Markets betting on US inflation easing

It is a big day for markets as investors brace for one of the most important data prints so far this year. Optimism surrounding a cooldown in US inflation, peaking short-term interest rates and renewed stimulus from China have supported equities this week. This has put some pressure on the US dollar, which is on track to record its fifth daily depreciation.

Both stocks and bonds rallied together in an attempt to price in better prospect of fiscal stimulus supporting the Chinese property market and the Fed nearing the end of its tightening cycle. The S&P 500 is up around a percent this week as two-year government bond yields eased from 5.10% on Friday to 4.85% today. The only data release from yesterday, the NFIB’s small business survey, did not generate any reactions across markets. The US Small Business Optimism Index improved to a seven-month high but remained below its long-term average for the 18th consecutive month. Looking at today’s highlight, economists expect US inflation to have cooled from 4% in May to 3.1% in June with core inflation estimated to fall from 5.3% to 5.0%.

Expectations for a big drop have accumulated in recent weeks given that the June print benefits from a negative seasonality bias – inflation peaked last summer– and that used car prices declined by 10% since March. FX markets have already positioned for a weaker print with EUR/USD ($1.1030) closing in on its cyclical highs at around $1.11. Given that such a disinflationary print is expected, any miss to the upside would rattle markets and lead to a sell-off in risk assets.

30 pips shy of $1.30

GBP/USD continues to scale 15-month highs after strong UK wage growth data keeps the spotlight on Bank of England (BoE) rate hikes. The currency pair has peaked this morning at $1.2970 at the time of writing. A softer than expected US inflation report today could be the catalyst to drive the pound back above $1.30 for the first time in 318 days. Meanwhile, the BoE has released its biannual Financial Stability Report (FSR) and the results of its latest stress tests of the UK banking system.

Real wages are improving because nominal wage growth remains at record high levels as inflation falls back. But while good news for working households, policymakers will view strong wage growth as a worrying development in the fight to limit the second-round impacts on inflation. Thus, money markets are currently pricing a 70% chance of the BoE hiking by another 50 basis points next month and to lift its key rate to 6.25% by December. UK rate and yield differentials are currently supportive for the pound but growing fears of a housing crisis amid rising mortgage costs, remains a strong headwind for the UK economy and currency. In its FSR, the BoE acknowledged rising interest rates as a big risk for growth and household debt levels, but stated banks are resilient and are strong enough to support their customers.

The UK economy has so far been resilient to interest rate risk, though it will take time for the full impact of higher interest rates to come through. The BoE estimate that the proportion of income that households spend on mortgage payments will climb from 6% to 8% by 2025. Could these looming delayed risks be the obstacles to deter the pound from rising much higher? Is $1.30 the potential top of a new long-term trading range perhaps?

Euro indifferent to European data

European investors are happy to step back and let US and global events guide domestic markets this week. The news from China surrounding the likely adoption of more property supportive policies with the aim to ensure the delivery of homes under construction has been welcomed in Europe, especially against the backdrop of easing yields this week. At the same time, the euro’s realised volatility has been the lowest since its inception, with EUR/USD having only moved by $0.05 from its low to high points so far this year.

It is impressive how unresponsive the common currency has been to incoming macro data. The trend of weaker economic and inflation prints has continued this week. The ZEW economic expectations index for Germany dropped to -14.7 in July from the previous months reading of -8.5. Sentiment is the weakest since last December with investors giving up hope for a quick summer rebound. Investors’ expectations of rising inflation have fallen to the lowest level since the ZEW institute began asking investors about price developments in 1999, while expectations for interest rates to rise remain extremely elevated.

Hawkish central bank speech has been able to push up the front end of the curve, but the backdrop of faltering economic growth is starting to limit policymakers’ commitment to hike rates beyond July. The euro remains sensitive to changes in US policy rates and indifferent to European data as long as the ECB keeps up its hawkish rhetoric. This is why inflation prints matter more in Europe than in the US.

Sterling scales 15-month peaks

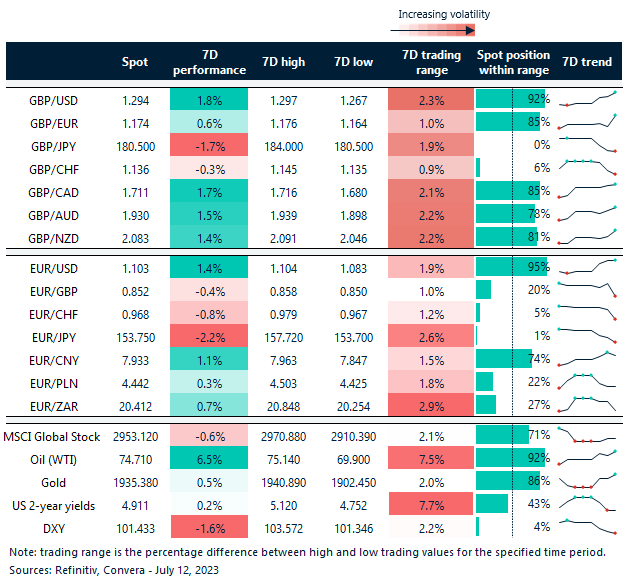

Table: 7-day currency trends and trading ranges

Key global risk events

Calendar: July 10-14

Have a question? [email protected]

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.