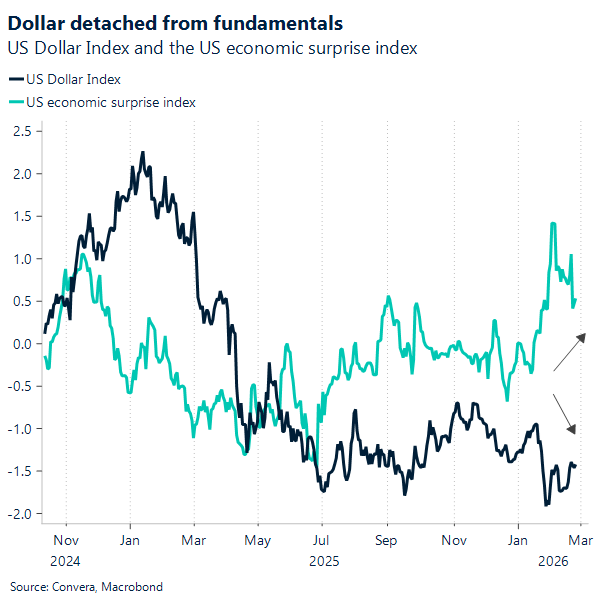

USD: Dollar direction derailed by conflicting signals

At the moment, renewed trade uncertainty is leaning dollar‑negative, while escalating US–Iran tensions and higher oil prices are leaning dollar‑positive. These opposing forces are pulling the dollar in different directions, which is why we’re not seeing a clean trend. Until one narrative clearly dominates, choppy, range‑bound trading is the most likely outcome. Little reaction came from the dollar after investors gave a lukewarm response to Nvidia’s above‑expectations earnings. The persistent sense of unsatisfaction with upbeat earnings highlights lingering skepticism around an AI‑inflated economic narrative. Even so, the broader tone across equity markets has improved this week, which is preventing the dollar index from drifting north of the 98 level despite its weakened safe‑haven appeal.

The US Supreme Court’s ruling on IEEPA tariffs — and the subsequent shift to 10% replacement tariffs — has revived structural dollar‑bearish arguments, particularly around fiscal sustainability and the case for greater global FX diversification. Still, this alone is unlikely to drive a sustained leg lower without a softer US cyclical backdrop, which has yet to materialise.

Geopolitics are still acting as a major swing factor. Crude briefly dipped after reports that Hezbollah wouldn’t retaliate against limited US strikes on Iran, which helped dial back immediate fears of a wider regional flare‑up. The move pushed both WTI and Brent into negative territory, a reminder of just how quickly energy markets react to even small shifts in the narrative. And while President Donald Trump reiterated that diplomacy remains his preferred route, visibility over the coming days is low and headline risk remains high.

Yet when it comes to the dollar’s broader role as a safe haven — not the version propped up through the oil channel that the dollar dominates — we continue to see clear signs of erosion. Yesterday’s skeptical reaction to Nvidia’s above‑expectations sales forecast underscored this shift. The numbers failed to impress investors amid growing doubts about an overheated AI economy. Today’s softer dollar tone highlights its loosening grip on investors when they seek refuge in risk‑off moods.

Stepping back, though, our broader view is unchanged: we still expect a weaker dollar in the second half of the year. That’s anchored in an anticipated US growth slowdown and the prospect of Fed rate cuts. We’re not calling for a repeat of the sharp dollar decline seen in 2025, but the concentration of risks in the US — not least the political uncertainty heading into the midterms — continues to tilt the balance to the downside in our view. Near term, the dollar remains messy and two‑way. Further out, the macro backdrop still argues for softness, though we’ll need a more consistent run of bearish dollar cyclical news to build stronger conviction.

GBP: UK politics priced for pessimism

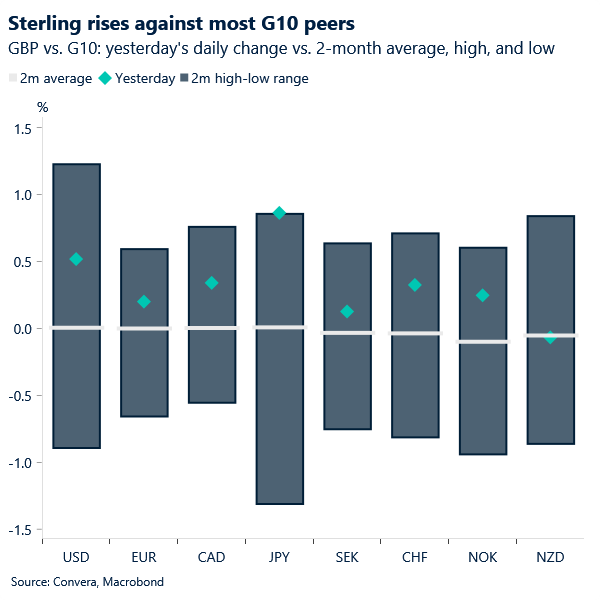

Sterling had a modestly good session yesterday despite quieter markets. The FTSE 100 hit new record highs on strong results from HSBC. The banking sector, alongside more traditional areas such as mining, have attracted renewed interest at a time when the tech sector faces heightened scrutiny amid growing concerns around AI. As a more traditional bundle of equities, the FTSE 100 has, therefore, seen a clear pickup in demand.

Meanwhile, at a time when public affairs appear to blur the independence of central banks globally – see Japan, Europe and the US – it is hard not to notice the relatively healthier UK government –BoE relationship. Barring significant negative surprises from today’s by‑election, we see this backdrop offering underlying support for sterling.

On the BoE easing outlook, the February’s policy meeting clearly leaned dovish, with policymakers effectively betting on a mechanically engineered sharp drop in headline inflation in the months ahead. With no further inflation reports due before the March meeting, markets are left to interpret BoE commentary that has so far failed to reinforce that dovish shift. Caution is likely to persist: Inflation still has a long way to fall, and the outlook for oil – of which the UK is a net importer – has been revised less bearishly for the year. February 20th saw the strongest pricing for a March cut at about 86 percent, which has now receded to roughly 73 percent.

Technically, GBP/USD continues to show reluctance to break more decisively below key support levels such as the 200‑day moving average at 1.3448. GBP/EUR has also recently reclaimed its 100‑day moving average. Both signals suggest that the risk premium embedded in the options market is still failing to materialise in spot. In both pairs, we would refrain from calling for more sustained losses unless the lows at 1.3331 for GBP/USD and 1.1368 for GBP/EUR were to be closed below.

Today’s by‑election is an important test for sterling. Expectations have leaned toward pessimism around UK politics, and the options market has clearly captured this through the recent rise in the premium investors are willing to pay to hedge against GBP weakness. This widens the window for positive surprises today. That said, as noted above, there is still unrealised downside that spot has not reflected, which means a negative election outcome could still generate a meaningful move in FX.

EUR: Steady now, stronger later?

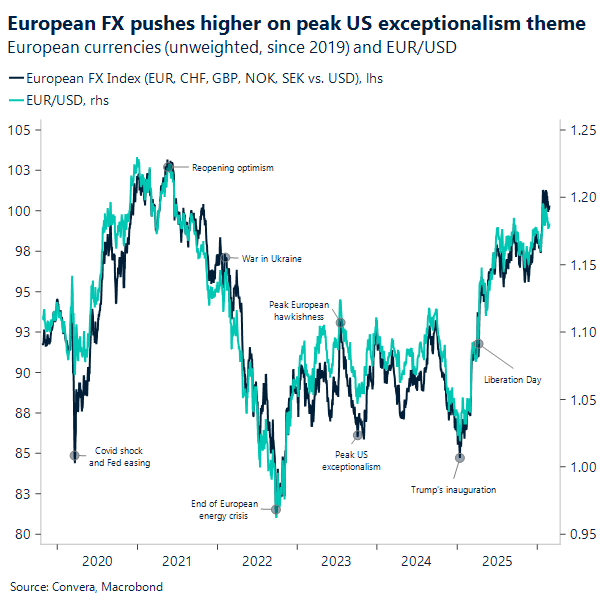

The euro‑area’s €800 billion fiscal package — including Germany’s €500 billion contribution — was a major bullish EUR catalyst last year, even though its growth impact was always expected to show up from 2H26 onwards. Still, early signs of that support are starting to appear. Germany’s Ifo index rose to 88.6 in February, its strongest reading since last summer, with both the current‑assessment and expectations components improving.

The broader picture is that fiscal spending, particularly in defence and infrastructure, is beginning to filter through via firmer order books and lower inventories. If this momentum builds, it could offer the euro some structural support by helping stabilise Germany’s industrial base and easing concerns that Europe is stuck in a low‑growth pattern.

At the same time, as outlined in the USD section above, the period of clear US outperformance may be behind us. Global investors are increasingly aware of how heavily their portfolios are tilted toward US assets, creating scope for further USD diversification. That process takes time, but it still leaves room for EUR/USD to push toward $1.22 before year‑end.

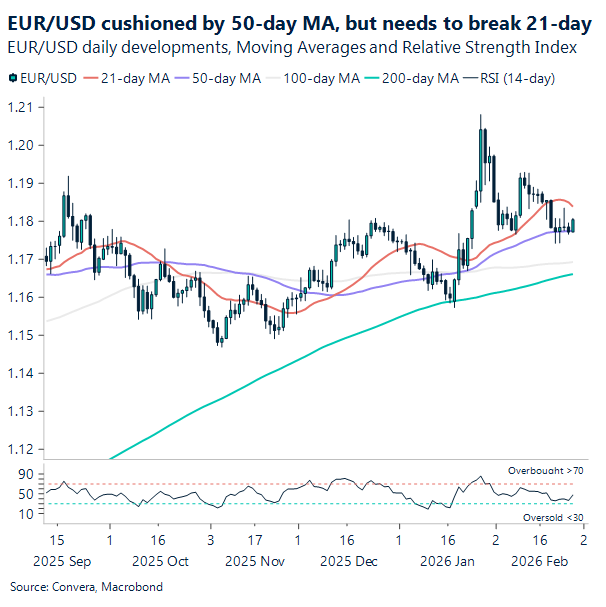

Near term, though, the euro faces headwinds. Expectations for Fed rate cuts have been pared back, and the risk of higher oil prices amid geopolitical tensions is another drag. Technically, EUR/USD has held its 50‑day moving average this week, but the RSI has flattened and the 21‑day moving average has rolled over — both signs that the recent uptrend may be losing momentum.

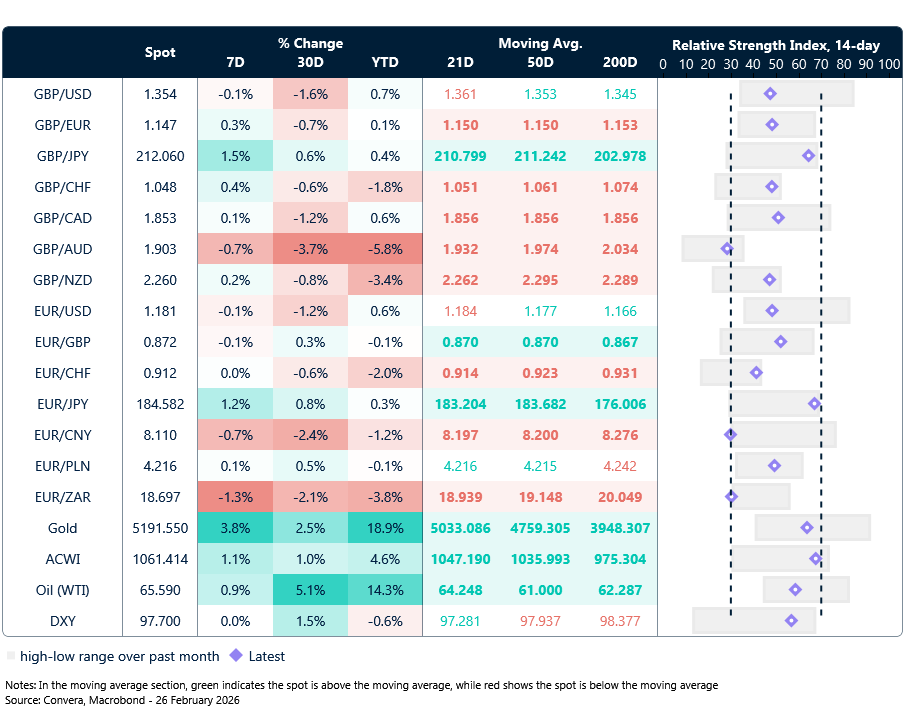

Market snapshot

Table: Currency trends, trading ranges & technical indicators

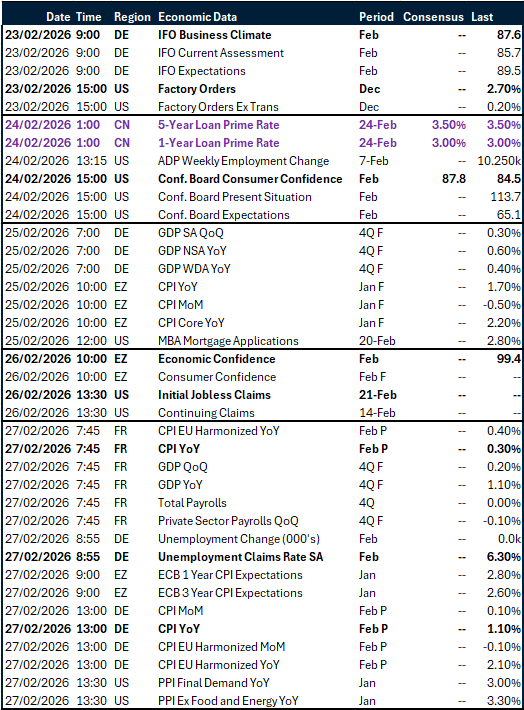

Key global risk events

Calendar: February 23-27

All times are in GMT

Have a question? [email protected]

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.