USD: CPI delivers calm, geopolitics steals the spotlight

Oil prices are under pressure again, trading just south of 100$ a barrel (Brent), after a brief reprieve following reports that the International Energy Agency (IEA) plans to release 400 million barrels of oil from emergency stockpiles – the largest draw on record. Latest developments include China tightening fuel‑export curbs to manage the fallout from the conflict in the Middle East. Meanwhile, attacks on two tankers in Iraqi waters prompted Oman to evacuate all vessels from a key oil port. The headlines injected fresh bullish impetus into the US dollar.

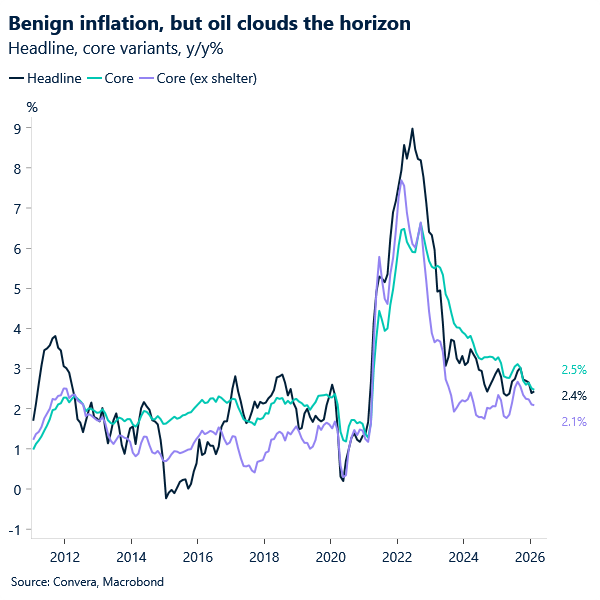

Moving away from geopolitcs, February’s US CPI report came in broadly aligned with expectations yesterday. Headline inflation rose 0.3% month‑on‑month, consistent with recent prints, while core inflation increased 0.2%. On an annual basis, the readings were 2.4% and 2.5% respectively. The calmness across the price complex also transpired from even cleaner forms of core inflation that better capture domestic demand dynamics, e.g., core ex shelter. While this is certainly good news, markets have largely discounted the benign outcome. The ongoing conflict in the Middle East has pushed inflation risk back into focus, overshadowing the softer CPI details. Ultimately, the longer the conflict persists, the more its effects will filter through the inflation curve.

In fact, durability is the key variable that will determine how far these pressures pass through to the broader price basket. Given the stability across the core, less‑volatile components, expectations lean toward a temporary rise concentrated in the most directly exposed categories – gasoline and food may register sharp spikes – but the degree of pass‑through will dictate whether more persistent price pressures emerge. For now, the consensus that the US’s oil production capacity, coupled with a fairly stable price backdrop at present, can offset longer‑term inflation risk. This is reflected in the divergence between 5‑year breakevens and 5y5y inflation forwards. The latter, which captures expectations five years ahead, remains notably more anchored.

The dollar index (DXY) remains bid, largely unfazed by the benign CPI outcome, with yields continuing to edge up as the conflict remains the dominant driver of market action. We expect the dollar to hold its posture above 98.500 – recently identified as short‑term support – for the remainder of the week, barring any material signs of de‑escalation.

GBP: Sterling resilience has limits

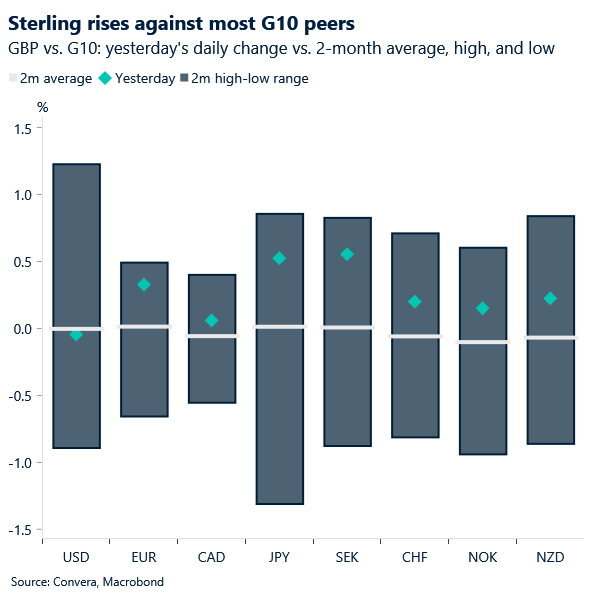

The pound appears to have fared better than its peers amid the ongoing conflict in the Middle East so far. Sterling is higher against the euro this week and, on a month‑to‑date basis, it has fallen 0.7% against the dollar, compared with a 2.2% decline in the euro against the dollar.

Sterling appears supported by the most forceful hawkish repricing among major currencies, driven largely by the BoE’s focus on a still-elevated inflation and an easing bias that hinges on a sharp drop in the headline figure over the coming months. That said, the persistently cool labour market in the UK may act as a deterrent to more sustained inflation pressures: weaker demand for workers implies less bargaining power to push for higher wages in response to rising energy costs. This backdrop would confine inflation pressures more strictly to the supply side, helping contain any more durable impact.

A softer labour market also reinforces the view that the BoE will ultimately lean toward rate cuts, regardless of the pace. In that sense, the support sterling is drawing from the current backdrop may prove short‑lived, particularly as renewed inflation pressures weighing on real incomes would further weaken an already soft labour‑market environment.

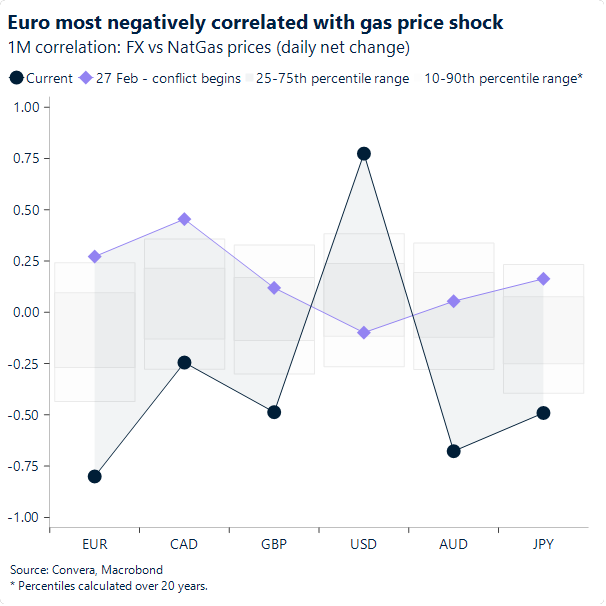

EUR: Still reliant on sustained energy flows

The IEA’s approval of a coordinated release of more than 400 million barrels of emergency oil reserves has offered a brief lift to sentiment, but it has done little to change the euro’s trajectory.

EUR/USD is struggling to hold above 1.16, capped by its 200-day moving average, and remains one of the weakest performers in G10, reflecting the market’s view that this is a short‑term reprieve rather than a genuine solution. Europe may be more exposed to natural gas than crude, but oil still matters for inflation, freight costs and industrial margins. Strategic reserves can smooth volatility, yet they cannot replace the physical flows lost or repair the competitiveness hit facing Europe’s industrial base while the Strait of Hormuz remains closed. Until energy flows normalise and Middle Eastern production restarts, the eurozone faces a deeper and more persistent terms‑of‑trade shock than many peers.

This is also why the euro is becoming increasingly unresponsive to monetary policy signals. The beta of EUR/USD to short‑term rate differentials has collapsed to virtually zero, meaning shifts in ECB expectations are having almost no influence on the currency. Even as markets nudge ECB pricing slightly higher amid the conflict‑driven inflation scare, the euro has barely reacted. Energy flows — not rate spreads — are driving EUR/USD in the current regime.

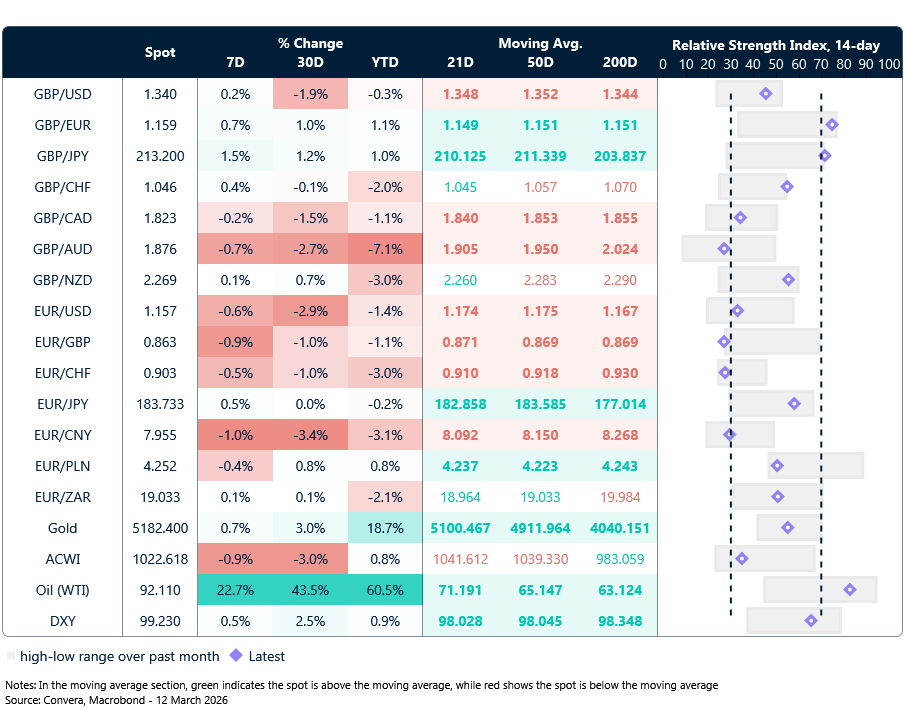

Market snapshot

Table: Currency trends, trading ranges & technical indicators

Key global risk events

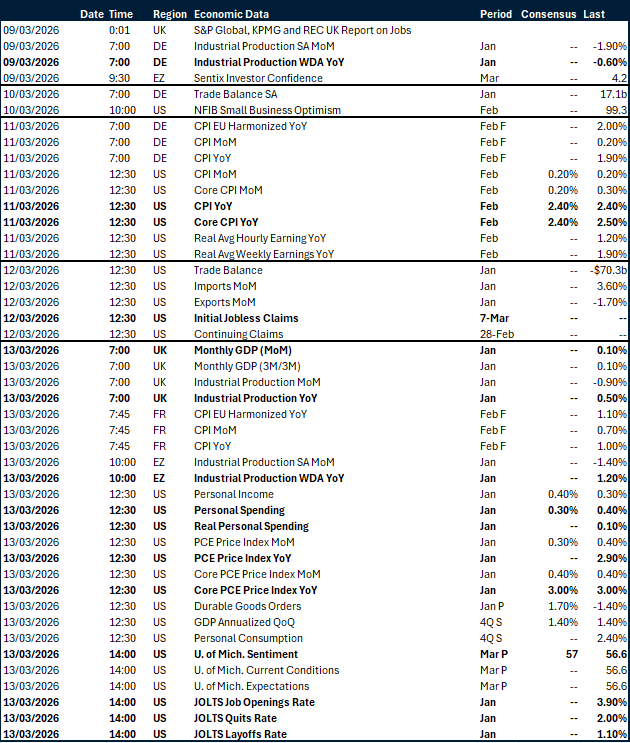

Calendar: March 9-13

All times are in GMT

Have a question? [email protected]

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.