Written by Convera’s Market Insights team

Treading water before inflation data

Boris Kovacevic – Global Macro Strategist

Global investors switched into a more neutral position at the weekly open after US equities had snatched a four week winning streak on Friday, rising by more than 8% since the beginning of the month. However, with inflation data looming later this week and investors trying to gauge the probability of a US soft landing, cautiousness set the tone for the trading session on Monday. The Greenback and US equities mostly treaded water with bond yields falling across the curve following a mixed US government bond auction in the afternoon and disappointing housing data. Markets are currently pricing in a 23% and 41% probability of the Federal Reserve cutting interest rates as soon as March or May.

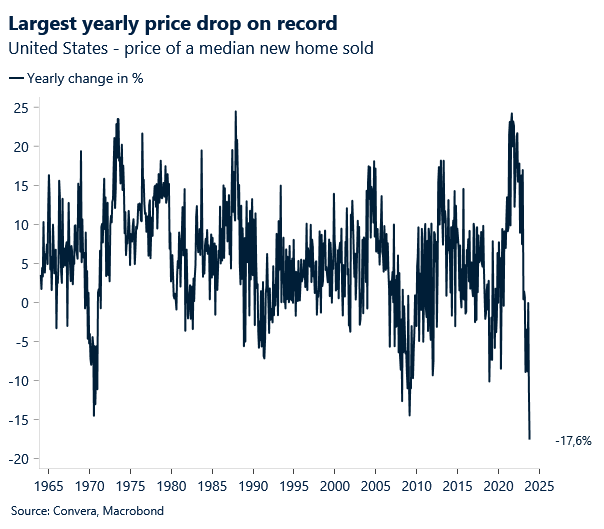

The week began with some disappointment on the macro front. New home sales in the US declined by 5.6% to 679 thousand in October, following a strong growth rate of 8.6% in the previous month. Mortgage rates at two decade highs are weighing on households affordability and have created a divergence between trends in new and existing homes. The median price of a newly sold home fell by 17.6% over the past 12-months, recording the steepest yearly drop on record (1965). At the same time, the general business activity index for manufacturing in Texas, published by the Federal Reserve Bank of Dallas, fell to the lowest level in four months in November. The barometer fell for a third consecutive month with the subindex for new orders now having been in negative territory for 18 months in a row.

The US Dollar index (103.40) is now positioned exactly at the middle of its short-term trading range (July low at 99.5 and October high at 107.3), being down 3.7% from its 2023 peak. Given that the dollars fate depends on the probability of a soft- or softish landing, weak macro data continues to have the potential to hurt the US currency. The upcoming release of US consumer confidence (today), the Fed’s Beige Book (Wednesday), PCE inflation (Thursday) and the ISM PMI (Friday) could push the dollar lower today, if the disappointments continue.

Leading indicators consistent with a recession in Q4

Boris Kovacevic – Global Macro Strategist

The euro was mostly unfazed by yesterday’s price action and Christine Lagarde comments on inflation and monetary policy. EUR/USD continued to trade above the $1.09 level with investors’ focus now shifting to this week’s releases of German inflation and retail sales and Eurozone inflation. Leading indicators for the European economy have started turning a corner as interest rates have peaked and the global trading slump slows. However, prospects of a quick rebound are being suppressed by the weakening of the region’s labor market and the expected fiscal drag going into 2024.

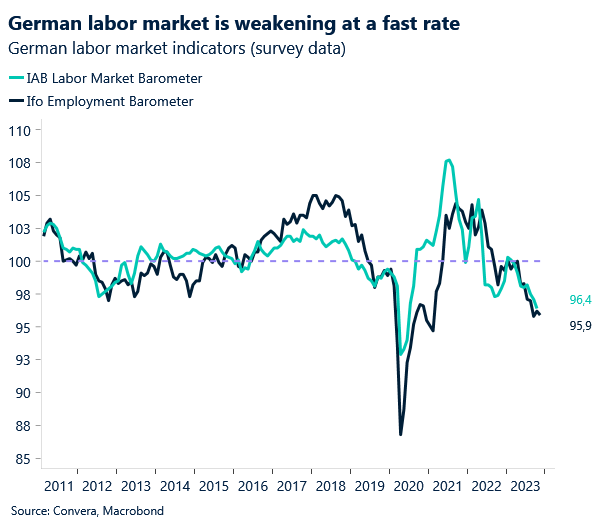

Last week’s purchasing manager surveys showed that companies in the Eurozone likely shed workers in November, with the employment sub-indicators for the French and German manufacturing sectors remaining deep in negative territory, dragging down the European labor barometer below the 50 mark. This is consistent with the Ifo and AIB survey indicating further job losses ahead as the number of unemployed people in Germany rose for nine consecutive months in October, recording the longest streak since 2005. A Eurozone composite PMI at 47.1 and Ifo current business conditions index at 89.4 are still both pointing to negative growth for the region in Q4.

ECB president Christine Lagarde said that she expects the economy to remain weak for some time as she took the stage before the Committee on Economic and Monetary Affairs of the European Parliament yesterday. However, she pointed out that the labor market displayed some resilience and that wage growth remained strong. The unemployment rate in the Eurozone still hovers near all-time highs at 6.5%. Going into the next year, an increasing jobless rate remains our base case as the leading indicators continue to deteriorate.

Proud pound holds firm

George Vessey – Lead FX Strategist

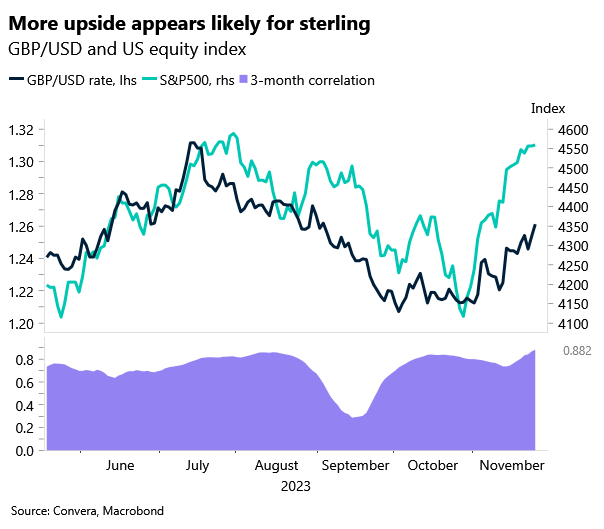

The pound hit a new 3-week high against the euro yesterday in the mid-€1.15 region and clocked fresh 12-week peaks versus the US dollar above $1.26, on track for its largest monthly rise in a year. This is largely a result of investors ditching the dollar amid rising US rate cut bets, but sterling also remains supported by improving global risk sentiment and UK data.

Yesterday, data showed the Confederation of British Industry’s monthly retail sales balance improved to -11 in November, surpassing market expectations of -30. Although it marked the seventh consecutive month with negative sales readings, it’s also another positive UK data surprise, which has helped support the pound’s appreciation of late. We note, the UK-US economic surprise differential has been trending higher and is at its highest point since early September. Outside of the macro space, in a potential longer-term boost for sterling, UK Prime Minister Rishi Sunak announced £29.5 billion of private-sector investments in Britain in the hope of restoring the country as Europe’s top foreign direct investment destination. However, looking into 2024, although we are mildly bullish on the pound, we expect the UK economy will struggle to gain momentum due to tighter monetary and fiscal policy settings, limiting sterling’s gains.

Separately, with global stocks on track for their best month in three years and the British pound’s strong positive correlation with equity performance due to its risk-sensitive nature, we feel there’s more room for GBP upside in the short-term. Whether the “risk on” environment continues though, depends on the upcoming inflation data this week.

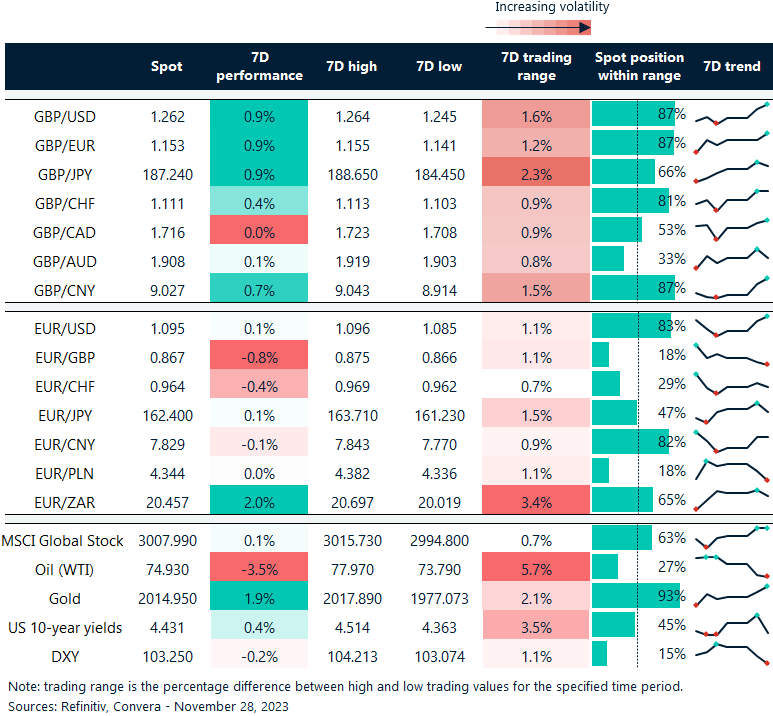

Sterling holding above key levels

Table: 7-day currency trends and trading ranges

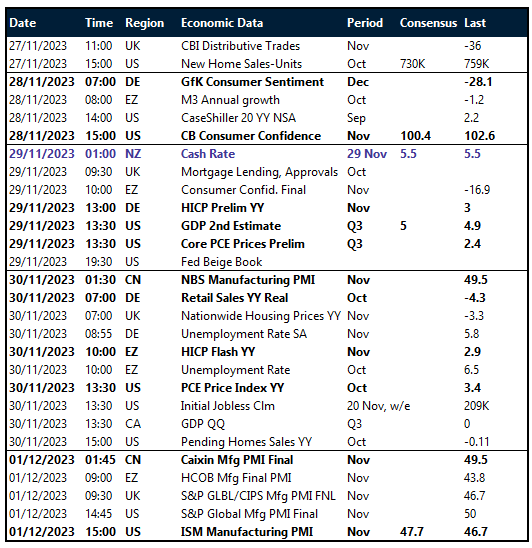

Key global risk events

Calendar: November 27-December 1

Have a question? [email protected]

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.