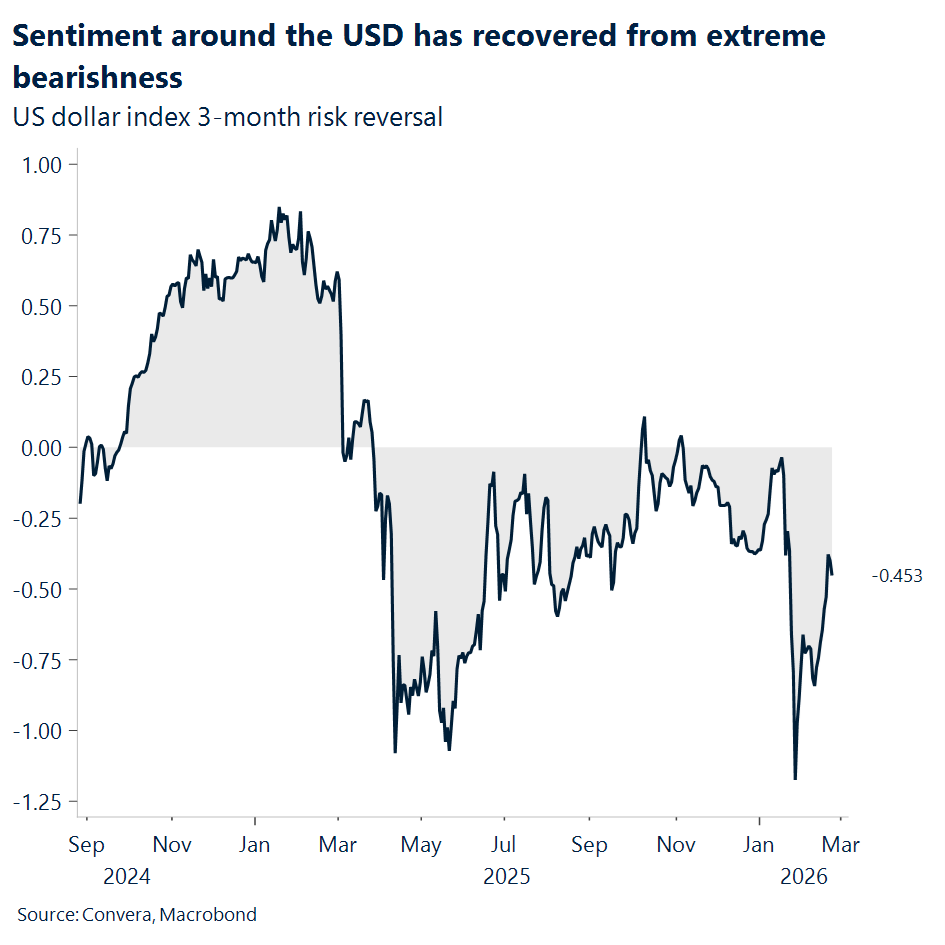

USD: Finding balance in a shifting market

The US dollar Index has seen some notable swings lately as it navigates a tug of war between prospects of decent growth and sticky inflation and shifting trade policies. While the index recently touched 98.1 before settling back near 97.7, it remains resilient despite a spike in market volatility. This stability comes as the administration pivots from the now struck down IEEPA tariffs to new 15% levies under Section 122. Although these new measures act as a momentarily bridge, the shift has brought back trade policy uncertainty. While the effective tariff rate is currently close to where it stood last week, the lack of long-term clarity on future trade barriers continues to weigh on the broader dollar narrative.

On the monetary side, recent data shows that price pressures remain stubborn with core inflation sitting at 3%. This has prompted a more cautious tone from the Federal Reserve, as officials seem increasingly wary of cutting interest rates too quickly. Such a hawkish stance usually provides a solid floor for the currency, even as we digest the news that tariff refunds likely will not provide an immediate economic boost. History suggests that these types of refunds can take years to process, meaning they are unlikely to change the 2026 tax revenue outlook. Even so, the recent court rulings have reduced the risk of sudden and dramatic tariff shifts, as the President can no longer use a magic tariff pen to threaten partners on a whim, which offers some structural relief for global markets.

Geopolitical tensions are also keeping the fear index elevated above 20 as markets watch developments between the US and Iran. With the US deploying significant resources to the region, oil prices recently reached a new high for the year. This situation creates a delicate balance for a presidency that campaigned on avoiding new conflicts while still maintaining a strong international presence. Most analysts expect this to result in limited actions rather than a major escalation that could hurt financial markets ahead of the midterms. For now, the focus remains on whether these tensions will lead to a new deal or continue to simmer as a source of market nervousness.

Despite the flurry of headlines, the broader equity market is finishing another healthy quarter of earnings with nearly 80% of companies beating expectations. It is encouraging for most market participants that growth is becoming more diversified, with energy and consumer staples leading the charge rather than just a few massive tech firms. This shift away from overdependence on a handful of names is a positive sign for the long-term health of the S&P 500.

Today, President Trump delivers the State of the Union address, where he’s expected to discuss policy priorities like tariffs and affordability ahead of the November midterms. Markets will pay special attention to Nvidia earnings (Wed) and the Apple annual general meeting (Tue) while US data releases cover consumer confidence (Tue), and producer price index (Fri). It’s a busy week that balances political rhetoric with major corporate updates and a heavy Fedspeak speaking schedule. Global focus shifts to inflation readings from Australia (Wed), Tokyo (Fri), and regional Europe (Fri) to gauge broader price trends. Central bank events include interest rate decisions in Hungary (Tue) and South Korea (Thu). The busy calendar concludes with GDP figures from India (Fri), and Canada (Fri).

EUR: Technicals turn heavy

The euro has slipped back below the $1.18 handle this morning, continuing to hover around its 50‑day moving average, which is acting as the key near‑term support. With EUR/USD now trading beneath its 21‑day moving average — which has rolled over decisively — it’s starting to look as though short‑term momentum is tilting lower and the pair is preparing for a deeper test of support. The 100‑day moving average, sitting just below $1.17, now looks like the next gravitational pull for the pair — a level that could easily act as a magnet if downside pressure persists.

However, the challenge for the dollar is that uncertainty is creeping higher again, reinforcing the point that policy risk remains its biggest headwind. The currency is being pulled in two directions: a resilient US economy and fading expectations of near‑term Fed cuts are supportive, yet a growing list of policy‑related concerns is tugging it lower. And the euro typically benefits when the dollar comes under pressure, with anti‑dollar flows providing an additional tailwind for the single currency.

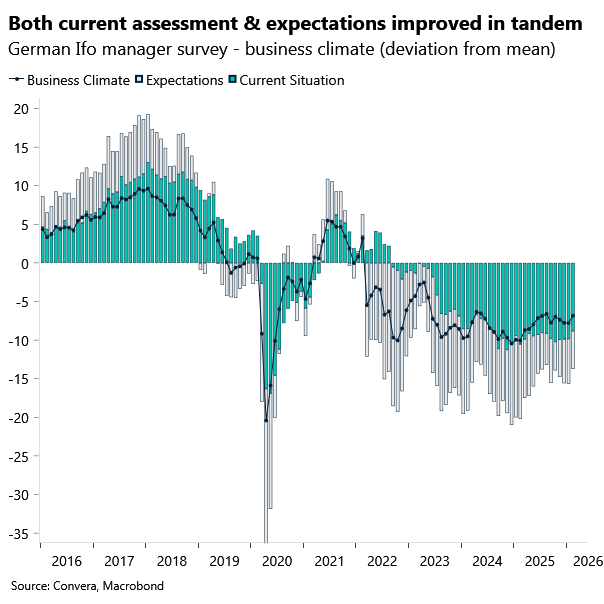

On the macro side, the question now is whether Germany is finally entering the long‑awaited cyclical upswing. The Ifo index jumped to 88.6 in February from 87.6 in January — its strongest reading since last summer. Both the current‑assessment and expectations components improved in tandem, signalling that sentiment is firming across the board.

January’s survey was likely still clouded by the Greenland conflict, but this month’s release comes before German firms have had a chance to fully digest the latest tariff uncertainty. Even so, the message is clear: the upswing is being driven by fiscal support, particularly in defence and infrastructure, and is now showing up in improving order books and falling inventories. If this momentum continues, it could offer the euro a degree of structural support by helping stabilise Germany’s industrial base and easing concerns that Europe is stuck in a low‑growth rut.

GBP: Tactically weaker, structurally exposed

The pound has slipped steadily through February as markets leaned into the idea of BoE rate cuts in March and later in the year. Even last week’s upbeat flash PMIs — a clear sign that underlying momentum is improving — failed to shift the dial. Sterling has been trading to the rhythm of global risk sentiment instead, with trade uncertainty and geopolitical tensions doing far more to shape price action than domestic data.

On the crosses, the technical picture has softened. The 100‑day moving average near €1.1456, which had been a dependable floor since January, has now flipped into resistance. GBP/EUR has failed to close above it for four straight sessions — a sign that the path of least resistance is turning lower. A move toward €1.14 looks plausible this week, with November’s €1.1320 lows coming back into view if downside momentum builds.

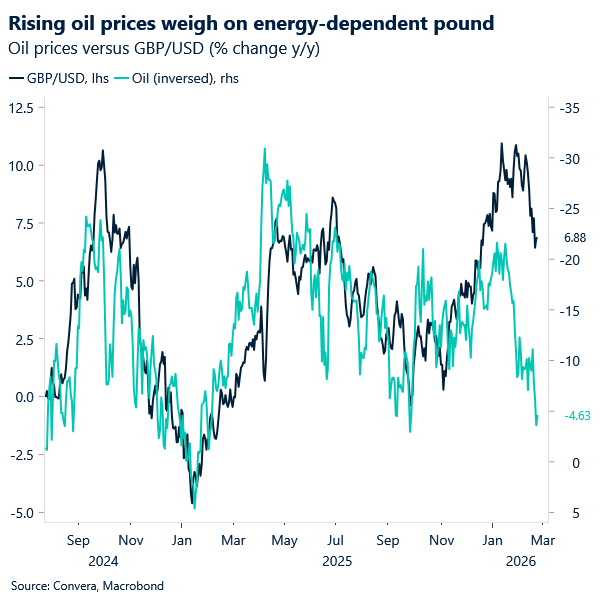

Meanwhile, a firmer dollar and higher oil prices dragged GBP/USD down to $1.3433 last week, erasing the year’s gains and raising the risk of a deeper correction. That level sits directly on the rising 200‑day moving average — a support zone that held repeatedly through late 2025 and early 2026 and remains central to the broader bullish structure. For now, that longer‑term uptrend is still intact, helped by the recent setback to Trump’s tariff plans, which has taken some of the shine off the dollar. GBP/USD is back near $1.35 this morning — almost exactly in line with its 10‑year average.

Politics now moves to the foreground. Thursday’s Gorton and Denton by‑election is shaping up as another moment of vulnerability for Prime Minister Keir Starmer, who faces mounting internal pressure. A loss in what has historically been a safe Labour seat would intensify questions over his leadership and raise the probability of a shift toward a potentially less market‑friendly configuration in the months ahead — a risk that remains under‑priced in sterling.

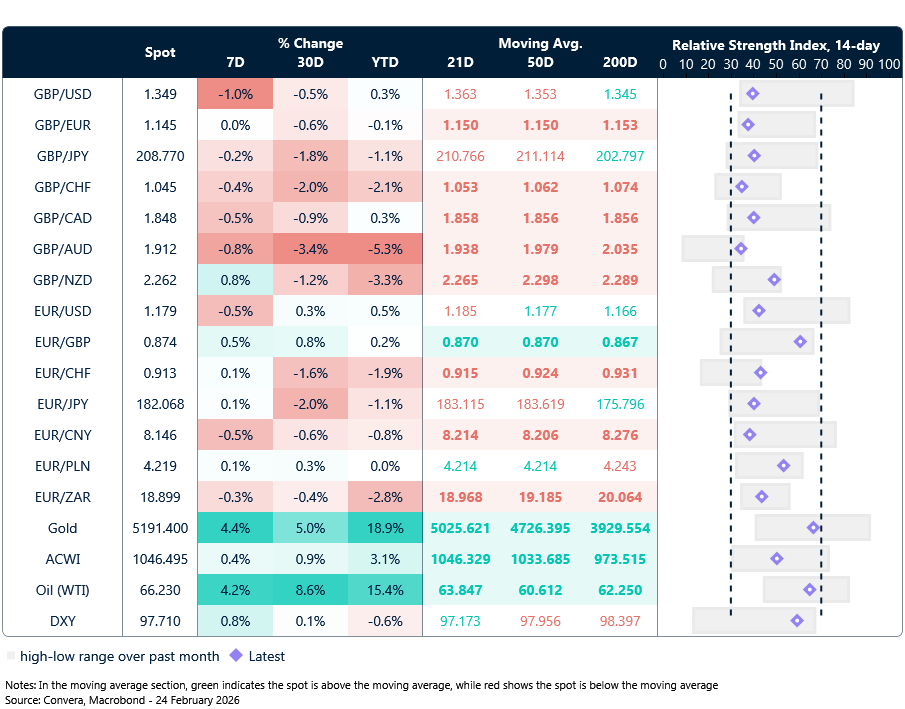

Market snapshot

Table: Currency trends, trading ranges & technical indicators

Key global risk events

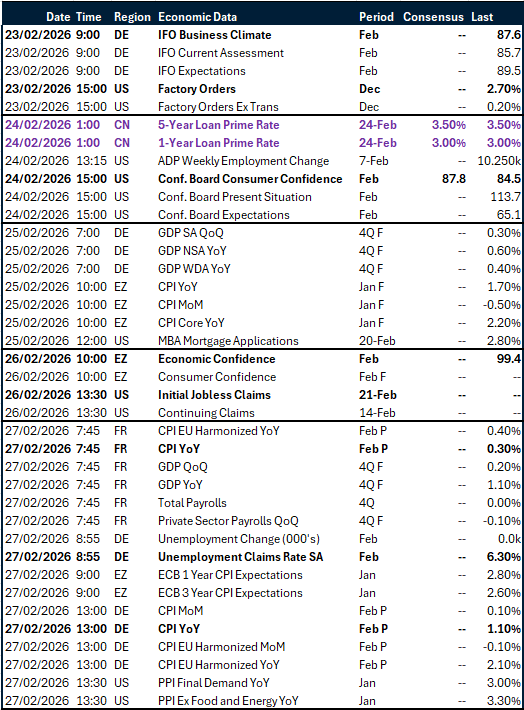

Calendar: February 23-27

All times are in GMT

Have a question? [email protected]

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.