GBP/USD primed for best month since November

The British pound has risen nearly 3% against the US dollar month-to-date, heading for its largest monthly gain since November last year. Against the euro, it has barely budged. Banking sector woes remain confined to the US for now and systemic risks have subsided, which has bolstered demand for riskier assets, with the risk-sensitive pound benefiting.

Despite volatile market conditions, it’s been a positive start to the year for the pound all round. On average, sterling has risen 3% against its G10 peers – the biggest gains seen against the Norwegian krone (9.4%) and South African rand (7.6%) as well as the Japanese yen (4.1%) and Australian dollar (4.1%). Recent data from the UK reveals the surprising resilience of the UK economy, which is now expected to evade a recession in 2023. GDP data this morning showed the UK economy grew 0.1% in the final quarter of 2022, revised higher from a first estimate of no growth. Meanwhile, although inflation remains in double digits, consumer confidence has improved, and demand remains robust in the services sector. As a result, the Bank of England is unlikely to cut interest rates in 2023 and although traders now believe interest rates will top out at 4.5%, down from 5% at the start of March, the narrowing US-UK rate differentials favour the pound over the dollar, particularly since US rates are forecast to fall below UK rates in 2024.

Daily sterling charts show the technical picture is generally favourable as well, with GBP/USD holding firm above its key long-term rolling averages. In addition, the pound has been supported by improving soft economic data of late, helped mostly by the extended rebound in consumer and business expectations as evidenced by GBP/USD’s correlation with our soft UK data proxy.

No warning signs so far

As discussed in yesterday’s daily, the weekly release of the usage of the Federal Reserve’s (Fed) emergency lending facilities remains an important indicator for gauging the stress level within the banking and broader financial system.

While the overall borrowing of US institutions during the recent week decreased only slightly from $163.9 to $152.6 billion, it is important to note the change in the composition of the facilities being used. Borrowing via the Fed’s discount window has fallen three weeks in a row while the new Bank Term Funding Program continued to increase in parallel to $64.4 billion. The compositional shift could be a sign that liquidity demand may be stabilising and that policy makers efforts to limit contagion risks might be working. However, the flight into money money-market funds continued, showing that smaller banks most likely lost deposits during the last week.

The Fed’s balance sheet update will be followed by the release of data on the banking deposit developments today. Markets will closely follow the impact of the inflation print in the US as well, after German consumer prices came in stronger than expected yesterday. The consensus looks for an unchanged core PCE rate, however, given the recent macro volatility, deviations from expectations are more than likely. The US dollar index will most likely record the third weekly loss in a row on the back of higher risk taking and easing contagion risks materialising over the recent trading sessions.

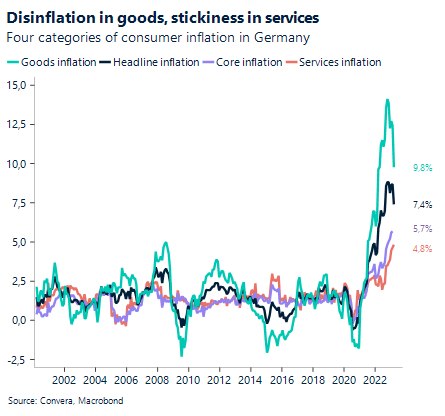

Sticky European inflation lifts euro

The euro received a boost yesterday after data showed German inflation eased less than expected in March, adding to pressure on the European Central Bank (ECB) to further tighten its monetary policy. This could close the policy rate gap between the ECB and the Fed going forward, a positive driver for EUR/USD, which currently grapples with the $1.09 handle.

German consumer inflation increased by 7.4% over the last twelve months through March, below the 8% mark for the first time in six months, but beating the consensus forecast of 7.5%. The decline in the inflation rate was entirely driven by a slowdown in energy prices, but with core and services inflation still stuck at the highest levels since the early 1990s, momentum behind a continuation of the ECB’s tightening cycle is building again. The latest data print strengthens the overall trend of falling goods and rising services inflation. So, while broader inflation indicators and price expectations indicate lower willingness to raise prices going forward, suggesting headline and goods inflation should continue their path lower, a resilient labour market and the higher inelasticity of the services sector to rate increases could mean that core inflation remains stickier than previously expected.

This morning, an unexpected fall in German retail sales has softened the euro slightly, but attention shifts to a first reading of March inflation for the wider Eurozone later this morning. If inflation doesn’t ease as much as expected, like in Germany, this could potentially support EUR/USD in erasing all of February’s losses.

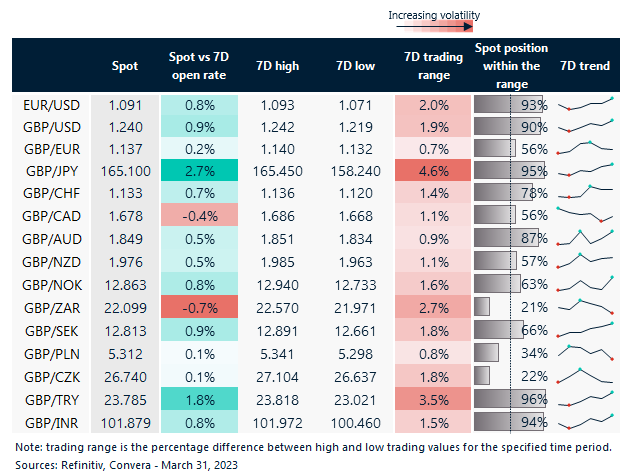

3.4% trading range for GBP/JPY in a week

Table: 7-day currency trends and trading ranges

Key global risk events

Calendar: Mar 27 -Mar 31

Have a question? [email protected]

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.