Global overview

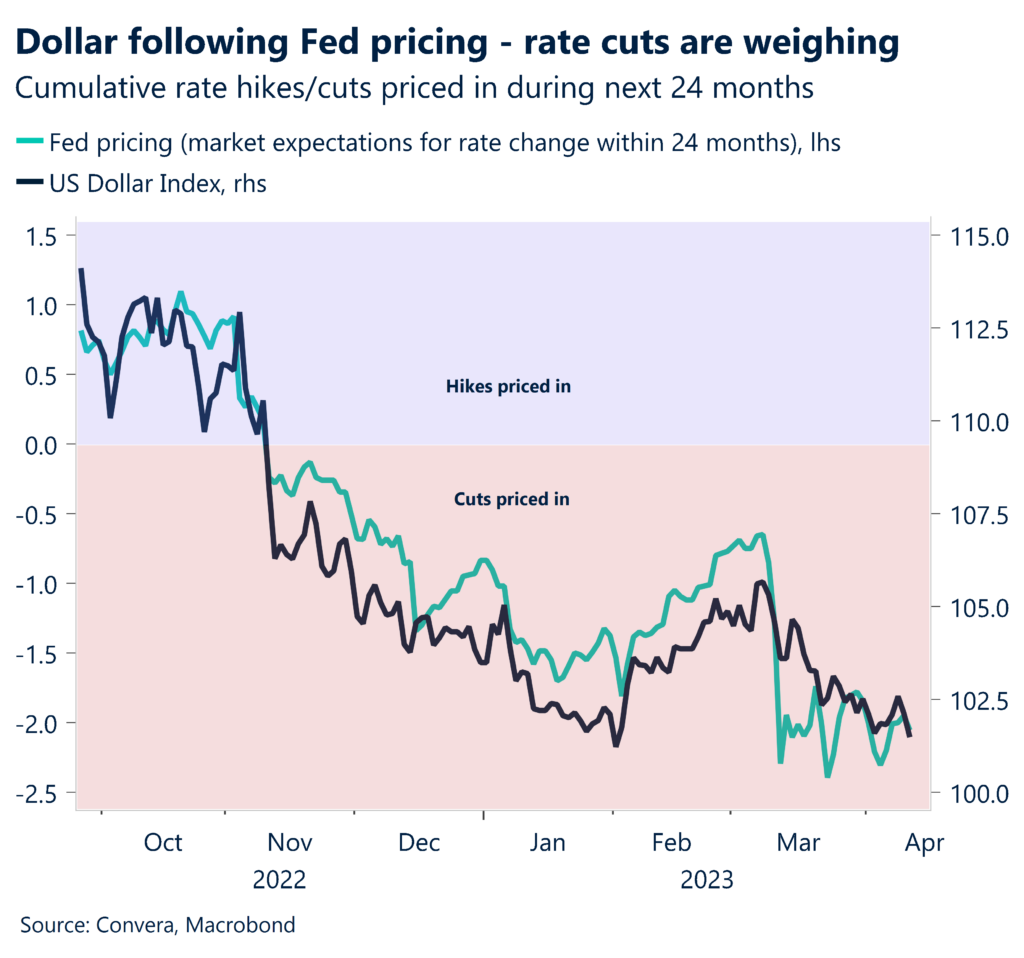

The U.S. dollar’s slide gathered pace as it tumbled to precarious levels versus its European counterparts. The buck fell to multimonth lows against the euro and sterling and hit an eight-week bottom versus the Canadian dollar. A trio of factors have conspired to weigh on the greenback such as moderating U.S. inflation, a Fed seen closer to ending its rate hiking campaign, along with faltering confidence in America’s economic outlook. The Fed is yet to slay the inflation dragon but consumer prices cooling to the lowest level (5%) in nearly two years eased pressure on the central bank to push lending rates materially higher from present levels just below 5%. Meanwhile, the minutes from the Fed’s March meeting showed that staff forecasts now anticipate a recession by year-end. With the Fed acknowledging the likelihood of recession, loosely viewed as back-to-back quarters of negative growth, it’s bolstered expectations that the central bank may have to cut rates later this year. The Fed’s data-dependent policy outlook will put emphasis on indicators today on wholesale inflation and weekly jobless claims, followed by retail sales Friday.

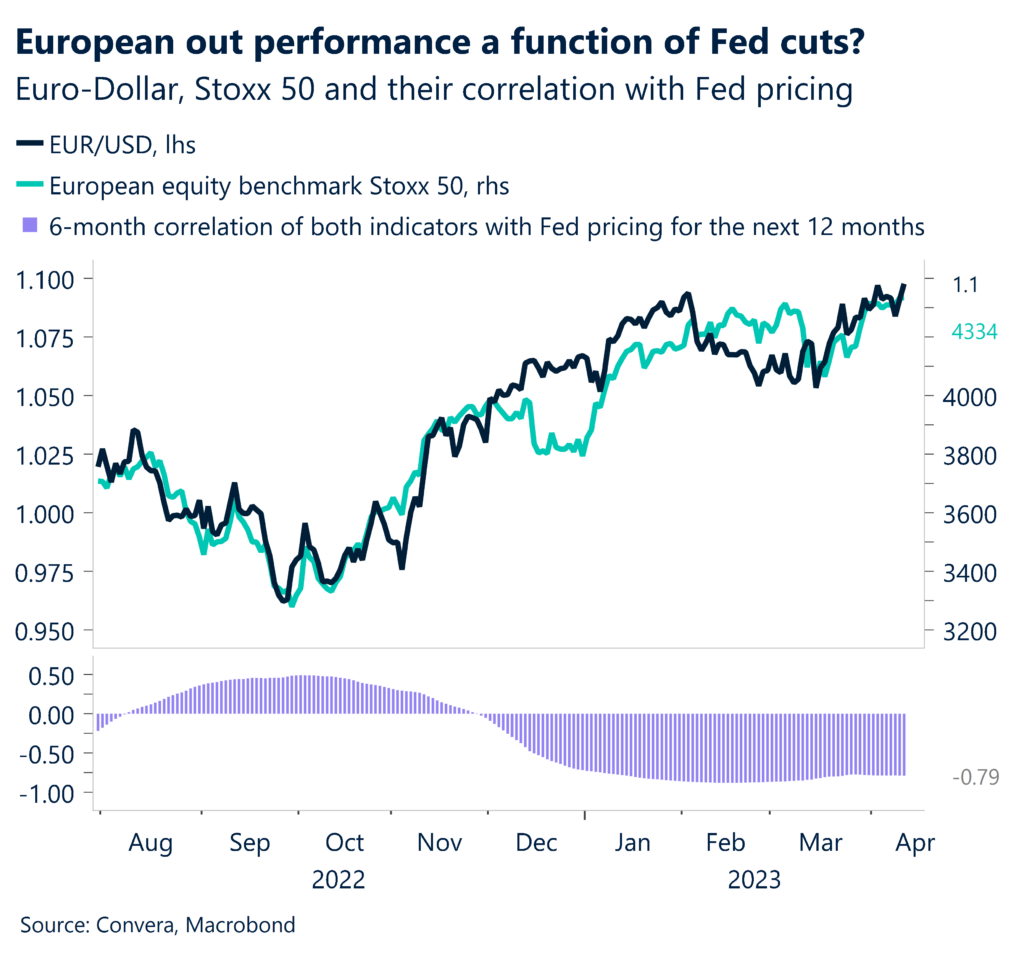

Euro flirts with 2023 highs

The euro popped to 10-week highs against its weaker U.S. rival as economic developments on the left side of the Atlantic cast doubt on the Fed pursuing higher interest rates for longer. U.S. inflation remains high but its steady descent from multidecade peaks points to a central bank in the late innings of its rate tightening cycle. The ECB, meanwhile, appears to have further rate hiking to go, given more elevated inflation in Europe. The euro’s latest surge moved it closer to highs for the year that it clocked in early February.

Sterling notches a mid-2022 top

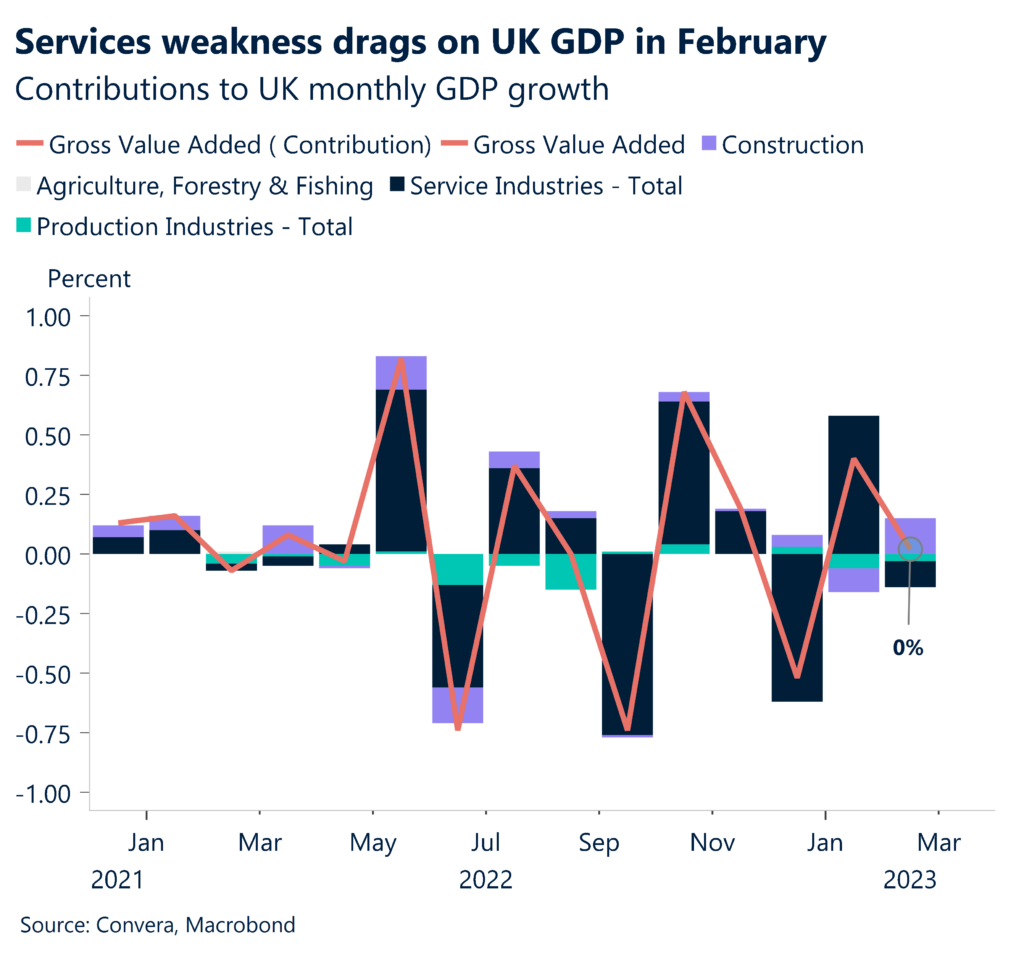

A weaker U.S. dollar and signs of a resilient UK economy proved a recipe for sterling outperformance as the British unit strengthened to fresh 10-month peaks. The UK economy unexpectedly flatlined in February with zero growth versus forecasts of a mild expansion. The pound sidestepped the data as it helped that growth for January enjoyed an upgrade. On balance, today’s data suggested fading prospects for the UK economy to slip into recession. Growth, though, is still expected to remain anemic over the balance of the year, a factor that can limit scope for Bank of England rate increases.

C$ soars to 8-week peaks

Canada’s dollar rolled to eight-week highs a day after the Bank of Canada kept interest rates steady and set a high bar for rate cuts later this year. Ottawa also didn’t rule out more rate increases from 4.5%, if inflation doesn’t moderate to roughly 3% by the summer from 5.2% at present, the lowest level in more than a year. Moreover, the sputtering greenback and oil’s climb to 2023 peaks further above $80 helped to put a stronger tailwind on the loonie.

Weaker data, weaker dollar

New signs of a slowing U.S. economy pushed the dollar lower and the euro higher with the latter scaling one-year peaks. America’s job market showed signs of moderating as weekly jobless claims climbed more than expected to 239,000 in the latest period from 228,000 the week before. Wholesale inflation cooled to an annual rate of 2.7% in March, a sharp slide from 4.9% in February. The extent of the slowdown in both consumer and producer inflation this week, coupled with mounting signs of a slowing U.S. economy, suggests it’s not out of the question for the Fed to hit the pause button further rate hikes as soon as May which is bad for the dollar.

Dollar slides to precarious levels above 1.10 vs EUR and 1.25 vs GBP

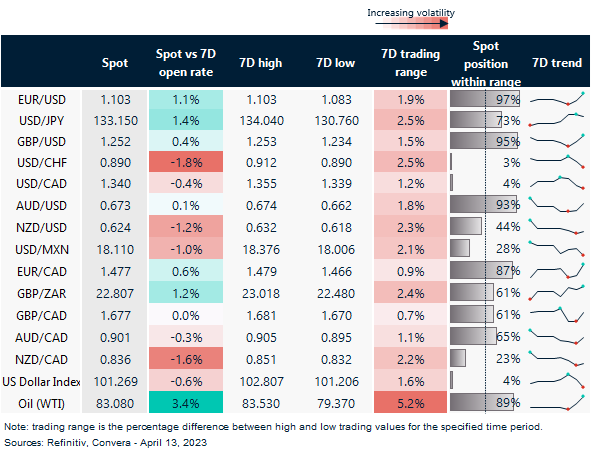

Table: rolling 7-day currency trends and trading ranges

Key global risk events

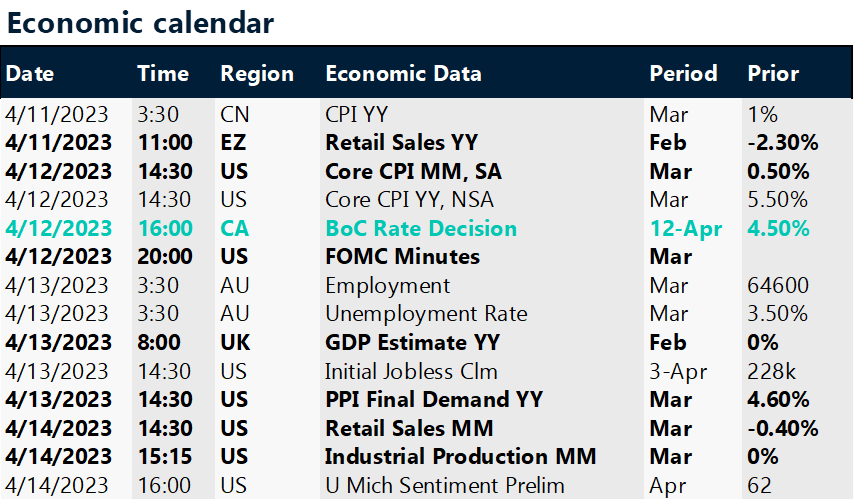

Calendar: Apr 10-14

Have a question? [email protected]

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.