Written by Convera’s Market Insights team

Retail sales continue streak of strong data

Boris Kovacevic – Global Macro Strategist

The US economy keeps on giving and investors keep on pricing out policy easing from the Federal Reserve. That has been the story of the past few weeks, which has culminated in markets now expecting less than two rate cuts this year. Yesterday’s stronger than expected retail sales (+0,7 m/m) for March lined up with the upside surprises of both the jobs report and latest inflation print, suggesting that economic momentum remained solid all throughout the first quarter.

Treasury yields on the long end have risen to their highest level since November, dampening risk appetite and putting the S&P 500 on track for its third consecutive weekly decline. At the same time, the global commodity index has risen by 11% so far this year. Taken together, this has created a perfect environment for the Greenback to shine, as its benefiting from its position as a high yielding, high growth, commodity backed safe haven currency. As central banks outside the United States continue to lay the groundwork for rate cuts, policy divergence and momentum will favor the reserve currency. The US Dollar Index appreciated for a fourth consecutive day, extending its year-to date gain to 4.7%.

However, it will be interesting to see how much of this shift has already been reflected in markets and how much more rate cuts can be priced out for the Federal Reserve. This is hard to answer right now due to the current push (global inflation impulse rising) and pull (weakening leading economic indicators) effects influencing the dollar and Fed pricing. Geopolitical developments relating to the conflict in the Middle East add to the uncertainty surrounding the future policy path of central banks and the inflation trajectory. However, so far, markets seem to have taken the escalation by Iran with stride as Western forces race to avert a full blown retaliation from Israel.

Sterling plunges to a 6-month low on jobs data

Ruta Prieskienyte – FX Strategist

The British Pound is struggling to climb out of the hole it fell into end of last week and continues to slide against the US dollar. GBP/USD finally broke out of the 4-month range and extended the drop into the $1.2400 handle, a 6-month low, as the employment report missed expectations with an uptick in the unemployment rate and an easing in wage growth.

The February labour market report showed the UK unemployment rate rising to the highest level since August 2023, up to 4.2% and exceeding the market consensus. The labour market slackening was driven by an increase in long term unemployment, a decrease in part-time employment as well as a rise in the economic inactivity rate. Meanwhile, the BoE’s closely watched pay growth metric went up to 6% y/y – the slowest pace since September 2022. Adjusted for inflation, wage growth in real terms was unchanged at 1.9%. The BoE meets on May 9th and is expected to hold rates for a fifth straight time, but the central bank remains divided about the rate policy. Governor Bailey has said that rate cut expectations this year are “not unreasonable”, but Monetary Policy Committee members Megan Greene and Jonathan Haskel have said that rate cuts should be a long way off. For now,

Looking ahead, the CPI report due tomorrow will prove important for gauging the timing and extent of Bank of England interest-rate cuts. The markets appear to have concluded that a string of hotter-than-expected CPI prints in the US will limit the Bank of England’s ability to cut rates this year to just over 50bps, but a change of heart and indication of intent to decouple from Fed could see the Sterling weaken in the short term. Over the immediate term, GBP/USD technicals are bearish, with $1.2500 seemingly out of reach.

Euro fails to recover despite industrial output rebound

Ruta Prieskienyte – FX Strategist

The euro continues to struggle to find its footing, falling to a fresh 6-month low and below the $1.0620, and over 1% below Friday’s peak of $1.0732.. With the ECB April monetary policy meeting and US inflation updates in the rear-view mirror, attention this week turns to relative economic performance and how it is being interpreted by central bankers.

The latest report revealed that industrial production in the Eurozone rebounded by 0.8% m/m in February, marking a partial recovery from a revised 3.0% downturn in January. On a yearly basis, industrial production contracted by 6.4% in February, extending the 6.6% contraction observed in the previous month. Outside of data, over the past few days we have received further validation of impeding policy divergence between the Fed and the ECB. ECB’s Stournaras and Simkus show openness to cut 3, potentially even 4, times by year end, despite Lagarde’s unwillingness to commit to a specific policy path during the conference last Thursday. Overall, the sentiment across the Governing Council is growing increasingly more dovish. Swaps are currently pricing an almost sure thing of a June cut, with probability rising to 89% and expect 82bps cumulative rate cuts by year-end.

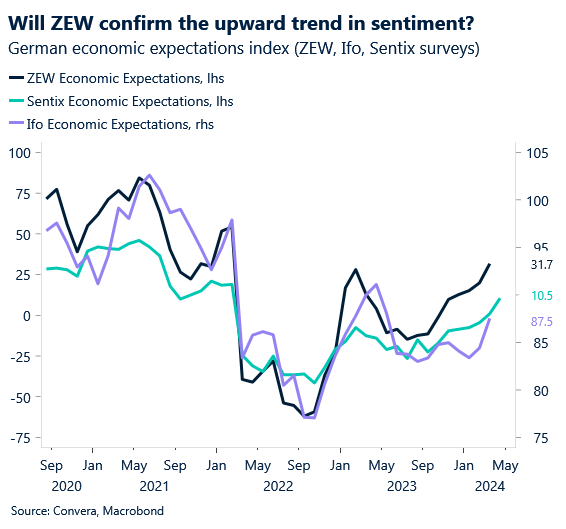

Today, investors will eye the ZEW Economic Sentiment for further confirmation that investor appetite is improving across the bloc. As overnight EUR/USD ATM implied option vols are above long-term average levels, we anticipate the print to have a sizable impact. Market consensus is expecting the largest improvement in sentiment across both Germany and Eurozone, and a such a confirmation would be euro supportive. However, the net gain may be negligible as the downside pressure remains high and the US dollar is still bullish.

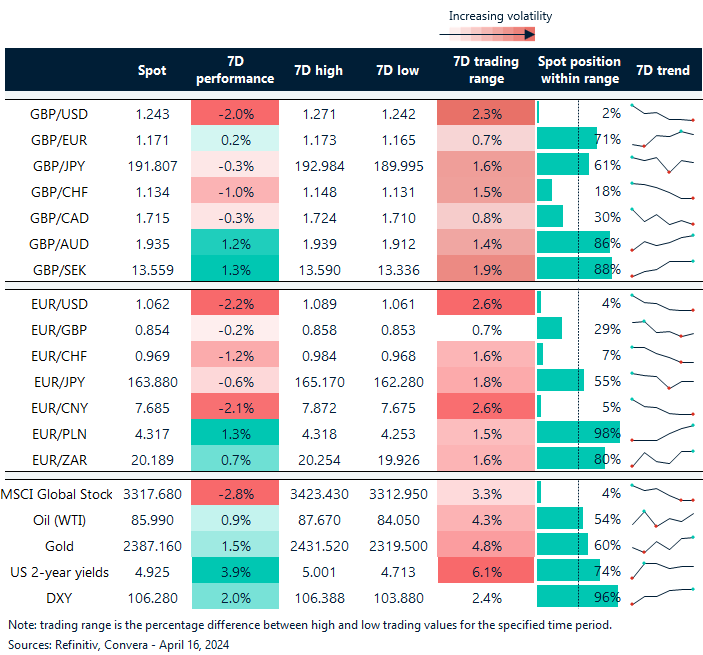

GBP and EUR extend 1-week losses to over 2%

Table: 7-day currency trends and trading ranges

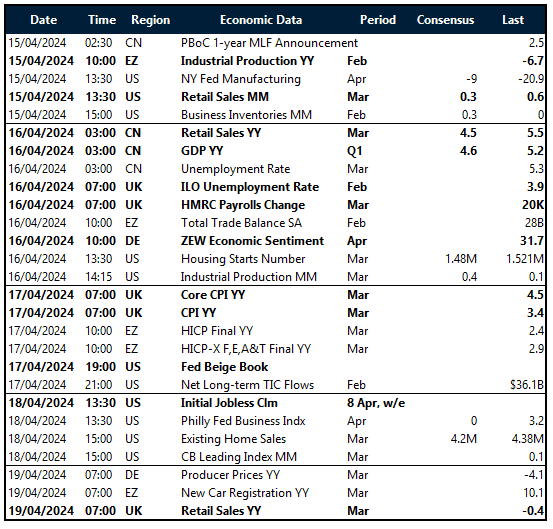

Key global risk events

Calendar: April 15-19

Have a question? [email protected]

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.