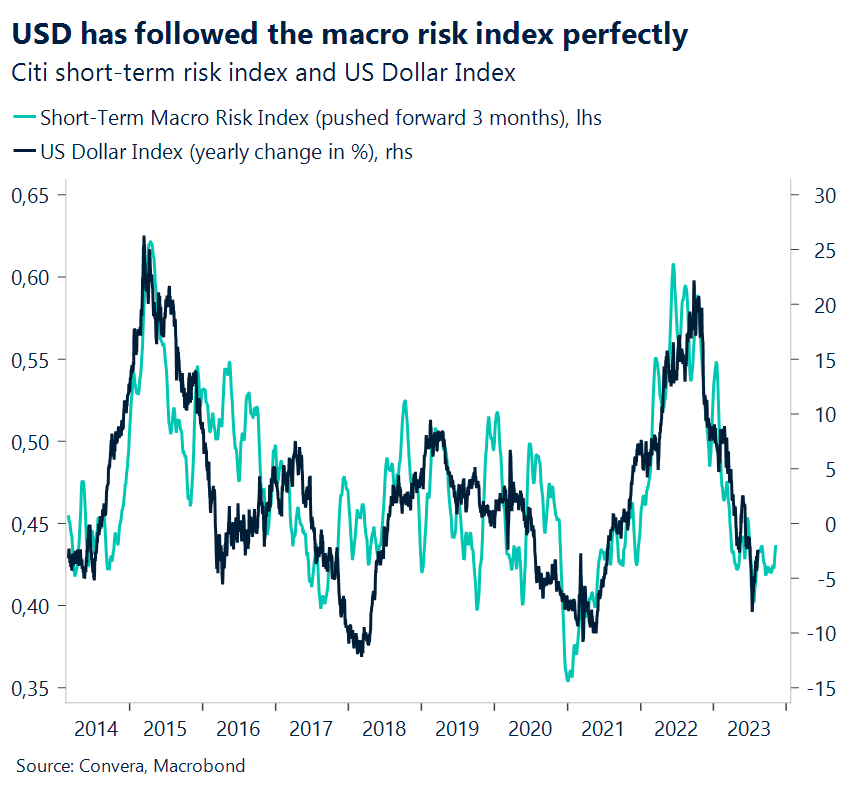

It’s all about the dollar but gains still limited

Last week has been a testament to the fact that inflation continues to be on top of investors’ minds. While the pace of consumer price growth has clearly slowed in the developed world, fears about inflation not returning to the 2% target in some countries have clearly spooked markets. The US dollar and longer-dated yields have now risen four weeks in a row with stocks trading broadly lower for a second consecutive week.

The latest print to evoke fears of inflation rebounding was the US Producer Price Index published on Friday. Factory prices beat expectations and rose 0.3% in the month of July, the second highest month-on-month increase so far this year. Services prices picked up by 0.5%, driving overall prices higher. Markets will continue to gauge where the US economy is headed with retail sales, industrial production and the FOMC minutes coming up this week.

The dollar has benefited from the combination of the risk off sentiment coming from weak economic data out of the Eurozone and China and higher domestic interest rates and is enjoying its position as a 1. safe-haven and 2. high-yielding currency. However, even with the gloomy European outlook, the advance of the dollar has been limited, suggesting that investors could see the current bout of strength as events driven and not enough to compensate for the overvaluation of the global currency.

China is limiting the euro’s potential

Europe has not been unaffected by reigniting inflation fears. However, in contrast to the US, where a strong economy is pushing up inflation expectations, the old continent is once again fearing the impact of high energy prices causing turmoil. Natural gas prices jumped by over 30% in a day at one point last week, caused by strike threats in Australia. Energy prices remain well below their pandemic highs, but European inflation expectations recently hit their highest level in 13 years.

This is why investors have not fully given up bets that the ECB will continue to raise interest rates despite the Eurozone’s sluggish demand and gloomy economic outlook. Markets currently price in a 40-percent probability of a rate hike in September. At the same time, expectations of rate cuts worth around 60 basis points have started building for next year. This has primarily been a function of the cyclical downtrend of the global economy with China and Europe at the centre of it. Chinese loan growth, published just before the weekend, fell more than expected to the lowest level since November 2009. The print is the latest data patch showing just how much China has disappointed investors hoping for a quick rebound this year.

The euro has noticed the slowing momentum from one of the Eurozone’s most important trading partners and while EUR/USD is still trading around 13% above its 20-year low reached in October, the upside seems to be limited in the short-term. As we noticed some weeks ago, there is only so much upside the euro can get from the US disinflation story without global economic growth picking up. EUR/USD is trading around $1.09 and is going into the week with a slightly negative bias.

Pound mixed before UK wage and inflation data

Tainted global risk sentiment after amid more disappointing Chinese data has weighed on risky assets including the pound against safe haven currencies this morning. GBP/USD has drifted back into the $1.26 region following a fourth weekly drop on the trot. Attention turns to key UK labour market and inflation data on Tuesday and Wednesday respectively, and the impact they will have on Bank of England (BoE) interest rate expectations.

Inflation data for June was more encouraging than expected, with headline inflation dropping to 7.9%. Another dip is expected, but the BoE has made it clear that it’s primarily focussed on services inflation and wage data to judge how many further rate hikes are needed. A September pause is unlikely and money markets are pricing an 80% chance of another 25-basis point rate hike, but policy decisions hinge on incoming data. Although we expect to see further signs of improving worker supply and a possible tick higher in unemployment, wage pressures remain strong and this could keep services inflation buoyant, which will concern BoE policymakers. The UK headline inflation rate should continue its decent as energy bills fell by almost 20% in July and food inflation continues to fall, but according to the BoE, services inflation risks ticking up from 7.2% to 7.3% on a year-on-year basis. We also have UK consumer confidence and retail sales data published on Friday, but these will play second fiddle to wages and inflation.

The 100-day moving average for GBP/USD is located at $1.2611 and this is likely to be the next downside target for FX traders betting on sterling depreciating. Meanwhile, GBP/EUR managed to score a weekly gain last week and is trading about 1% above its 1-year average but continues to lack conviction around the €1.16 level.

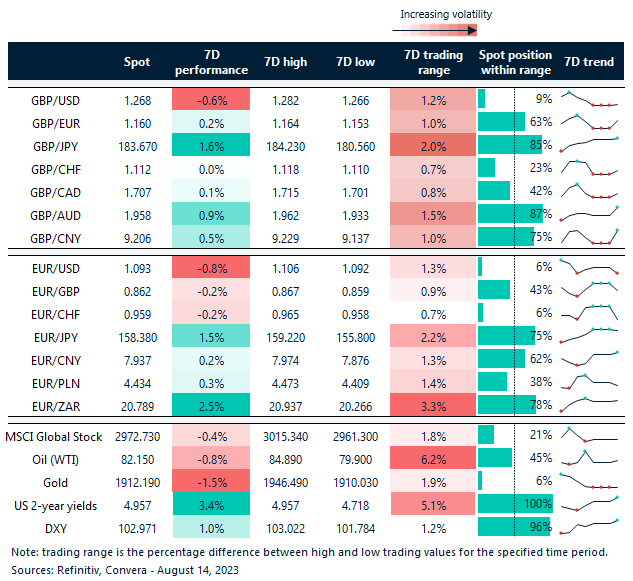

Risk assets on the defensive

Table: 7-day currency trends and trading ranges

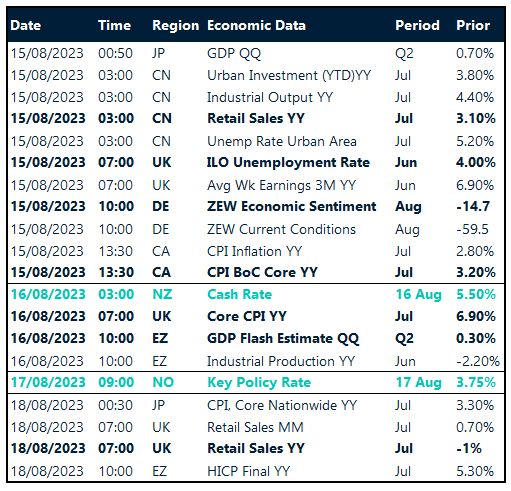

Key global risk events

Calendar: August 14-18

Have a question? [email protected]

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.