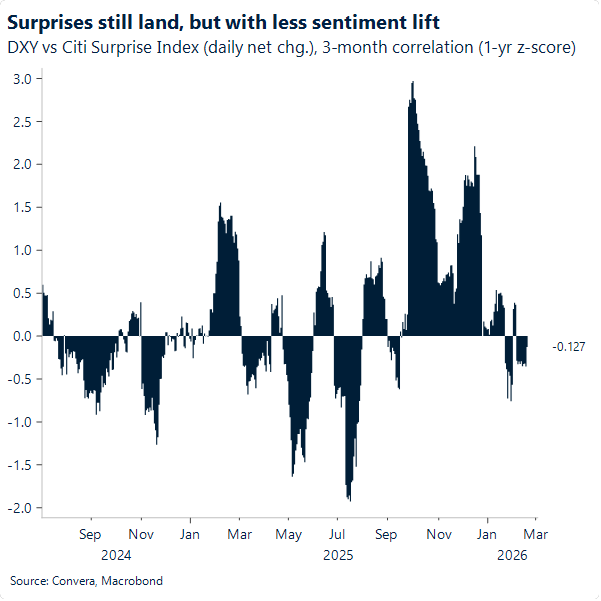

USD: Hawks and hotspots drive the dollar

The US dollar index extended its rebound from the January low of 95.551 yesterday, closing 0.2% higher. The index has risen every day this week and is now flirting with the 50‑day moving average, roughly aligned with the 98 level. With a deluge of US macro data due today – most notably the Personal Consumption Expenditure – we see scope for a test of that level (read more below). This week’s steady grind higher reflects a revitalised Fed hawkishness following the January minutes, as well as heightened geopolitical tensions as the US military stations a large array of forces in the Middle East to pressure Iran over its nuclear programme. Oil benchmarks have climbed this week – at the highest since the June 2025 Iran-US geopolitical flareup – adding support for the greenback.

Overall, these factors have helped suppress what remains a soft underlying sentiment toward the dollar. Investors are still disillusioned with the buck, with the debasement trade very much alive. The next key risk to watch is Warsh’s Fed chairmanship and how it interacts with President Trump’s preference for lower rates. But with the pick now known – and not as dovish as some alternatives – markets appear to be taking a breather from this risk, allowing the dollar to re-engage with its still hawkish-leaning rates-implied path.

Even so, a resilient US macro story for 2026 and its expected bullish effect on the dollar warrant a deeper look for longer‑term considerations. Investors may be reading the data differently than in 2025, when the dominant question was whether tariffs were dampening growth. Back then, positive surprises triggered more vigorous dollar rallies, helped by sentiment gains as evidence mounted that the US economy was weathering tariff impacts far better than feared. Today, with trade uncertainty largely diffused and resilience somewhat priced in, attention has shifted to more traditional questions – most importantly whether inflation is falling enough to justify further cuts this year. In the months ahead, we therefore expect the dollar’s reaction function to be more grounded, with positive surprises offering support but capping more meaningful bullish bursts.

But for now, we see the dollar edging back above the 98 mark, and that may well be the case today as the Personal Consumption Expenditure (PCE) deflator is expected to move higher. While largely priced in, the Fed’s expected disinflation path still implies inflation remaining above target this year, which is why we believe that even an on‑target print showing a hint of upside risk would keep the hawks on alert and have a more pronounced bullish impact on the dollar.

EUR: Rates attempt a grip on EUR/USD

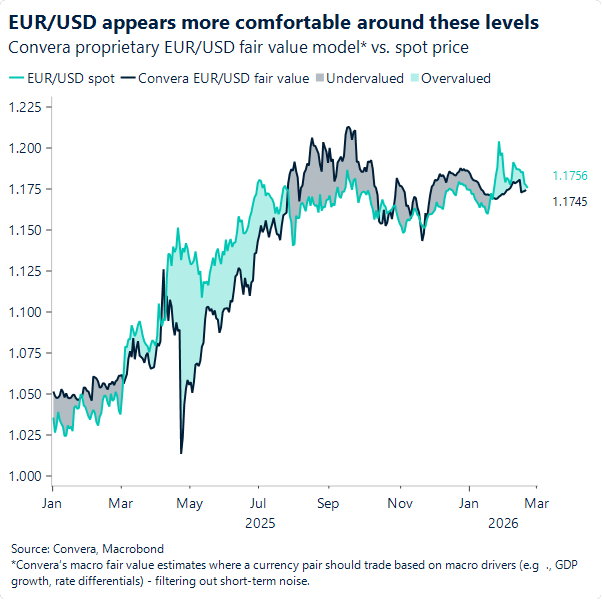

EUR/USD traded lower throughout the week and is now hovering below the 1.18 mark. A technical clean‑out after the ferocious rally that pushed the pair to highs last seen in 2021 partly explains the move lower. But widening rate differentials, along with heightened geopolitical tensions (see USD section), really forced the issue this week, attempting to overshadow the still‑soft sentiment around the dollar.

On the US side, strong ADP weekly change and firm industrial production data reinforced the narrative of a more stable labour market and resilient economic activity – messages that the Fed minutes packaged up and amplified. On the euro side, the headline was Lagarde stepping down earlier than expected. The move appears strategically political: it is intended to let leaders Merz and Macron have a say in the next ECB president before France’s 2027 general elections, with far‑right, euro‑sceptic Le Pen currently the favourite. The backdrop naturally reintroduces a degree of risk premium at a time when the “central bank independence” theme is back in focus (see the US, and to some extent Japan). Meanwhile, there were hints of dovishness tied to inflation undershooting, with ECB officials becoming more vocal about it and the rates market beginning to pay closer attention. Overnight Index Swaps now price roughly a 30% chance of a cut by November – telling, given that in December that tenor had a hike priced in.

That said, this week’s widening in rate differentials in favour of the dollar still looks brittle unless incoming data on both sides validates the dovish‑versus‑hawkish contrast between the ECB and the Fed. It is too early to make that call, not least because geopolitics is muddling the rates–FX pass‑through. We therefore refrain from declaring a sustained re‑establishment of 1.18 as well‑known resistance just yet, although that remains our medium‑term outlook as previously argued.

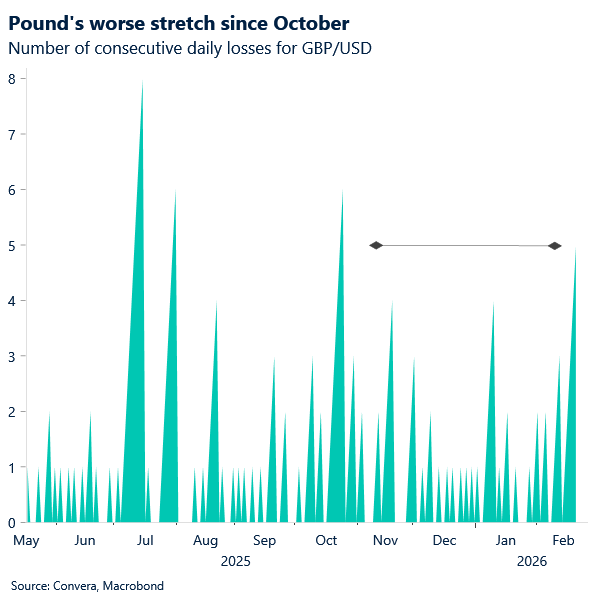

GBP: Markets overlook strong UK data this morning

Sterling is on track for its biggest weekly decline against the dollar in more than a year, down 1.4% as GBP/USD breaks through key support and flirts with its 200‑day moving average near $1.3445. The slide reflects a decisive dovish turn in UK data: unemployment has risen, wage growth has cooled and headline inflation dropped sharply, prompting markets to price an 80% chance of a March BoE cut. Catherine Mann’s warning about labour‑market risks only reinforced that shift.

This morning’s releases offered a rare counterweight. Retail sales surged 1.8% in January — the strongest monthly rise since May 2024 — while public finances posted a record £30.4bn January surplus. This will give the UK Chancellor something positive to point to in her Fiscal Statement on 3rd March, although it hasn’t made much of a dent in the UK’s national debt.

Even with today’s upside surprises, the pound remains hostage to a labour market losing momentum and inflation falling faster than expected. The result is a currency still struggling to find its footing. Markets are now treating every soft UK print as confirmation the BoE will have to move earlier — and sterling is trading accordingly. All of this leaves the UK currency vulnerable, with its risk premium largely eroded and fresh political noise expected around next week’s by‑election likely to add another layer of pressure.

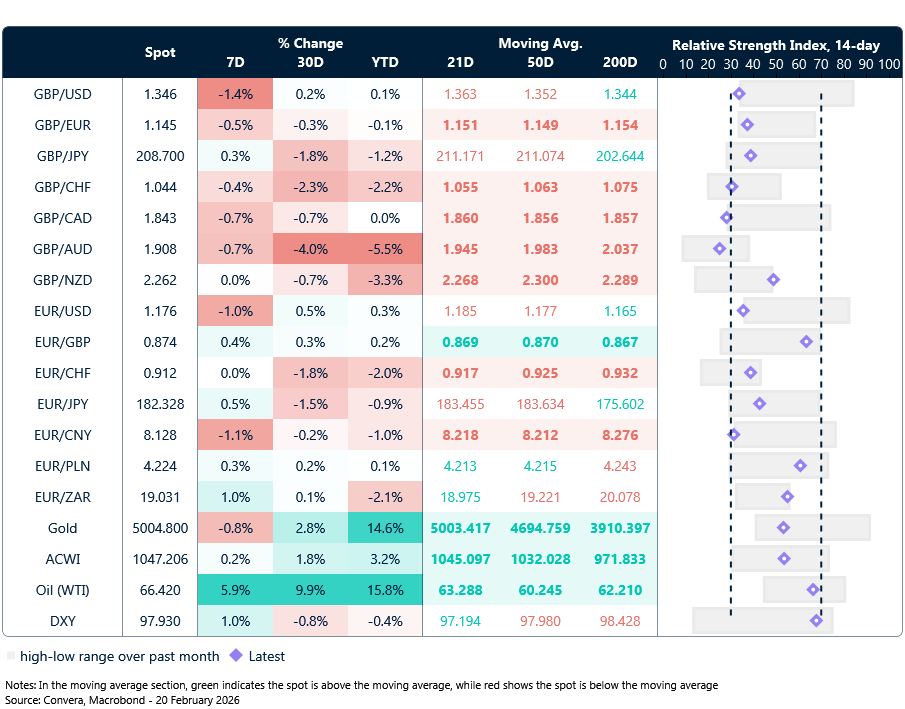

Market snapshot

Table: Currency trends, trading ranges & technical indicators

Key global risk events

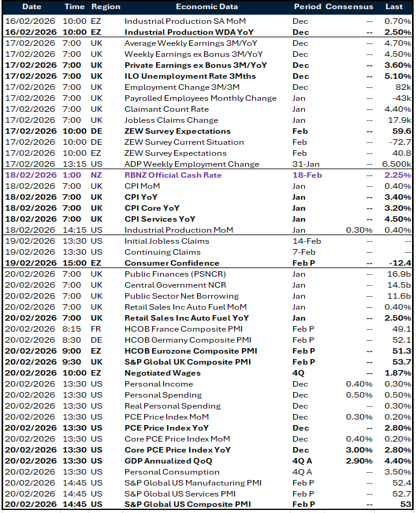

Calendar: February 16-20

All times are in GMT

Have a question? [email protected]

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.