Pound mixed as risk sentiment sours

The pound has started Tuesday on a slightly weaker note against safe haven currencies like the US dollar and Swiss franc. Risk sentiment has soured after disappointing export and import data from China underscored the weak external and domestic demand in the Chinese economy. Elsewhere, UK house prices continue to fall and retail sales growth slowed to a 9-month low.

The outlook for the global economy remains uncertain, especially when we see such weak economic data from the world’s second largest economy, and it reinforces the need for further stimulus from Beijing. The pound, a risk correlated currency, is circa 0.2% lower against the US dollar this morning, hovering in the mid-$1.27 region, whilst GBP/EUR continues to grapple with €1.16. Sterling is about 0.4% stronger against riskier currencies though, such as the NOK, AUD, NZD and ZAR. Domestically, there’s little in the way of top tier macro data until UK GDP figures on Friday, but yesterday we saw the Halifax house price index fell by 2.4% year-on-year in July. It was the third straight month of yearly fall but slower than the 2.6% rate of decline reported in June and less than the 3.8% reported by Nationwide last week, as rising UK interest rates continue to feed through slowly to mortgage holders as fixed-rate deals expire.

Meanwhile, the British Retail Consortium data for UK retail sales growth revealed a 1.8% rise on a like-for-like basis in July 2023 from a year ago, a marked slowdown from the 4.2% gain in June, and a result of bleak UK weather and stubbornly high inflation.

Dollar firms but all eyes on inflation data

The US dollar remains the safe haven currency of choice. Amongst the major currencies, the dollar has the strongest negative relationship with the S&P500 when comparing the one-year rolling correlation of the 3-month change. Thus, the dollar is in demand this morning amid modest risk aversion after the batch of weak China trade data.

Amid US economic exceptionalism, the dollar is unlikely to majorly underperform its peers, especially given the ongoing frail economic backdrop in China and Europe. However, with slowing US jobs growth and signs of consumer credit on a softening trend, recession risks in the world’s biggest economy haven’t disappeared. Consumer spending is two-thirds of economic activity in the US, and with pandemic excess savings being run down, coupled with a sharp drop in banks’ willingness to make consumer loans, this is a troubling signal for US economic activity. As such (though mostly a result of US disinflation) the probability of the US Federal Reserve (Fed) raising rates in September are a slim 14% according to current money market pricing. The US inflation report this Thursday will be the prime focus though, and after the stronger than expected average hourly earnings number in the US employment report on Friday, there will be a lot of focus on a potential uptick in service price inflation.

Nevertheless, US shelter inflation, the biggest component of the consumer price index, and more than 40% of core, is set to slow significantly and may even turn into deflation next year, according to research from the Fed’s Bank of San Francisco. Short-term currency volatility remains pinned on yield spreads and consequently on policy, which will be heavily influenced by the US inflation report this week.

German disinflation continues, yields at 5-week low

Global investors are awaiting important economic data all around the world with the German CPI report earlier today kicking off the week of inflation. The euro had ignored weaker than expected industrial production numbers coming out of Europe’s largest economy and China recording disappointing trade numbers. This shows us that euro pairs continue to be driven by factors primarily outside the Eurozone.

After a policy-related increase of consumer prices in June from 6.1% to 6.38%, which had questioned the deflationary trend of the past few months, CPI growth returned to 6.2% in the month of July. Inflation remains close to its 14-month low and continues to show a short-term bias to the downside, as highlighted by various survey-based indicators and our proxy index for German inflation. The data print left the euro unfazed but did pressure yields across the curve, with the 2-year German bond yield falling to the lowest level since the middle of July at 3.1%. A day prior, German industrial production confirmed the latest string of weak economic data, falling by 1.5% in the month of June.

Markets are now zoning in on inflation prints from China and the US with EUR/USD perched around $1.10. Despite recent renewed risk aversion, the common currency is still profiting from elevated risk taking in general, with the S&P500 only being down on a 7-day basis (-1.45%), but up strongly on the 1-month, 3-month and 6-month timeframe.

Renewed risk aversion rocks Aussie & Rand

Table: 7-day currency trends and trading ranges

Key global risk events

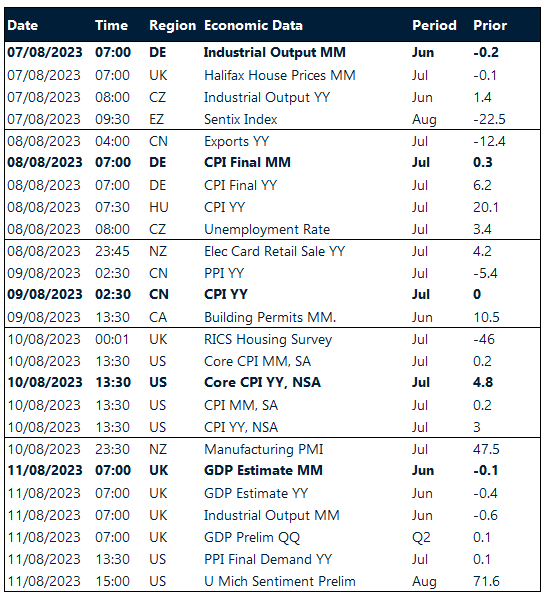

Calendar: August 7-11

Have a question? [email protected]

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.