USD: Oil shock trumps dollar doubts

Over the weekend, the United States and Israel launched large-scale coordinated airstrikes on Iran, marking one of the most significant direct attacks on Iranian soil in decades. The strikes targeted military infrastructure and leadership sites, and Iran’s supreme leader, Ayatollah Ali Khamenei, has been reported killed. Iran has retaliated by striking Israeli cities and US military bases across the Middle East as both sides continue trading fire.

Risks of military escalation had built quickly in 2026. The US had assembled its largest military presence in the region since 2003 over the past few weeks, while discussions between the two sides aimed at securing a deal over Iran’s nuclear programme failed, closing off the diplomatic route entirely.

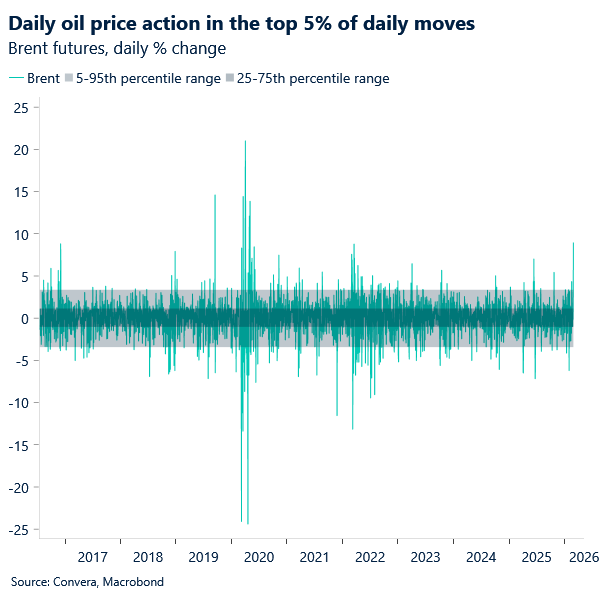

It is unclear how long the conflict will continue. President Trump has stated that he does not intend to stop until Iran’s hardline regime is overthrown, and that the assault can last “four to five weeks”. The path to achieving that goal, however, remains highly uncertain. While many unknowns persist, markets already have enough information to react. Brent has risen 8% near $79 a barrel, after earlier rallying by a much as 13%. It closed on Friday at $73 a barrel, having climbed 20% since the start of the year in anticipation of conflict.

Tanker traffic through the Strait of Hormuz, a key waterway for global energy supplies through which a fifth of the world’s liquefied natural gas and oil travels each day, has come to a halt. Iran has insisted the strait remains open, but it also attacked three oil tankers on Sunday, deterring passage further and prompting a self-imposed pause from shipowners and traders. In response, OPEC has announced on Sunday plans to raise oil output by 206,000 barrels a day from April. Meanwhile, Gulf states had been increasing oil loadings this year as escalation risks rose. These measures may help temper price spikes over the longer term, but for now there is little that can slow the move higher.

When it comes to the dollar, an oil‑centred geopolitical shock is precisely the type of risk event in which the dented credibility of the greenback does not prevent demand from rising – with the dollar index (DXY) up 0.8% since the Asia open. While one could group Trump’s militaristic move under the broader “erratic policy” risk that has undermined the dollar’s safe haven appeal since the start of Trump’s second term, there are structural factors at play that remain dollar supportive.

Firstly, with the US a net exporter of oil, unlike Switzerland, the eurozone and Japan, and with most energy transactions denominated in USD, the greenback tends to benefit during oil‑centred geopolitical flareups. Also, the breadth of the sell‑off away from risky assets triggered by the escalation generates mechanical demand for USD. Given its central role in global funding markets, deleveraging at a broad scale typically triggers automatic buying flows into the dollar.

Geopolitics is set to dominate price action in the coming days and weeks, overshadowing the push‑and‑pull between a more hawkish Fed and still‑fragile US‑led sentiment toward the dollar. We continue to lean on upside risks for the DXY based on a continued conflict and ongoing obstruction to the energy trade case.

EUR: Conflict premium turns euro soft

EUR/USD opened the week on the back foot after slicing through 1.18, a level that had acted as an anchor through much of last week and capped price action between the 21‑day and 50‑day moving averages. That threshold had been a defining resistance fortress since late 2025, with the pair repeatedly rejecting rallies before renewed soft USD sentiment in early 2026 finally allowed a brief topside break.

The euro’s vulnerability is straightforward. The bloc is a net oil importer, and the sharp rise in crude following the Iran–US escalation has delivered a clear deterioration in the eurozone’s terms of trade. Episodes of this scale also tend to erase whatever incremental safe‑haven appeal the euro has built against the dollar since the start of Trump’s second term.

The geopolitical overhang now injects a persistent bearish bias into EUR/USD, and we’re highly doubtful that this week’s US data can realistically counter it. Markets already understand that difficult weather conditions have weighed on early‑year activity, with implications for the labour backdrop. This means a softer jobs report and retail sales data (due Friday) may have struggled to generate much bullish impetus for EUR/USD even in a no‑conflict scenario. Euro upside risks, therefore, have become largely confined to a de‑escalation narrative to stabilise.

On the data front, look out for the eurozone CPI release for February (Tuesday). Following relatively benign country‑level prints last week, we are expecting an orderly outcome at 1.7%, unchanged from January, with FX pass‑through practically negligible.

GBP: Domestic strains, global jitters

Sterling heads into the week on the back foot, with domestic politics, softer data, and a dovish BoE shift now combining with global risk aversion linked to the erupted conflict to drag the currency lower across the board. Behaving like a high‑beta currency, the pound tends to sell off quite heavily when risk aversion picks up, with GBP/USD almost 1% lower since markets opened.

GBP/USD also closed February more than 1.5% lower, snapping a three‑month winning streak and erasing its year‑to‑date gains, though the broader uptrend in place since 2022 remains intact. Sterling has been sensitive to swings in global risk sentiment, but it also grows vulnerable to the re‑emergence of a UK‑specific risk premium as political uncertainty builds following Labour’s heavy defeat in the Gorton and Denton by‑election.

Meanwhile, GBP/EUR has extended its familiar February weakness — the pair has fallen in more than 60% of Februarys on record — and this year has followed that pattern. The cross dropped over 1% to a fresh two‑month low near €1.14, in line with the risks we flagged last week. The 100‑day moving average around €1.1456, a dependable floor since January, has now flipped into resistance, underscoring the deterioration in momentum.

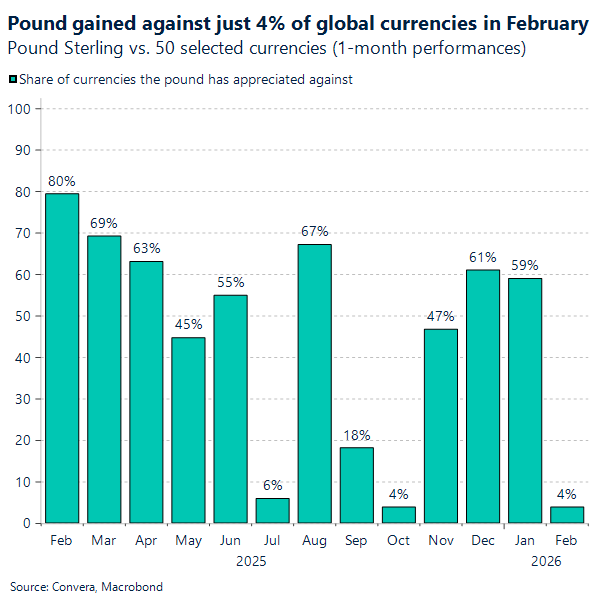

From a wider lens, the pound strengthened against just 4% of a 50‑currency global basket in February — another clear sign that domestic factors are driving the weakness. Slowing wage growth, softer inflation and a dovish BoE shift have all weighed on sentiment, and the political backdrop has now added another headwind. Markets are increasingly alert to the surge in support for the Greens and the prospect of a more expansionary fiscal tilt. For now, sterling and gilts are signalling caution rather than stress, but with political uncertainty rising and the policy trajectory appearing less predictable, the pound’s capacity to rebound looks limited until Labour provides clearer direction.

Market snapshot

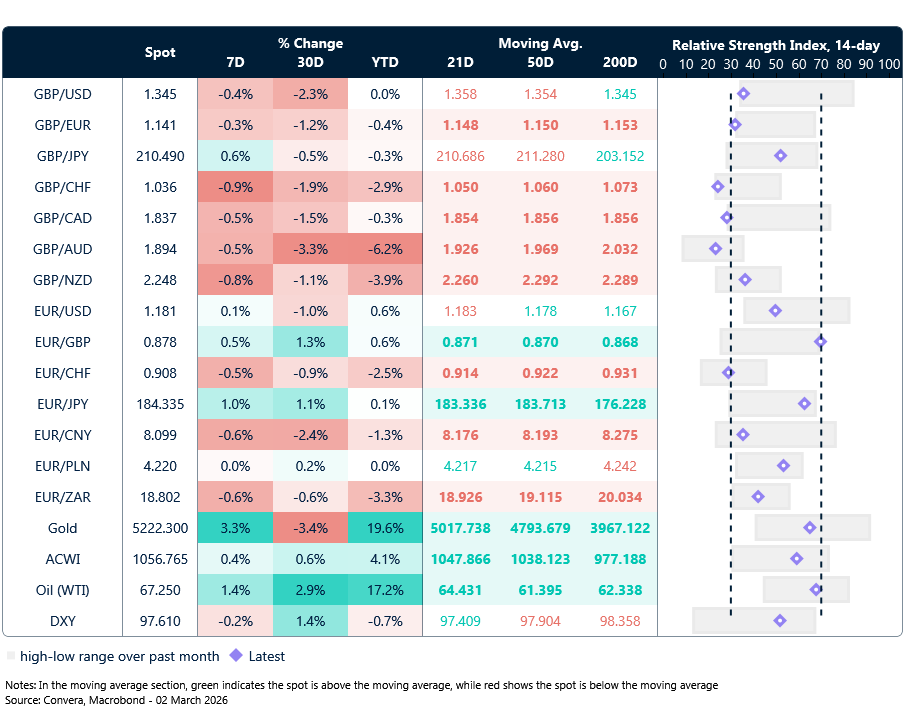

Table: Currency trends, trading ranges & technical indicators

Key global risk events

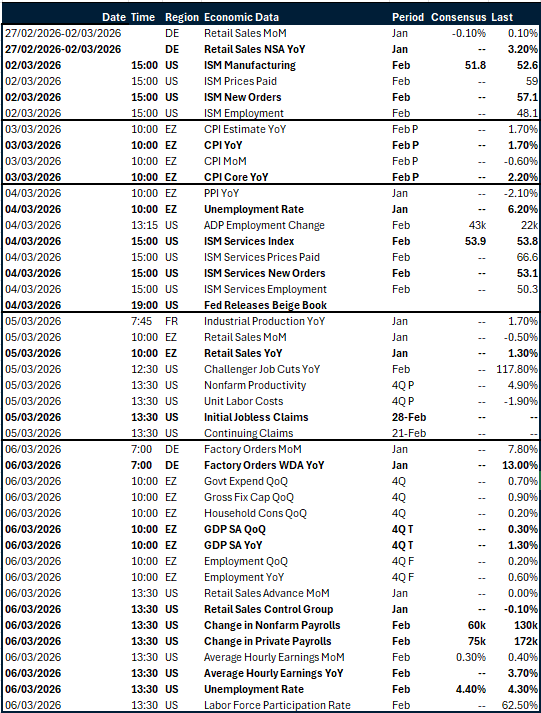

Calendar: March 2-6

All times are in GMT

Have a question? [email protected]

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.