USD: “TACO” trade still alive and well

For much of last year, the so‑called “TACO trade” — the idea that “Trump Always Chickens Out” — gained traction across global markets. It reflected a pattern in which tariff threats were ultimately followed by a step‑back and a declaration of victory, sometimes even resulting in outcomes more favourable to the targeted country than to the US.

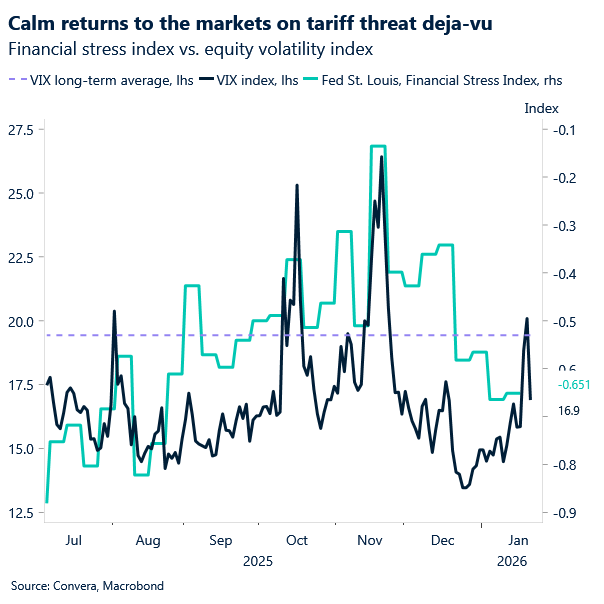

It appears the hallmarks of Trump’s early second‑term playbook are still in force, with US assets rallying sharply after the President stepped back from his Greenland‑related tariff threats during the World Economic Forum in Davos. Calm thus returned to markets with both equity and bond volatility gauges erasing the previous day’s jump. The shift triggered a broad, cross‑market rebound, lifting risk sentiment and driving a strong move higher across major US asset classes. Stocks surged, the USD found tepid support, and long‑end Treasuries rallied as investors unwound the bearish positioning that had accumulated during weeks of rising US–Europe tensions.

Still, it may be too early to assume tensions have fully eased. While markets welcomed Trump’s comments, he simultaneously increased pressure on Europe, arguing that NATO should support US claims over Greenland.

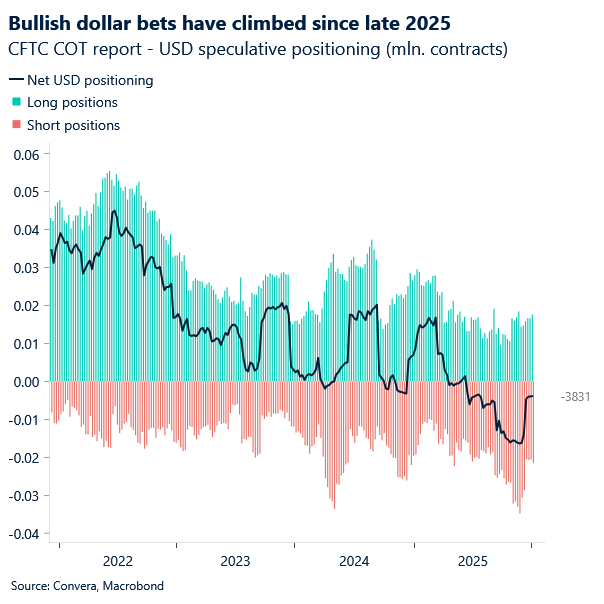

Tariffs remain a key vulnerability for the US dollar, even without a full‑blown breakdown in NATO. Markets tend to punish self‑defeating policy risks, and the dollar is already trading at a negative premium relative to where unretaliated tariffs alone would place it. Concerns around Fed succession, political interference, and the potential for foreign investors — particularly in Europe — to increase FX hedging add further downside pressure. Positioning also works against the dollar: investors entered the year with heavy long exposure, justified by strong US data and fiscal stimulus, but vulnerable to any negative shock that could trigger a squeeze into alternative funders such as the euro.

For now, the de‑escalation over Greenland gives investors space to refocus on earnings, growth trends, and Federal Reserve policy. Attention today turns to the third estimate of Q3 GDP and the Fed’s preferred inflation gauge. While the year‑on‑year inflation rate likely ticked higher in November, the underlying details should confirm cooling price pressures in core goods. As tariff‑related inflation risks fade, we expect a broad enough coalition on the FOMC to support resuming rate cuts around mid‑year.

EUR: Euro caught between sentiment and fundamentals

Substantial signs of de‑escalation emerged in Davos yesterday, with President Trump not only dismissing the idea of any military intervention to take over Greenland but also suggesting that a “framework of a future deal” has been agreed. As a result, he has pulled back from imposing tariffs as of February 1st.

There is still little detail about this framework, and it certainly raises questions. Danish foreign minister Lars Løkke Rasmussen appeared to welcome the latest developments despite having expressed firm opposition just earlier the same day to any negotiations involving ceding the territory to the US.

EUR/USD was bound to pare back some of its earlier gains this week. After testing resistance at 1.1740, the pair slipped back into the 1.16 zone, closing 0.34% lower.

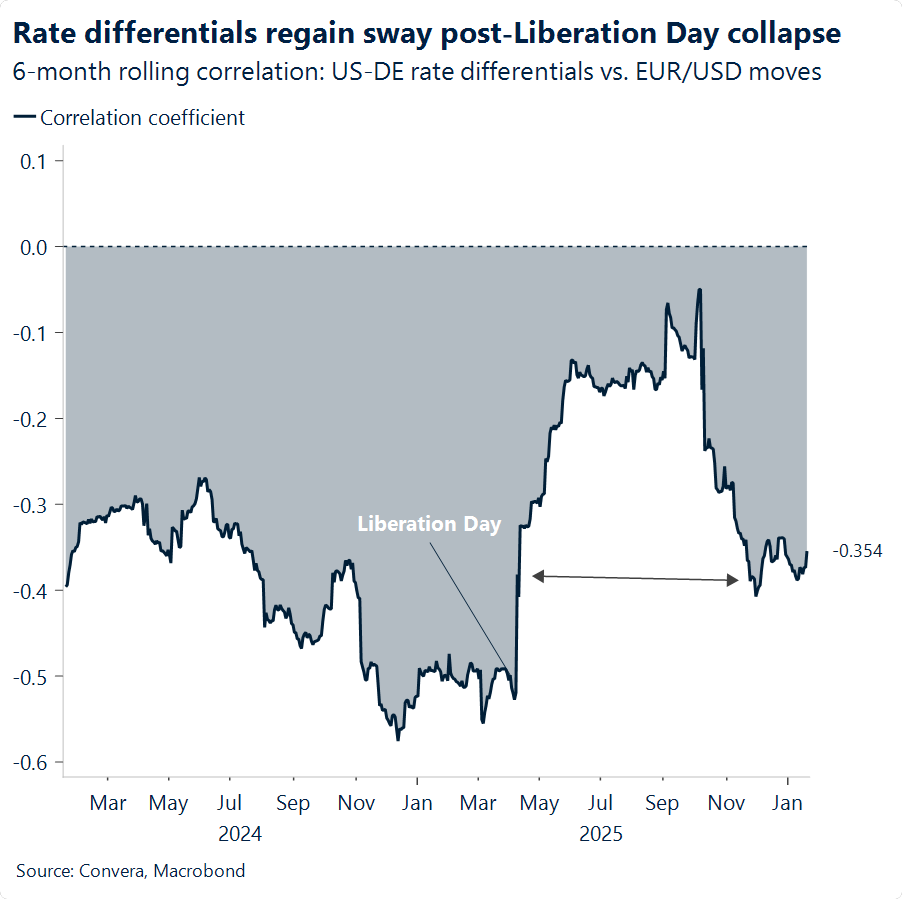

This week we have seen sentiment‑driven demand flow into the euro, disrupting the cautious bearish momentum that recent Fed‑led hawkish repricing had begun to imprint on EUR/USD. Even so, the macro story is set to remain the dominant driver of the dollar’s moves. Unlike at the start of 2025, when the dollar began falling sharply against the euro, investors now have some “history” to lean on. That experience tempers the impulse to fully embrace the sentiment narrative and keeps the focus on the macro one instead.

First, there is the question of economic growth. The US has weathered tariffs surprisingly well, with inflation rising less than anticipated. That reduces the economic uncertainty markets would otherwise price in if tariffs on Europe were to increase. Second, Europe’s stark divisions, which contributed to the poorly negotiated deal with the US back in July, remain visible. Some leaders, such as President Macron, are openly pushing back, while others, including German Chancellor Merz, are seeking dialogue instead. These two “pieces of evidence” inevitably act as cushions when USD sentiment trembles, and certainly help explain markets’ more sanguine posture toward the US dollar at the onset of 2026.

GBP: Sterling’s bounce meets macro reality

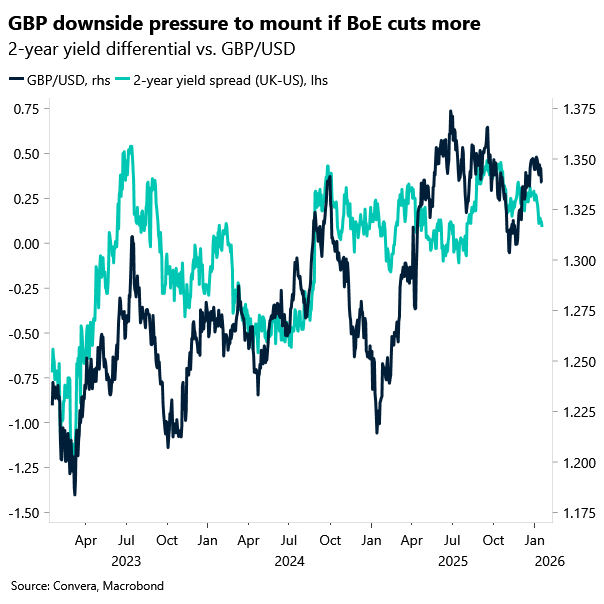

The de-escalation in geopolitics tensions has helped the British pound recover some losses against the euro and safe-haven currencies. However, although the overall impact on FX was noticeable it has been unremarkable. GBP/USD still holds steady above $1.34, ending yesterday flat, whilst GBP/EUR has bumped into resistance at its 21-day moving average, struggling to reclaim €1.15.

Outside the geopolitical noise, the UK delivered a run of notable data this week. A steady unemployment rate supports the case for patience before cutting rates, while slowing wage growth across both ex‑bonus measures strengthens the argument for bringing cuts forward. The mixed inflation report didn’t shift Bank of England pricing, leaving markets broadly unmoved.

With fewer than two cuts priced for 2026, market expectations still look too conservative, setting a low bar for a dovish surprise. That leaves the pound vulnerable to rates‑driven weakness if incoming data continue to validate the BoE’s disinflation narrative.

Meanwhile, stress in the long end of the bond market remains an important dynamic to monitor. Over the past year, the USD, GBP, and JPY have been the three developed‑market currencies most prone to negative correlations with long‑dated yields — and they were also the worst‑performing G10 currencies earlier this week as the surge in Japanese yields spilled over into global bond markets.

This pattern points to fiscal concerns, rather than broad risk sentiment, becoming a more influential driver of FX behaviour. Markets appear increasingly sensitive to economies where long‑end yield stress intersects with questions around fiscal credibility, leaving those currencies more vulnerable when rates move sharply.

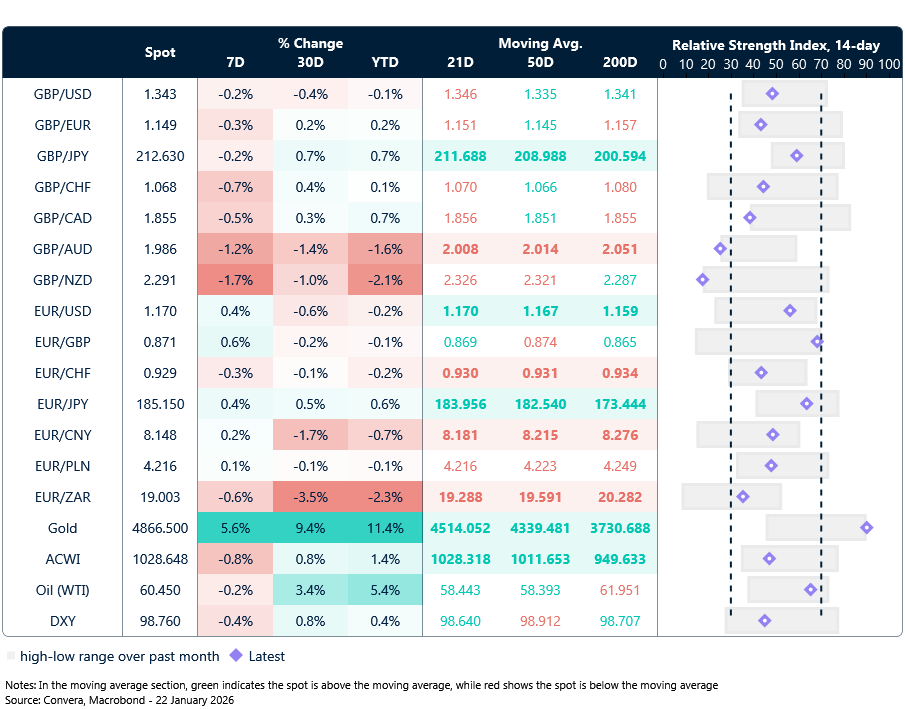

Market snapshot

Table: Currency trends, trading ranges & technical indicators

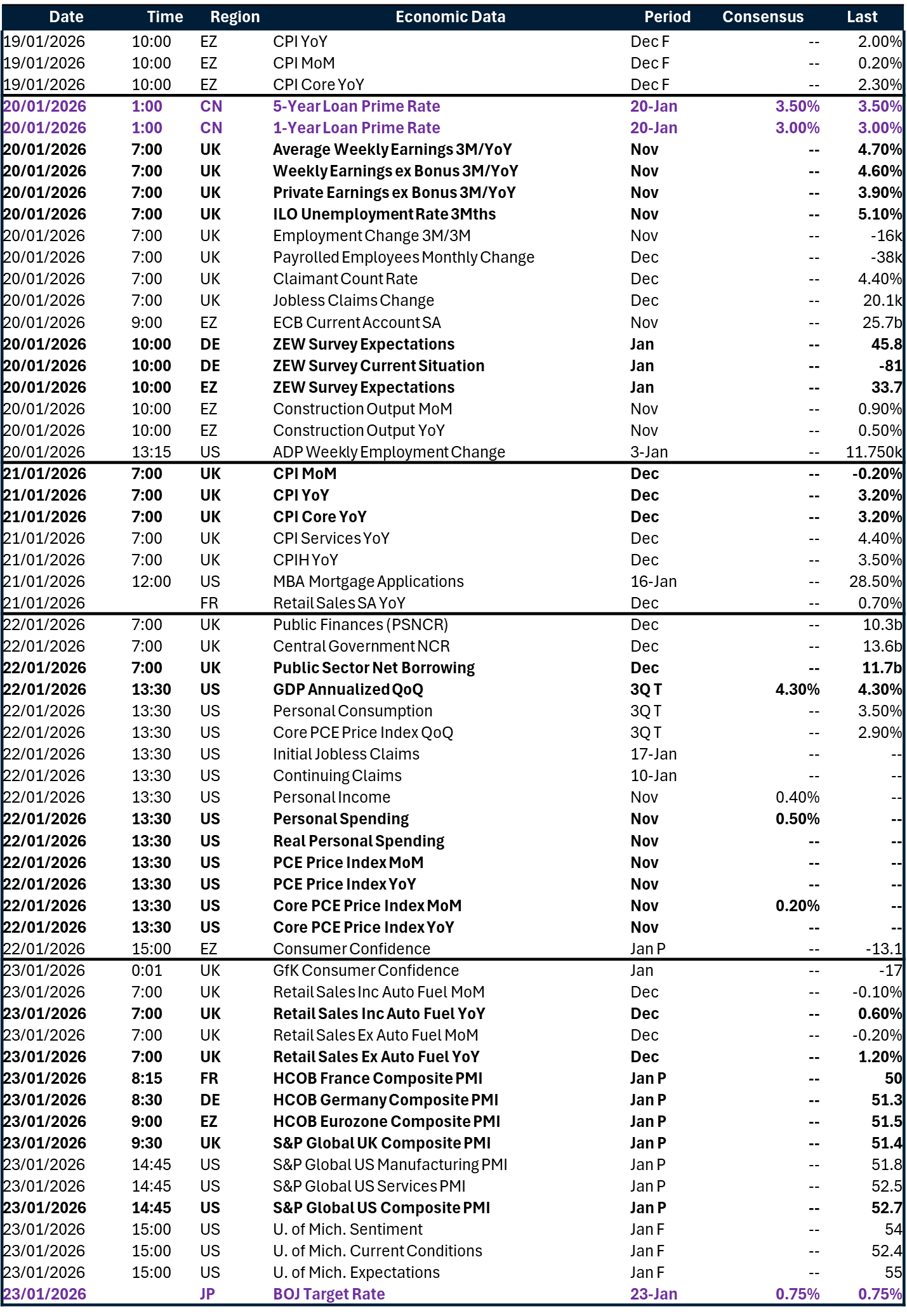

Key global risk events

Calendar: January 19-23

All times are in GMT

Have a question? [email protected]

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.