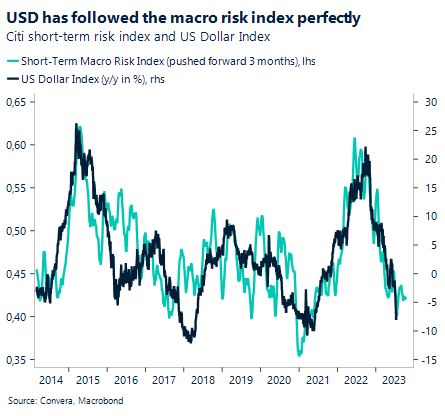

Disinflation trumps resilient macro data

Last week was shaped by global risk assets profiting from the lower-than-expected US inflation print and reduced expectations of a Fed hike after the July meeting. However, the wave of optimism has subdued somewhat since the start of this week. Investors appear cautious ahead of the release of US retail sales, industrial production and crucial housing data starting from today with the dollar finding a temporary bottom after suffering its worst week this year.

Secondary data points offered the US currency some support with both the Michigan Consumer Sentiment Index (Friday) and New York Fed Manufacturing Index recovering more than economists had anticipated in the previous month. The currency’s sensitivity to macro data has somewhat weakened given the strong disinflationary forces starting to build. Consumer, producer, import and wholesale inflation all weakened in June, showing how both the supply and demand side are normalizing.

Nonetheless, the US economy has held up surprisingly well so far and the labor market continues to add people every single month. This conundrum will be the main concern of policymakers when they meet in July, where markets price in a rate hike by 25 basis points with a 97% probability. The chance of another increase, as forecasted by the Fed’s dot plot, has eroded to just 21%. The US dollar index is currently trading just below the 100 mark at the lowest level since April 2022.

ECB: Doves in a hawk’s costume

The European economic outlook is closely tied to developments in China, given the close trade relationship between the two regions. It is therefore even more surprising how the euro has held up its gains against major currencies while the second and third largest economies in the world are facing economic headwinds.

The International Monetary Fund currently expects Germany to shrink slightly this year, with momentum only gradually recovering in the following two years. This assessment was echoed by the German Bundesbank, which expects GDP growth to be weaker in the second half of the year than previously implied by its June forecasts. Worries over China’s sluggish reopening at the beginning of this year have mounted as well, with most macro data coming in weaker than expected. Yesterday’s data for the month of June left investors with a mixed feeling. While industrial production did surprise positively (4.4% vs. 2.7% expected), both retail sales and GDP growth surprised to the downside with growth rates of 3.1% (vs. 3.2 exp.) and 6.3% (vs. 7.3% exp.).

Weaker Chinese macro data put Asian equities under pressure over night, but it seems that European stocks might be poised for a slightly higher open today. Meanwhile, EUR/USD is hovering near its 16-month high at $1.1250. The common currency has been less affected by recent comments from ECB policymakers cautioning markets about taking a rate hike beyond July as given. The presidents of the German and Italian central banks have said that the September meeting remains an open one, which will be decided by incoming data. Ignazio Visco went as far as to suggest that inflation could even fall more than the current forecasts suggests. This puts a lot of weight on the European macro data, which will matter more next week. The next trading session will be US focused.

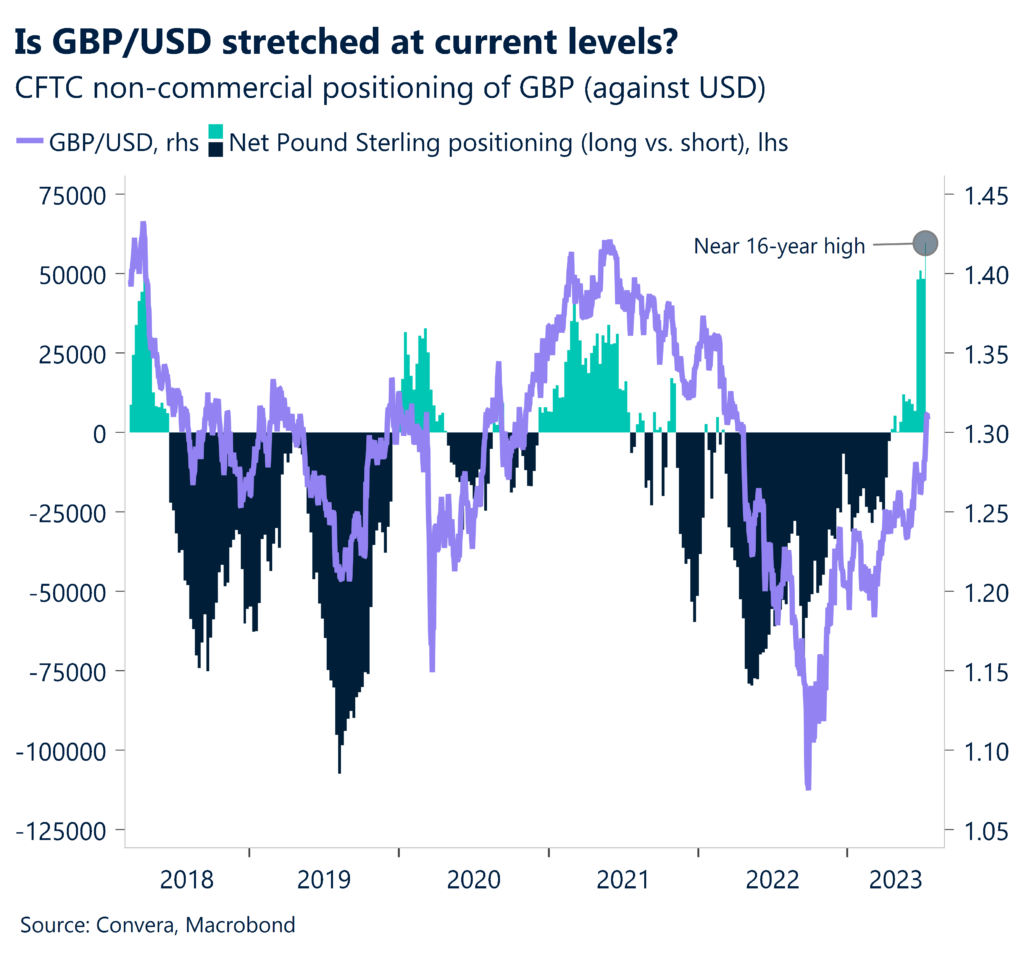

Could a softer UK inflation print support sterling?

Large upside surprises for services inflation and private sector regular pay growth – two data points identified as key by the Bank of England (BoE) – resulted in financial markets aggressively repricing UK interest rate expectations higher in the weeks before the central bank’s last meeting in June and sent sterling surging across the board. We’ve seen UK pay growth remain elevated since, but what impact might tomorrow’s inflation report have on the pound?

The upward repricing of UK interest rate expectations likely pressured the BoE to increase the pace of rate hikes, with a 50-basis point increase in Bank Rate to 5% last month, accompanied by hawkish rhetoric. Money markets are currently pricing a 70% probability of another jumbo hike next month and for rates to peak around 6.25% early next year. In theory, the pound should react positively to this interest rate rise speculation so long as the UK economy continues to be resilient. But, if data suggests the risks of a recession are growing, sterling may lose its shine despite widening rate and yield differentials. Although some might argue an inflation print that exceeds expectations tomorrow will offer support to sterling, based on a likely rise in nominal gilt yields, it could also be argued that a softer inflation print might help the pound. This is because 1. It boosts the UK economic outlook and chances of a so-called soft landing and 2. Falling inflation will boost UK real yields.

As is often the case these days, macro data is proving challenging to forecast and the reaction in financial markets can often catch market participants off guard. Hence, we should take heed of the pound’s current positioning. GBP/USD is almost 2% above its 5-year average rate of $1.2870 and is 8% above its 1-year average. The currency pair is still in overbought territory according to several momentum indicators, and CFTC data showed the latest net GBP long position rose to its highest since November 2007, indicating a potentially overcrowded bet on the pound appreciating further from here.

Global stocks up 3% amid improved sentiment

Table: 7-day currency trends and trading ranges

Key global risk events

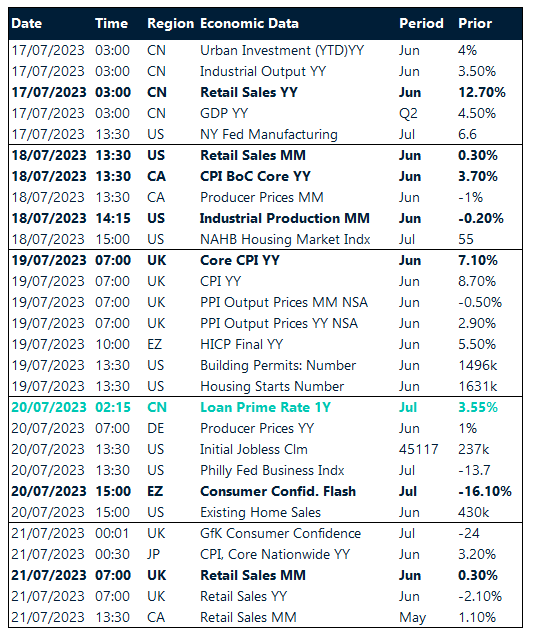

Calendar: July 17-21

Have a question? [email protected]

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.