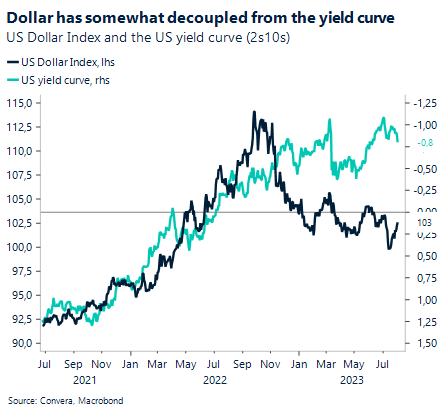

Dollar rises as yield curve steepens again

Investors continued to focus on the incoming data, one week after the Federal Reserve raised interest rates to the highest level in 20 years and days after the US lost its triple A rating from Fitch. Yesterday’s data releases failed to provide a unified picture of the economy but did confirm that a recession still seems far off, with yields pushing higher, laying the groundwork for some more dollar strength.

A report from the US Bureau of Labour Statistics showed that unemployment claims rose by 6000 in the week ending July 29th. The increase was however not significant enough to subdue expectations that the labour market remains resilient. Another release shows labour productivity increased in the second quarter by the most in three years as well, once again playing into the same theme. The last data release of the day came in the form of the ISM purchasing manager index for the services sector. The barometer ticked lower but remained in positive territory at 52.7.

The uptick on the long end highlighting the deteriorating fiscal strength in the US, has steepened the yield curve with premiums for hedging further yield increasing. The US dollar did not get dragged down by this development as the dollar’s safe haven status overshadowed its relationship with the US yield curve. The US Dollar Index is on track to record its third weekly rise, with only today´s nonfarm payrolls report standing in the Greenback’s way.

Pound subdued as BoE hikes rates for 14th time

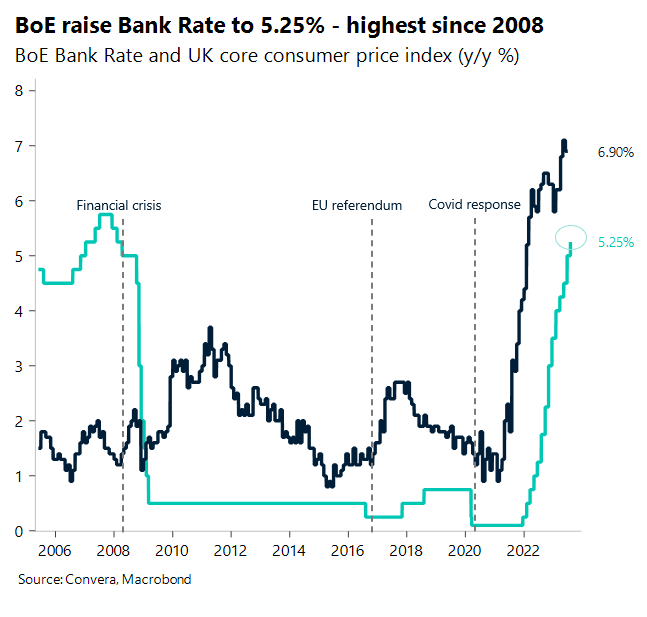

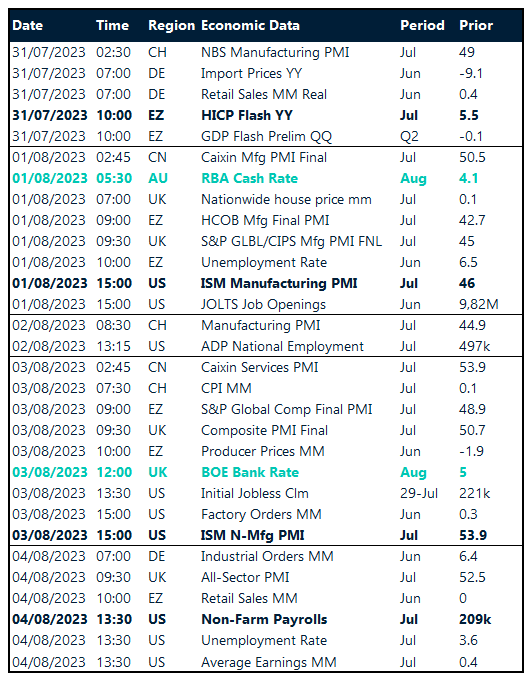

As expected, the Bank of England (BoE) raised its policy interest rate by 25 basis points to 5.25% yesterday, marking a 14th consecutive increase, and bringing borrowing costs to fresh 2008 highs. Along with UK government bond yields, the British pound slumped across the board as the BoE reaffirmed its view that inflation will drop sharply to 5% by year-end as policy is to remain restrictive for some time.

The BoE forecasts inflation to continue falling, which matches a leading indicator that we’re watching closely of private sector selling expectations. As such, we’re likely very near the end of the BoE’s tightening cycle, though markets are pricing a 60% chance of another 25-basis point hike in September. Headline (7.9%), core (6.9%) and services (7.2%) inflation all fell more than expected last month, but we shouldn’t get ahead of ourselves after one weak inflation report, especially with wage growth still strong. This is why the Monetary Policy Committee vote split went three ways with two members voting for a larger 50-basis point hike, though one voted to keep rates unchanged at 5%. Overall, the message from the BoE was that although we are nearing the peak in interest rates, they are likely to remain “higher for longer”. Sterling had marched to fresh 16-month highs above $1.31 against the US dollar when markets were pricing in a peak BoE rate of 6.5% next year. Now, that expected peak is just shy of 5.75% by March 2024, and it’s this dovish rate repricing, that has added to sterling’s woes.

The risk-sensitive pound has also been knocked by growing global growth fears amid weaker PMI data of late, but also the US credit rating downgrade, which spurred safe haven buying. Unless risk appetite returns soon, we see a potential test of $1.2580 unfolding for GBP/USD, but the recent rebound back above $1.27 and notably reversal signal on the daily chart has weakened this call in the short-term.

Euro rebounds as German factory orders surge

The euro continues to languish under the $1.10 handle against the US dollar but has found some much-needed support at both its 50- and 100-day moving averages located in the lower realms of the $1.09 region. Data from Germany this morning has helped the rebound, as factory orders unexpectedly surged 7% month-on-month.

The market consensus was to see a 0.2% decline in new orders, but instead we saw the steepest pace of growth since June 2020, which bodes well for Germany’s industrial production print due on Monday, where we were expecting to see a fall. Meanwhile, yesterday’s data showed Eurozone producer prices declined by 3.4% year-on-year in June, marking the second consecutive decline in producer prices and the steepest since June 2020, mainly on account of energy prices. This week, final PMIs indicated a further slowdown in the services sector and a larger contraction in manufacturing in the Eurozone, although GDP returned to growth and expanded at a faster-than-expected 0.3% in the second quarter. Recall that the European Central Bank (ECB) remains data dependent, so each data point will be digested carefully by both policymakers and market participants. Eurozone retail sales are up next today, but most focus will likely be on the pivotal US jobs report.

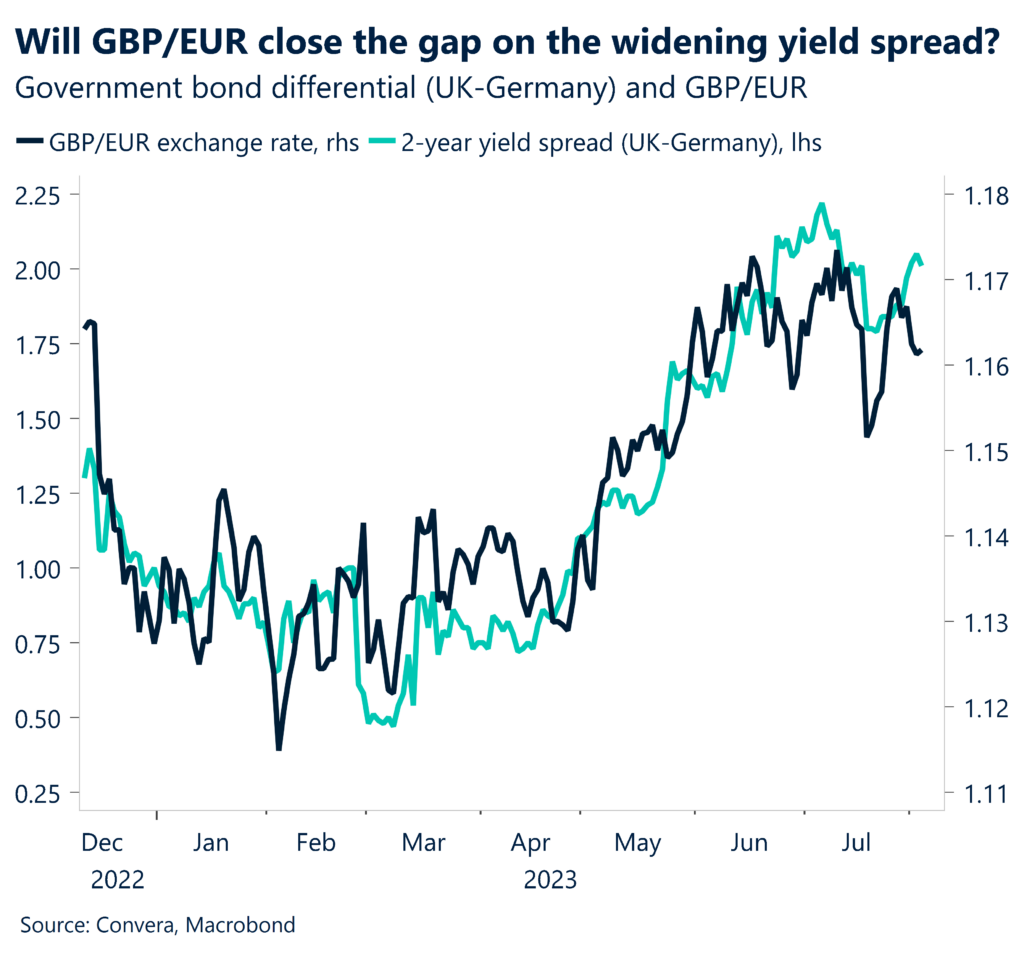

The markets believe the ECB is done with hiking, attaching a 70% probability of no change to rates in September. As such, due to yield spreads favouring the pound with the BoE expected to hike at least once more, we’ve seen GBP/EUR reclaim the €1.16 threshold, but the currency pair is primed for its third weekly drop in four.

Dollar’s rebound gathered pace this week

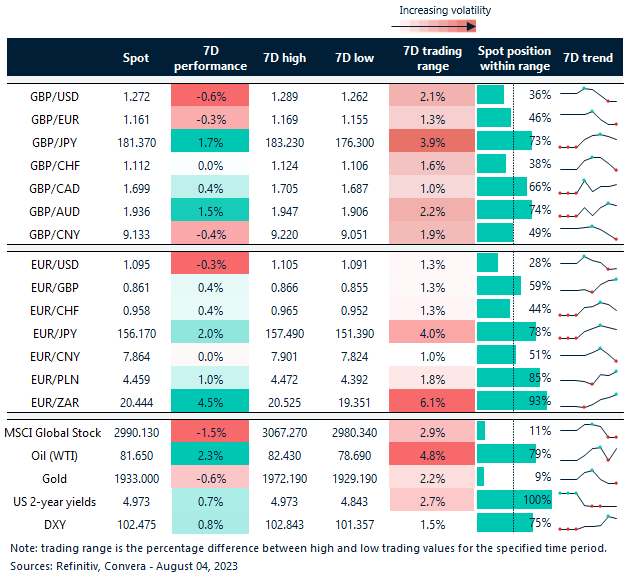

Table: 7-day currency trends and trading ranges

Key global risk events

Calendar: July 31- August 4

Have a question? [email protected]

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.