Written by Convera’s Market Insights Team

US dollar touches one-month high

Boris Kovacevic – Global Macro Strategist

Global markets started the week without liquidity from the United States, as trading in the country remained closed due to a public holiday. The lack of macro data and US trading volumes led to a lackluster weekly open, in which investors slightly pared back their bets on near-term rate cuts from the Federal Reserve. The US dollar seems to have broken out of the downside trend that had formed back in November and is on track to record its fourth consecutive daily rise.

This can be explained by 2-year Treasury yields rebounding today, after having fallen to their lowest level since May last week. Geopolitical tensions continue to linger around as the Houthi movement from Yemen announced an expansion to its targets in the Red Sea to include US ships. The yield rise across the curve and the geopolitical risk premium have pushed the US Dollar Index (DXY) to a one-month high at 102.90. Asian equity markets fell to a one-month low due to the same factors driving the Greenback higher, falling bets of a Fed rate cut in March.

The probabilities of this occurring have fallen from 77% on Friday to 65% today. The economic week in the United States will start slowly with no data scheduled to be released. Fed member Christopher Waller is expected to speak at an event today and considering that he was the policy maker initially responsible for markets pricing in the pivot to easier monetary policy at the end of last week, investors will pay close attentions to his comments.

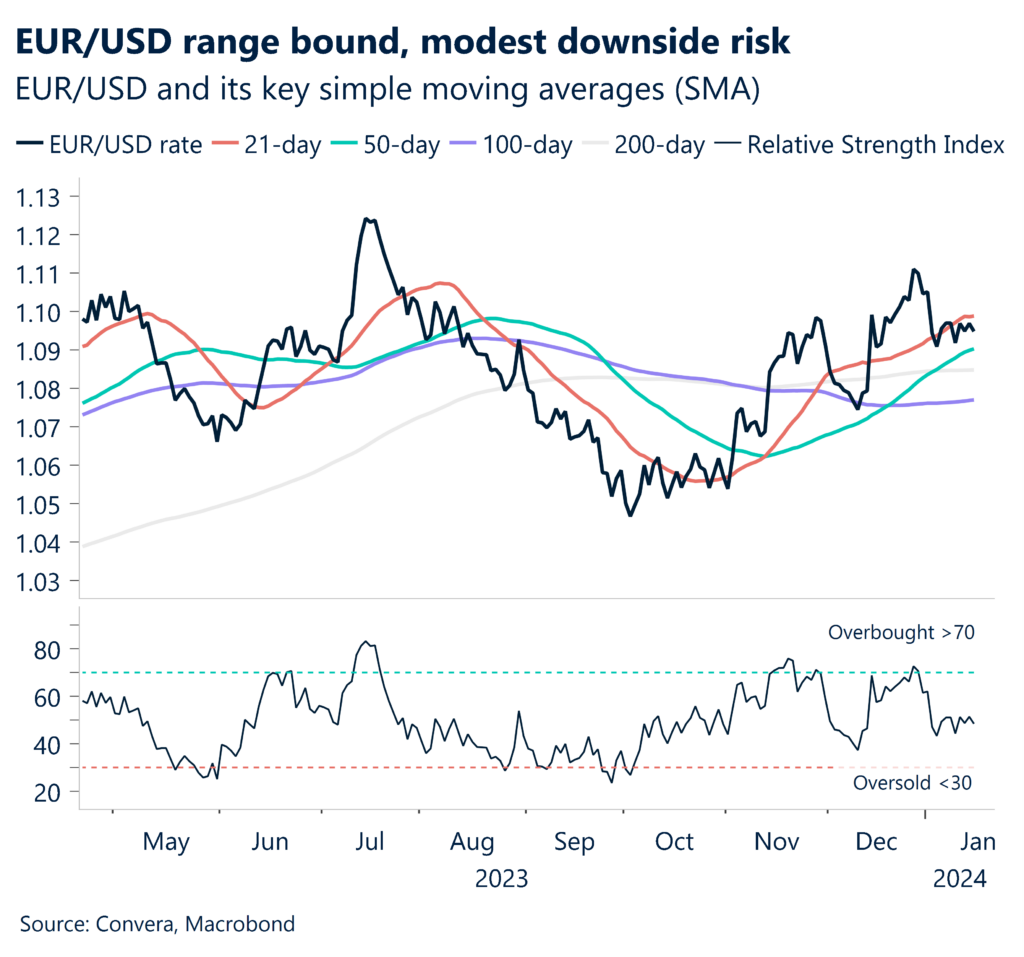

Hawks awaken as Germany contracts

Ruta Prieskienyte – FX Strategist

European stocks reversed early gains to trade in the red while EUR/USD finished the day flat in a largely uneventful day as most US markets were closed due to Marting Luther King Jr. Day. Investors geared up for a week filled with crucial data releases while carefully assessing the potential monetary policy outlook.

Earlier in the Monday trading session, the euro marginally depreciated (-0.2%) against the US dollar as a German report showed Europe’s largest economy contracted by 0.3% in 2023 as stubbornly high inflation, along with rising interest rates, dampened activity and demand from both home and abroad. Meanwhile, the Eurozone’s industrial activity shrank by 0.3% in November, marking the third consecutive month of decline. On an annualised basis, industrial activity shrank by 6.8% in November, exceeding expectations, and extending the current sequence of contraction to a ninth consecutive month.

On the policy front, investors are anticipating the European Central Bank (ECB) to kickstart interest rate cuts in April, despite Chief Economist Lane suggesting a more plausible rate-cut timeframe in June over the weekend. Adding to this, ECB policymaker Joachim Nagel emphasized on Monday that it is premature for the ECB to consider reducing interest rates due to the persistently high inflation. Furthermore, hawkish Robert Holzmann expressed scepticism about the likelihood of rate cuts in 2024 as a whole. However, investors would not budge their pricing on ECB rate cut expectations, which has been largely unchanged since 6th December, expecting 147bps cumulative rate cuts over the course of this year.

Looking ahead, EUR/USD faces a modest downside risk as escalations in the Middle East could provide support for the dollar via the risk-sentiment channel. A miss on the German ZEW index could also weigh down on the currency pair, dampening the beacon of hope of bloc’s economic recovery this quarter. We will also be closely watching Consumer inflation expectations due shortly, as higher consumer inflation expectations have been shown to increase consumption, which could feed through into the real economy.

Weak labor report weighs on the pound

Boris Kovacevic – Global Macro Strategist

The United Kingdom kickstarted a crucial week filled with tier one economic data releases with a disappointing labor market report weighing on the British pound this morning. Wage growth cooled more than economists had expected, adding to the speculations that the Bank of England would ease monetary policy sooner rather than later. Regular pay growth eased from 7.2% to 6.5% in the three months through November. While still well above the central banks target rate, the month saw the first sub-7% print in eight months, highlighting the current downside momentum. Investors have shifted to pricing in the BoE’s policy pivot in May, one and two months later than the ECB and Fed.

However, we think that the report adds to the case of the British central bank potentially having to ease monetary policy more than its peers with inflation still expected to fall below 2% in the first half of this year. The next macro data in focus will be the CPI print tomorrow morning, where core inflation is expected to fall from 5.1% to 4.9%. Today’s negative sterling price action confirms our view of the currency remaining sensitive to the incoming data. Investors are parsing through the data to see how likely the UK is to differ from its peers, justifying a different pricing path for the Bank of England versus the ECB and Fed. So far, there have been no indications that this would be the case. GBP/USD fell through the $1.27 level with cable expected to close below the threshold for the first time in eight days. Cable has been in an upward trend since November. However, a break below $1.2650 could bring the 50-day moving average at $1.2590 into play.

Key global risk events

Calendar: January 08 – 12

EUR/USD and GBP/USD fall through key levels

Table: 7-day currency trends and trading ranges

Have a question? [email protected]

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.