Global overview

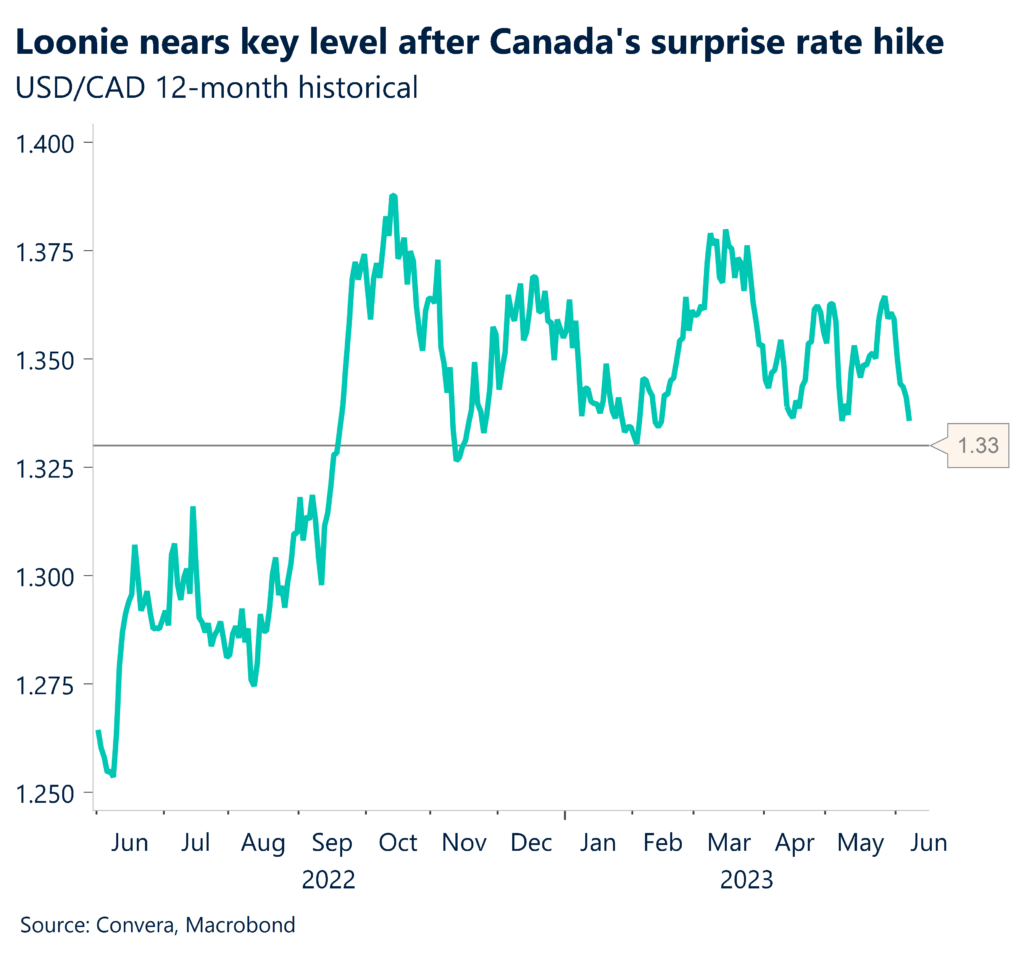

A more hawkish near-term outlook for monetary policy abroad kept the U.S. dollar index below recent mid-March peaks. The dollar posted declines versus its European and Canadian counterparts a day after the latter’s central bank unexpectedly restarted inflation-fighting interest rate hikes. The Canadian dollar rose to one-month highs after the Bank of Canada raised rates to 4.75% from 4.50%, its first increase since January that lifted borrowing rates to two-decade peaks. The greenback also has drifted lower this week after tepid services sector data suggested the world’s biggest economy may be less resilient than previously thought. June, meanwhile, has put a heightened focus on central banks after surprise hikes this week by Australia and Canada. Markets are leading toward the Fed, which meets next week, holding borrowing rates steady for the first time since it embarked on its aggressive tightening cycle in March 2022. Given more elevated inflation abroad, both the European Central Bank and the Bank of England are expected to deliver more policy tightening over coming months, underpinning their respective currencies.

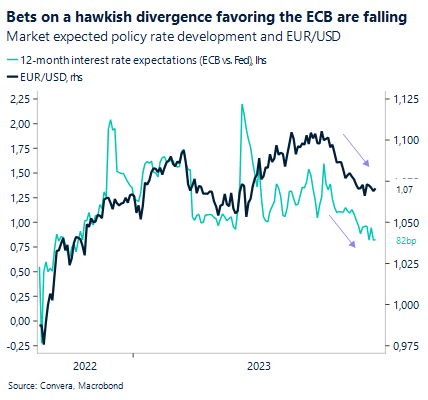

Euro sidesteps mild European recession

The euro fared more resiliently than the bloc’s economy as it edged up versus its softer U.S. counterpart. Gains for the euro may not prove durable after weaker than expected data revealed that the 20-country euro zone economy fell into a technical recession with back-to-back declines of 0.1% over the last two quarters. Though downbeat, the bloc’s contraction so far proving minimal hasn’t significantly impacted the euro. Still, scope for euro appreciation has diminished along with prospects for the ECB to outpace the Fed in tightening policy over coming months.

Sterling buoyed by hawkish UK rate stance

The UK pound was broadly steady in positive territory for the week against its softer U.S. rival. The buck has drifted lower this week versus counterparts whose central banks are thought to have more rate hiking to do this year than the Fed. The Bank of England was the first among the big central banks to hike rates to strangle inflation and it could outlast its chief peers, a hawkish outlook that has buoyed the pound, one of the year’s best performing currencies with a YTD gain of 3% versus the greenback.

C$ rises; U.S. jobless claims pop to 261K

A firm Canadian dollar stuck close to one-month highs against the U.S. dollar, a day after Ottawa surprised with a quarter-point rate hike to 4.75%, the highest level in 22 years. Canadian central bankers acknowledged greater concern about the inflation outlook that officials fear could take longer to return to their 2% goal. Canada issues its May jobs report Friday that, if solid, would strengthen the case for another loonie-positive rate hike as soon as July. The greenback added to session declines after more data challenged the view of a resilient U.S. economy. Weekly jobless claims jumped to 261,000 from a revised 233,000, coming in far above forecasts of 235,000. The jobs data could be an early sign of the Fed’s aggressive rate increases finally catching up with the labor market and slowing it.

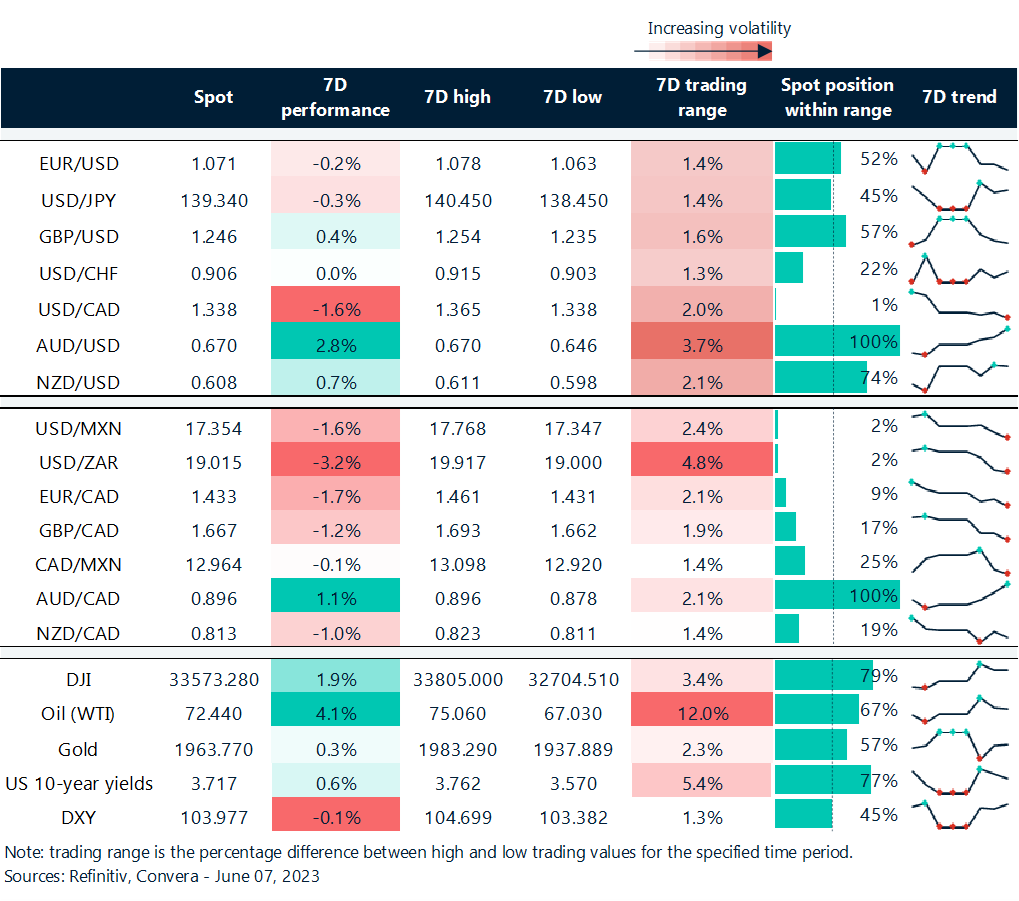

Dollar keeps toward mid-range levels

Table: rolling 7-day currency trends and trading ranges

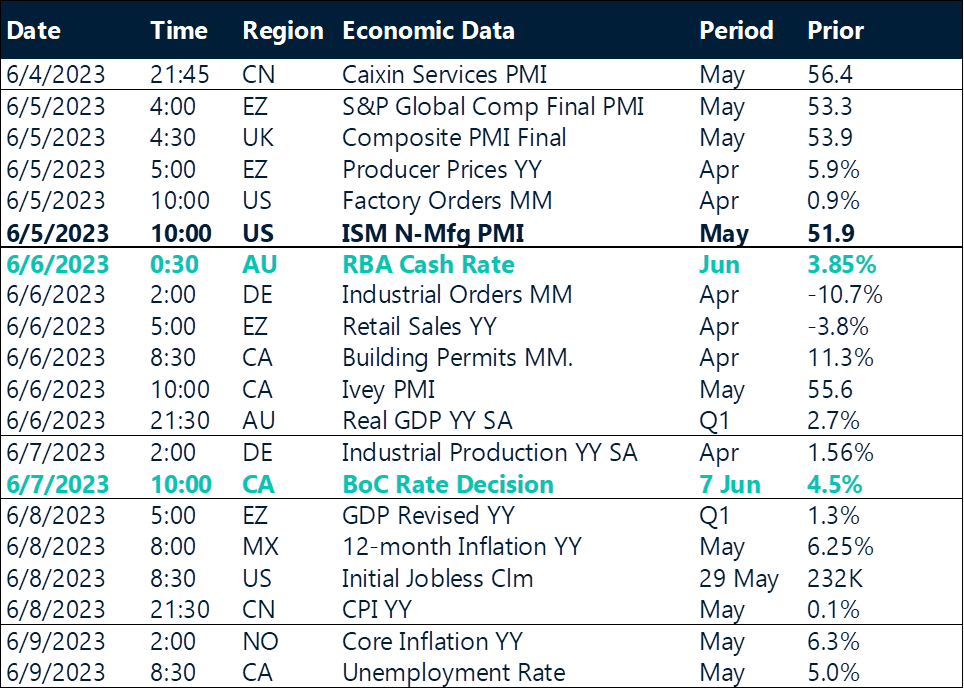

Key global risk events

Calendar: Jun 5-9

Have a question? [email protected]

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.