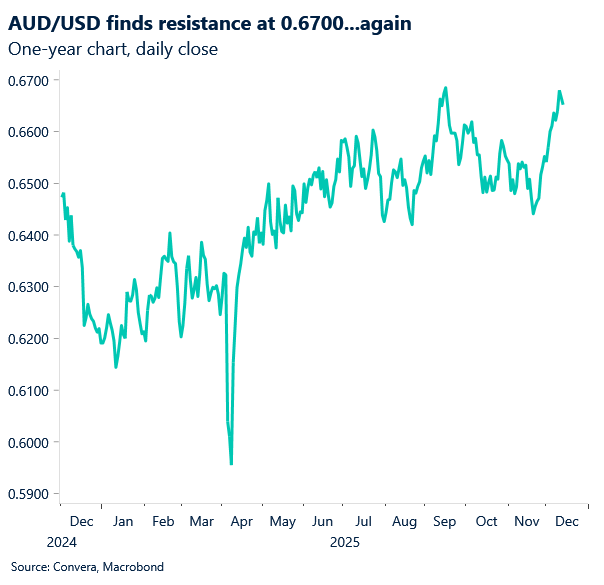

Aussie, kiwi ease from recent highs

Global markets drifted lower on Friday, with US shares falling and risk-sensitive currencies like the Aussie and the kiwi also under pressure.

Earlier last week, markets had neared recent highs, boosted by the Federal Reserve’s decision to cut interest rates. The Fed also appeared to remain open to further cuts.

However, the Aussie ended the week lower, falling on Thursday and Friday, to close the week with only a moderate 0.2% gain. Some momentum indicators, like the RSI (relative strength index), signal the market is vulnerable to further losses after a 3.5% gain since 21 November.

The kiwi was also lower in the back half of the week but held on to more gains, ending the week up 0.5%. Daily momentum studies also suggest the move higher is extended, with the NZD/USD finding resistance at the 200-day moving average – historically a key technical level.

CNH in focus ahead of data

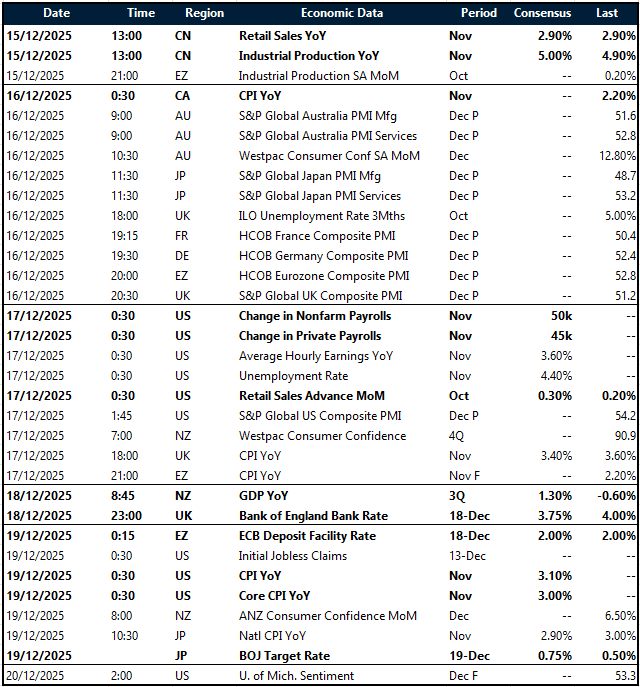

In a busy week of data, the early focus will be on Chinese monthly releases, including industrial production, retail sales and fixed asset investment. The numbers are due at 1.00pm AEDT.

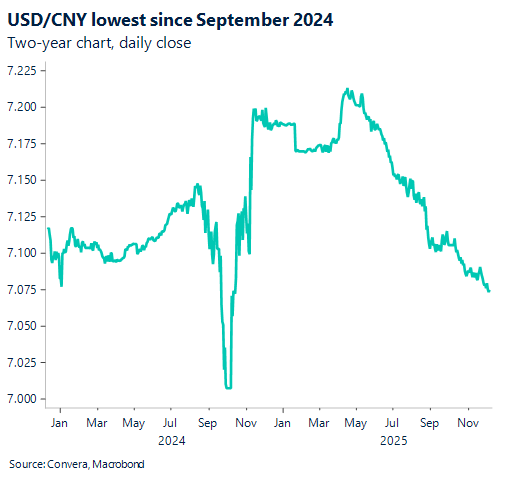

The Chinese yuan has recently been stronger, with the USD/CNH at 18-month lows.

The yuan’s strength has impacted local companies, with the state-owned financial newspaper The Securities Times reporting last week that Chinese corporates have seen a sudden surge in hedging activity.

In other markets, the AUD/CNH has eased from two-month highs, with major resistance seen at 4.7500.

BoE, ECB and BoJ due this week

A series of central bank meetings are due next week, including the European Central Bank, Bank of England and Bank of Japan. The BoE is expected to cut, although we remain doubtful of how dovish the tone will sound given still-elevated inflation levels. The ECB, meanwhile, is set to remain steady, with analysts eager to hear Lagarde’s potential response to Schnabel’s recent hawkish remarks. The BoJ is expected to hike.

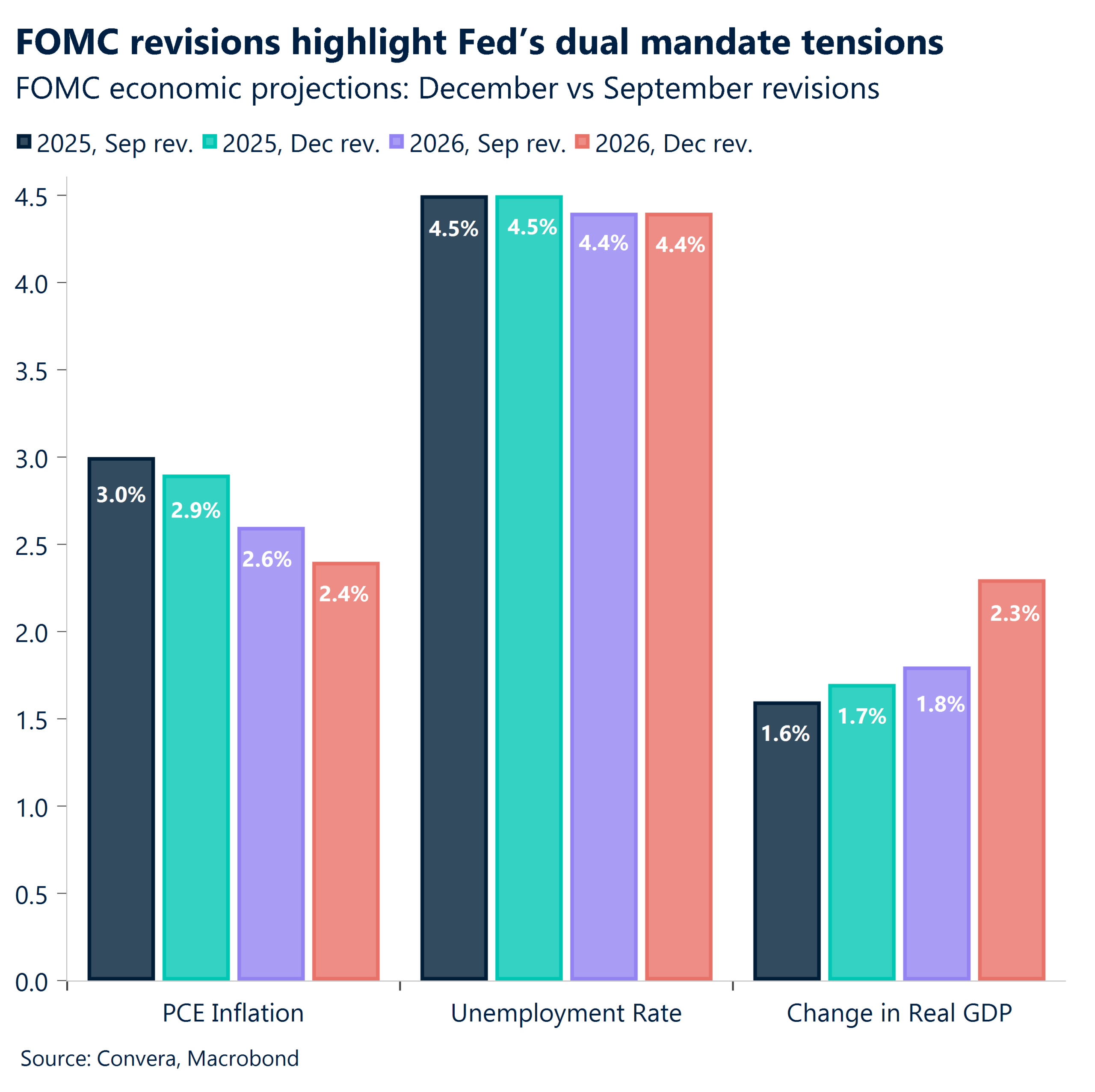

A similar story is unfolding in the US. The November NFP report, coupled with CPI, will be key inputs in shaping the Fed’s policy path as we head into 2026, particularly after the growing dissents within the FOMC.

On the US labour market, unemployment has gained greater importance, as Powell recently highlighted, alongside wage growth. At the December meeting, the Fed Chair stressed that cooling wage growth – driven by a softer labour market – is the main culprit behind lower services inflation.

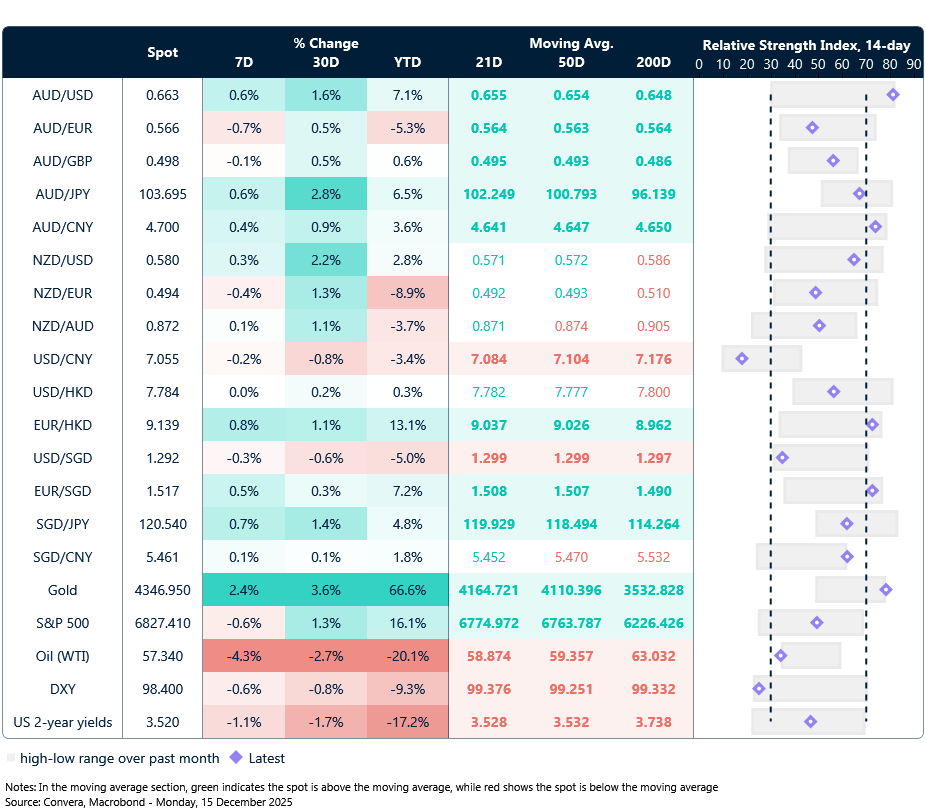

Aussie turns at highs

Table: seven-day rolling currency trends and trading ranges

Key global risk events

Calendar: 15 – 20 Dec

Have a question? [email protected]

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.