 percent firm.”

In short, the message is clear: Trump is open to further negotiations with countries offering additional concessions.

As markets worked to confirm that the latest announcements were simply part of Trump’s familiar strategy—tough rhetoric followed by openness to negotiation—certain currencies came under pressure. Asian currencies, particularly those of Japan and South Korea, along with commodity-linked currencies like the Antipodes and the Canadian dollar, fell as high as 1 percent. However, they rebounded during the overnight Asian session, regaining ground as sentiment shifted and investors reassessed the likelihood of constructive trade talks.

What these underperformers have in common is stalled trade talks with the U.S. and limited signs of progress.

Meanwhile, the U.S. dollar led the pack, with the dollar index (DXY) rising 0.5 percent—marking its strongest single-day gain since the safe-haven spike in mid-June.

As for the euro, EUR/USD briefly dropped nearly 0.6 percent but recovered as the European Union maintained a strong negotiating position. The EU is working to finalize a preliminary trade deal with the U.S. this week, aiming to secure a 10 percent tariff rate before the August 1 deadline.

Looking ahead, the focus turns to updates on the EU–U.S. trade deal. If talks prove more difficult than expected, EUR/USD may drift lower, finding support around $1.1700.

Fiscal fears tarnish USD and GBP

After surging to fresh 44-month highs near $1.3800, GBP/USD reversed course sharply, dipping below $1.36 yesterday. The retreat followed a renewed dollar rally ahead of the July 9th deadline, and fresh budget jitters weighing on the Pound.

Fiscal policy is emerging as a key pressure point for both currencies, with bond markets in the UK and U.S. becoming increasingly uneasy about medium-term fiscal credibility. Washington must grapple with a $3.4 trillion deficit blowout from its tax overhaul, while the UK faces tightening fiscal rules—especially after last week’s dramatic U-turn on Keir Starmer’s welfare plan, which came with a £5 billion price tag.

Yet, the dollar has one powerful advantage: a robust, steady stream of tariff revenue. Regardless of where the final average tariff level lands, and chronic uncertainty still mounting, proceeds will most certainly remain well above pre-2025 norms. Between now and 2034, tariff collections are projected to total $2.3 trillion—even after adjusting for weaker trade flows and a pivot toward lower-tariffed goods and partners.

Ironically, this fiscal boost gives the greenback a firmer footing than sterling in the credibility stakes, suggesting that economic resilience may come more from trade policy than political rhetoric—at least for now.

JPY stands out as underperformer

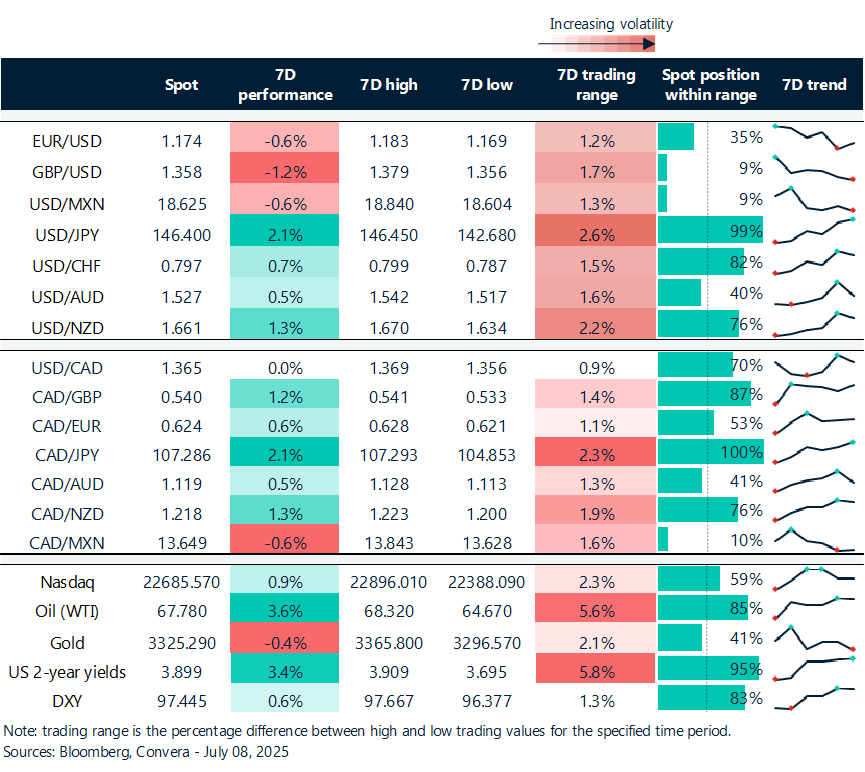

Table: 7-day currency trends and trading ranges

Key global risk events

Calendar: July 7-11

All times are in ET

Have a question? [email protected]

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.