Fed hikes rates to 22-year high

The US Federal Reserve (Fed) raised interest rates by 25 basis points yesterday, in line with market expectations. The new target range for the federal funds rate is now 5.25-5.5% – the highest level since 2001 and just above its 7-decade average. The Fed did not close the door to further hikes, but nor did it close the door to cuts in 2024. The market reaction has been relatively muted, but the US dollar has lost marginal ground across the board, with EUR/USD toying with the $1.11 handle.

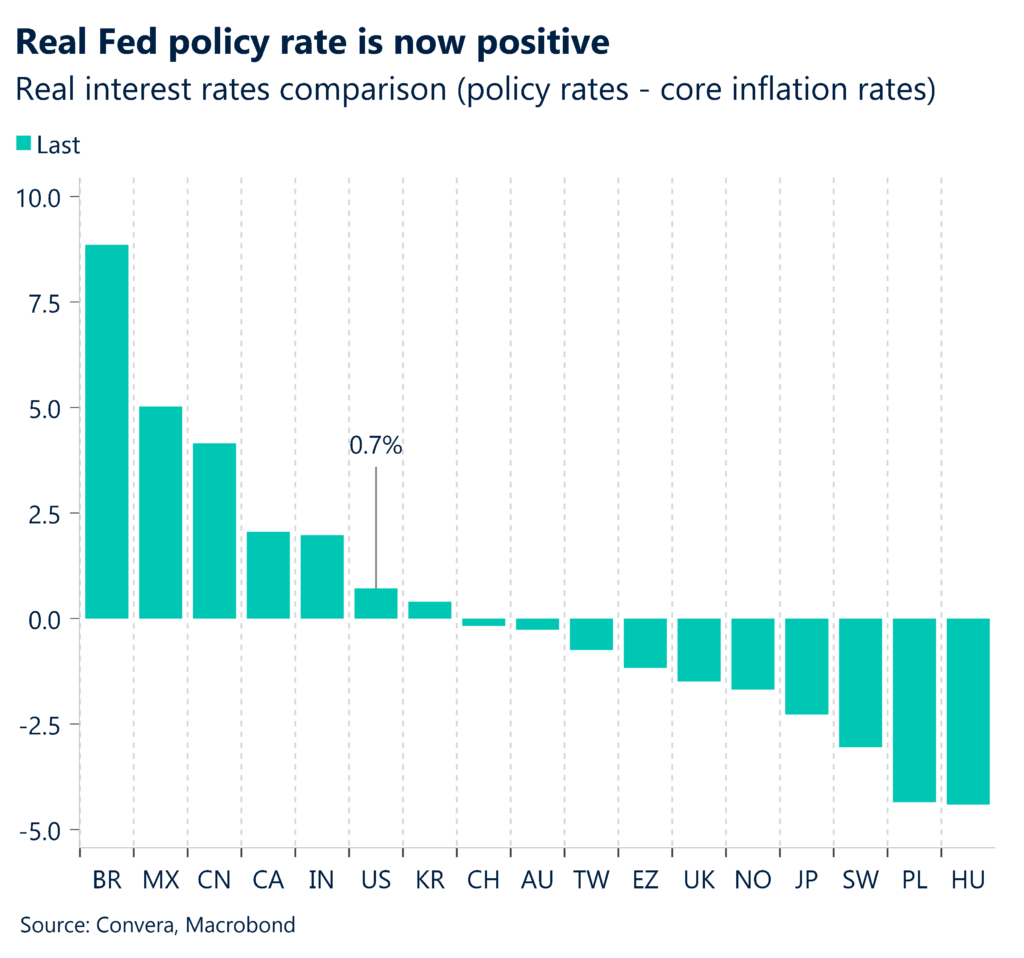

It was a fairly balanced presser from Fed Chair Jerome Powell, hence the limited volatility across financial markets. The Fed acknowledged the US economy has defied expectations of a sharper slowdown this year and upgraded its growth outlook from “modest” to “moderate”. Powell also welcomed the June inflation report but went on to stress the need to see more reports of this nature and will therefore remain data dependent, making policy decisions on a meeting-by-meeting basis. Should inflation continue to fall, the Fed could be “passively” tightening real rates without raising the fed funds rate further. However, falling inflation will also raise consumers’ purchasing power, sustain strong spending, and potentially refuel inflation, especially if the labour market remains tight. Interestingly, the latest rate hike means the real Fed policy rate (using the core CPI rate of 4.8%), is now positive, at 0.7%, which can be interpreted as a positive development for the dollar.

The Fed next meets in September and this will be a live meeting, meaning it could raise rates again, especially if the data is not decisive. Two more full rounds of monthly data on jobs, inflation and consumer spending will be digested in the interim. We expect the dollar to trade slightly on the softer side for now given rate differentials, but the gloomy economic backdrop elsewhere should prevent an aggressive dollar sell-off.

Will ECB switch to full data dependency?

Next up, the European Central Bank (ECB). Again, a quarter point hike is widely expected, but building evidence of an economic slowdown has called into question the chances of another hike by year-end. Will the ECB be in a pure data-dependent mode, which would likely weaken the euro? Or does it want to indicate that further hiking looks likely, which would probably strengthen the euro?

The common currency has held up surprisingly well this year given the bleak European economic backdrop and outlook. Germany remains in recession and France looks like it could soon follow. The hawkish ECB helps to explain some of the euro’s resilience, but it’s largely a result of upbeat investor sentiment since the hawkish policy divergence (ECB vs. Fed rate expectations) has clearly narrowed over recent months. Market participants will surely find it hard to ignore the feeble European fundamentals though, especially given the weakening momentum in the services sector and soft economic data pointing to a potentially longer economic downturn. So even if the ECB tilts to the hawkish side, the euro may not gain much ground as tighter for longer policy will only increase recession risks.

Currently, markets see the ECB cutting rates by around 75 basis points over the course of 2024, so we are looking for a firm “higher for longer” narrative to counter these bets. Otherwise, EUR/USD could slide back to $1.10 and GBP/EUR could climb back above €1.17, especially given the confirmation of a bullish reversal pattern on the daily charts this week.

BoE to follow next week

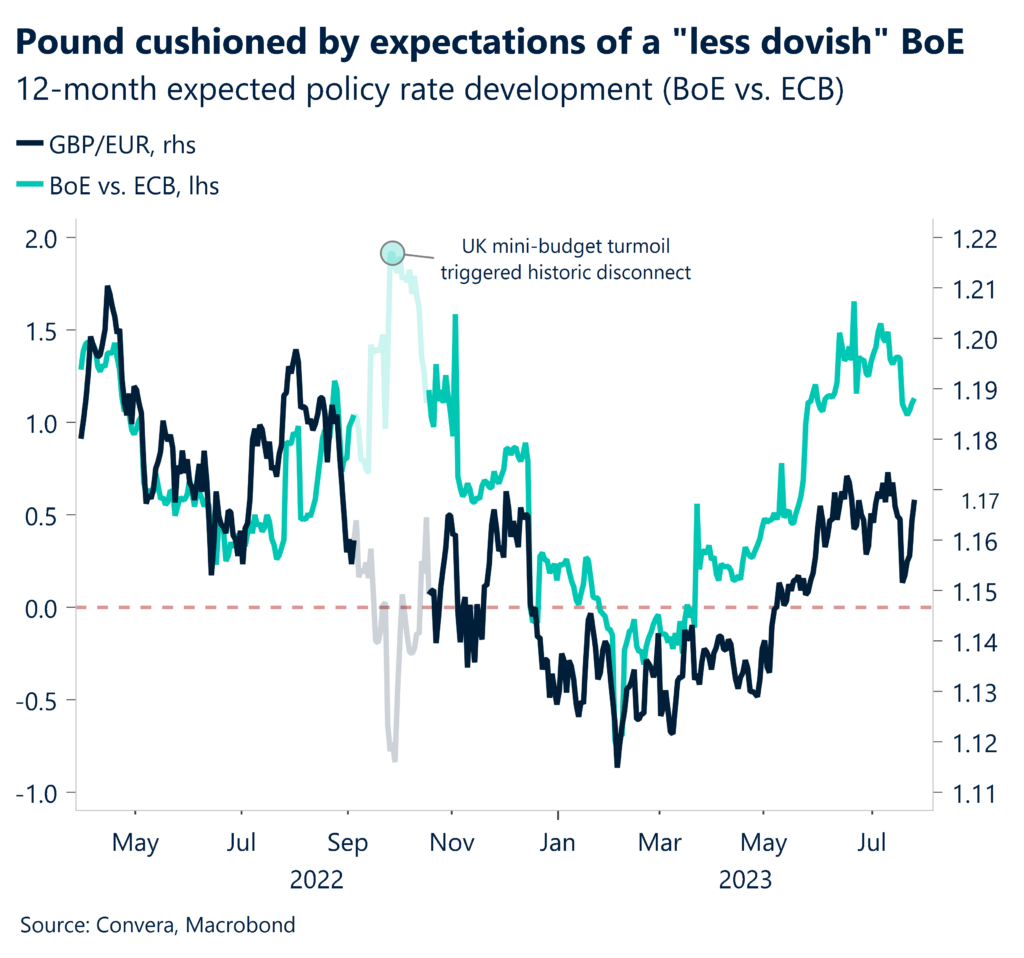

Following in the footsteps of the Fed (and likely ECB), the Bank of England (BoE) is widely expected to hike by 25 basis point next week, to a fresh 15-year high of 5.25%. There is a slim risk of a larger 50-basis point hike but given the latest UK inflation report surprising to the downside, the pressure has eased off the BoE, and the pound has suffered due to scaled back rate expectations and narrowing yield spreads.

Expectations for what the BoE signals when it meets next Thursday have shifted aggressively this month. Markets are now pricing UK rates to rise to around 5.8% by next March, but this is well below a peak of nearly 6.5% priced in just two weeks ago. As a result, UK-US two-year yield spreads have slipped back from 2014 highs in line with GBP/USD falling nearly 2% from 15-month peaks. Nevertheless, if markets continue to price US rate cuts versus UK rates staying higher for longer, this should remain supportive for the pound and limit any extended downside risks unless we see a repricing. Indeed, GBP/USD remains in an upward sloping trend channel that’s been in place since the record low of sub-$1.04 printed last September. Could we see a retest of $1.30 in the short-term? It’s certainly possible, especially if the BoE opts for what would now be a surprise 50 basis point rate hike next week.

Beyond the debate about the size of the hike, the vote split and forward guidance and any signals around potential quantitative tightening over the coming months will also be crucial factors that could inject some volatility into UK assets.

Dollar cedes ground after Fed meeting

Table: 7-day currency trends and trading ranges

Key global risk events

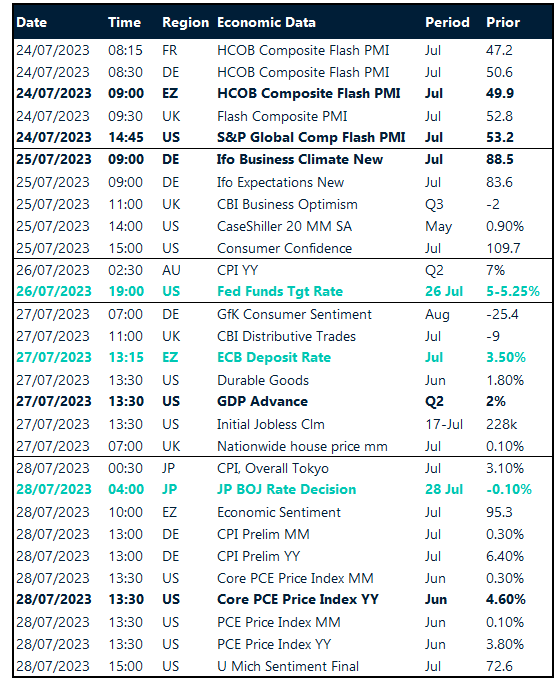

Calendar: July 24-28

Have a question? [email protected]

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.