Written by Convera’s Market Insights team

Data to decide size of Fed cut

George Vessey – Lead FX Strategist

The US dollar staged a strong end to August last week following a patch of stronger US data releases and month-end flows, but it still recorded its worst month of the year, with the dollar index dropping over 2%. Equity markets recorded a strong month, supported last week by the Federal Reserve’s (Fed) preferred measure of inflation which advanced at a modest rate, backing policymakers’ plans to cut interest rates in September.

The chirpier market mood of late could come under pressure this week though as attention shifts to some big US data releases, including ISM PMIs on Tuesday and Thursday and the jobs report on Friday. Markets remain highly data dependent and sensitive to macro surprises and the looming US data dump will decide the magnitude of the Fed’s rate cut this month. We continue to believe that a 50-basis point cut is on the table for the Fed. While not the base case, even a slight 0.1% increase in the unemployment rate to 4.4% would likely increase such a scenario exponentially. However, a fall of the jobless figure and improving ISM employment sub-indices would break the will of the doves looking for a jumbo cut. Such an outcome would likely support the dollar too.

Meanwhile, US stocks, face historically the worst month of the year for equities as September has been the biggest percentage loser for both the S&P 500 and the Dow Jones Industrial Average since 1950. In the currency space, traders are also on high alert. Implied volatility has not been this elevated going into a week in all of 2024 for USD/CAD and GBP/USD. A calm start to the week most likely awaits though with both US and Canadian markets closed for Labour Day today.

Sterling lacking fresh positive catalysts

George Vessey – Lead FX Strategist

Whilst GBP/USD has lost its grip on $1.32, a level it’s only been above for four days out of the past two years, it recorded its biggest monthly gain since November versus the US dollar and remains over 6% above its 2-year average rate of circa $1.24. This week, sterling is likely to be driven more by US data as investors judge the pace of upcoming easing cycle.

The 2-year UK-US yield differential has risen to plus 244 basis points, from a negative 530 basis points at the end of May, helped mainly by dovish Fed repricing, but also the Bank of England’s more cautious messaging of late. This has led the latest leg higher in GBP/USD to scale 2-year peaks. A narrowing in US-UK growth differentials has also helped support the pound given upbeat UK data. Hence the options market has turned the most bullish on sterling’s prospects over the next month since 2020. FX options implied probability also puts a near 40% chance of cable trading between $1.30-$1.35 by year-end. The biggest risks to the pound include: 1. The BoE catching up on the easing narrative and 2. A downward bias on the UK’s near-term growth prospects via fiscal tightening in the upcoming UK Budget in October.

Meanwhile, looking further ahead and on the UK political front, Labour faces two competing economic narratives which could help or hinder the pound. A positive one involves resetting the UK-EU relationship but a more negative one in the near term is the possibility of fiscal tightening in the upcoming UK Budget in October.

Euro momentum turns bearish as inflation cools

Ruta Prieskienyte – Lead FX Strategist

The latest macro news has endorsed the readjustment lower in EUR/USD, with the pair falling over 1% in the last week of August, while still maintaining monthly gains of over 2%, its best performance thus far in 2024. European stocks closed the month in the green, recouping early August losses. Bonds remained bid on the last trading day of the month as the German Bund yield curve shifted higher, outperforming US Treasuries.

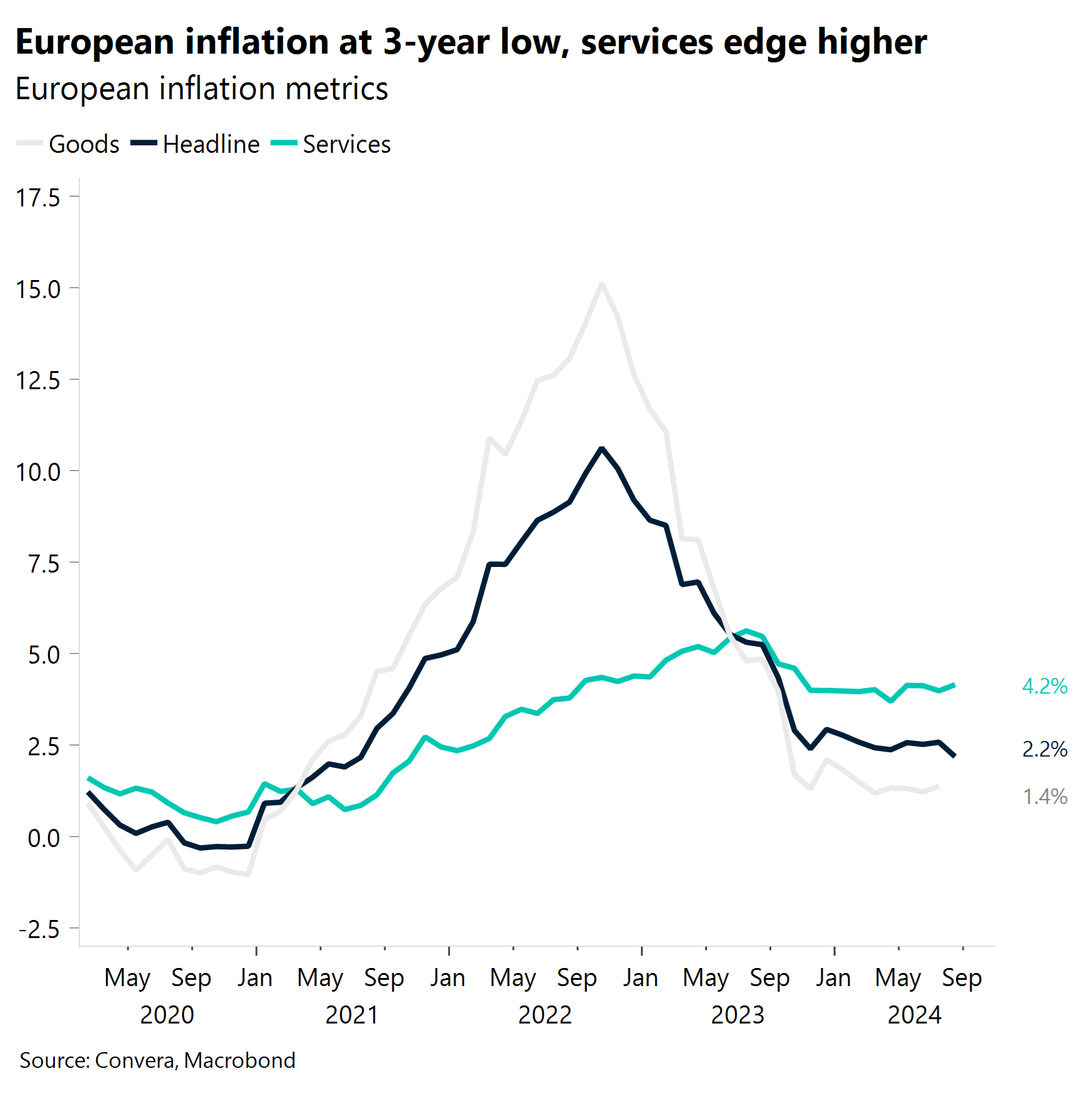

The flash annual inflation rate in the Eurozone, released last Friday, unexpectedly fell to 2.2% in August, down from 2.6% in the previous month, marking the softest increase in consumer prices since July 2021. The slowdown was due to a sharp decline in energy costs, thanks to base effects. Conversely, services inflation, a closely observed metric by the ECB, rose to 4.2%, while core inflation cooled to 2.8%. Month-on-month inflation edged higher by 0.2%, in line with expectations. The latest progress on inflation should give the central bank confidence to cut rates in September, but what lies beyond is unclear for both the market and ECB policymakers. The EUR OIS curve continues to price in 63bps of easing by year-end, suggesting investors expect the central bank to cut at a quarterly cadence despite growing risk concerns.

This week’s domestic macro calendar is sparse of top-tier data releases, with investor attention almost exclusively captured by US activity and labour market reports. German state elections in Thuringia, Saxony, and Brandenburg may divert some of that focus as the far-right AfD continues to move up the polls. Ultimately, the market hinges the euro’s prospects on this week’s US NFP print, with euro volatility going into the event set for its strongest close since January and one-week risk reversals retreating to neutral balance for the first time in two weeks.

Stocks near all-time highs

Table: 7-day currency trends and trading ranges

Key global risk events

Calendar: September 2-6

All times are in BST

Have a question? [email protected]

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.